In my continuing quest to think through Bagehot’s dictums and their relevance for the current age, I came across a good speech by Brad Jones of the Reserve Bank of Australia Bagehot and the Lender of Last Resort – 150 Years On (link to video, or transcript)

He starts by giving some history on the pre-Bagehot arguments for a lender-of-last-resort.

Some History of the Lender-of-last-resort

The earliest direct reference to the lender of last resort concept was traced to Sir Francis Baring following a wave of bank runs in 1797, when he argued for the Bank of England (then financing war against the French) to furnish stressed institutions with liquidity as private sources were exhausted. Henry Thornton progressed these ideas further in 1802 when setting out the considerations, including moral hazard, that central banks must balance and that still resonate today:

“The relief should neither be so prompt and liberal as to exempt those who misconduct their business from all the natural consequences of their fault, nor so scanty and slow as to deeply involve the general interest.”[3]

But it was not until 1873 that Bagehot counselled that to avert panic, central banks should lend early and freely to solvent firms, against good collateral and at ‘high’ rates.[4] This prescription was motivated by the financial panic that followed the collapse of London’s biggest bill broker, Overend & Gurney, in 1866 – a panic that was only contained by the Bank of England’s provision of liquidity to the financial system after its initial refusal to support the broker. Central to Bagehot’s axiom was the idea that public confidence could be enshrined, and an unnecessary credit contraction averted, by a conditional commitment from the central bank to provide liquidity insurance in a crisis. By the end of the 19th century, the Bank of England had become well practised in last resort lending.

In the normal course of events, the liquidity operations of central banks are prosaic affairs.

But last resort lending by central banks is fundamentally different. It involves the dire circumstance where stability of the financial system is in question.

We have long accepted that liquidity and maturity transformation of this sort is economically and socially valuable − requiring banks to fully self-insure against liquidity risk by holding only the most liquid assets (as per the ‘Chicago Plan’ and ‘narrow banking’) would undermine their ability to extend credit and see credit risk concentrated in less regulated institutions.

Only [the central bank] can act as the backstop provider of emergency liquidity insurance to fundamentally sound institutions in bad states of the world. In such circumstances, last resort lending can spare society from the severe (but otherwise avoidable) disruptions to the economy associated with bank failures.

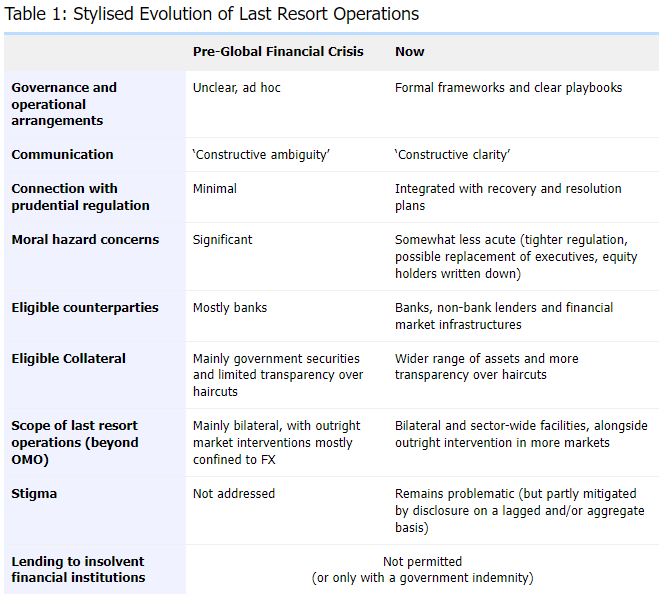

Then and Now - Evolution of LOLR

In my assessment, the most consequential development has been evident in central banks formalising, and more openly communicating, their framework for last resort operations.

Another feature of the evolution in last resort operations has been to encompass a wider set of institutions, collateral and asset markets. For a start, bilateral lending to banks is no longer the only form of emergency lending envisaged – most central banks now explicitly incorporate liquidity facilities for key financial market infrastructures. And some, like the US Federal Reserve and Bank of England, have gone further by establishing sector-wide liquidity facilities for specific investment vehicles, like money market funds (US) and pension and insurance funds (UK).

First, severe liquidity stress can emerge in a financial system even in an environment of abundant central bank reserves. The distribution of liquidity across institutions matters, not just the aggregate level.

Second, as we saw in the US and Switzerland in March, bank deposit runs can occur far more rapidly in the digital era than envisaged when the Basel III requirements were initiated.

Third, left unaddressed, systemic risk can emerge from liquidity stress experienced by bank and non-bank lenders that are not considered systemically important by traditional metrics.

Fourth, as an increasing share of activity in the global financial system is conducted outside of the traditional banking industry, central banks will be prompted to revisit their framework for emergency lending to non-banks and outright buy/sell operations in key markets.

Finally, while prevention is always preferable to cure – and there should be no illusion that the primary obligation of the industry is to manage its own risks prudently – recent international events have highlighted the importance of clear response frameworks and public communication by policymakers in periods of stress.

Readers will recall that I think the central bank ought to offer (and/or require) ex-ante liquidity insurance; they have the inside information needed to price it properly. Wrote about it back in Perspective on Risk - May 19, 2023 (Bagehot is out of date)

Prepositioning Collateral at the Discount Window Is The Future

This headline has caught some attention, with some commentators suggesting the Fed is trying to do away with the stigma of accessing the discount window (hint: it will not).

What I read this as is an attempt to get banks to preposition collateral at the Discount Window to alleviate the operational constraints seen during the regional bank failures. Virtually every post-mortem spoke about the operational difficulties that occurred since the firms had not practiced their use of the DW. Staying within a Bagehot construct (as opposed to the insurance construct I proposed above), this is clearly a next-best solution.

Izabella Kaminska have come out in support of this approach. She has a paywalled Politico article that you can access cheaply here, worth paying the five pounds sterling. I’ll respect her need for revenue by only briefly excerpting:

There’s a quiet revolution happening at the heart of central banking, but you wouldn’t necessarily know it.

In its most extreme incarnation, ‘pre-positioning’, as the concept is becoming known, would turn central banks into what Lord King has colorfully described as a Pawnbroker For All Seasons (PFAS)

The Discount Window is not the ideal place to position highly liquid collateral; instead it will see less liquid collateral like bank loans and securitization tranches(assuming they don’t all go to Private Credit ;→) This will require the Fed to up their game on marking this type of collateral accurately.

As you know, I am critical of the BTFP. It was a mistake and violated Bagehot’s dictum of lending freely at a penalty rate against good collateral. The collateral was inadequate, and the pricing was too low. When I’ve been asked, I’ve said that I firmly believes that the BTFP sunsets at its March maturity. I can’t imagine the Fed is happy that they have created a facility that is being arbitraged. The BTFP is charging a lower interest rate than IOR, creating an arbitrage reminiscent of the bankers' acceptances debacle the Fed created at the end of the 1920s. Unacceptable.

[Addendum: Since I wrote this the Fed announced that they will not renew the BTFP and will floor the interest rate at IOR, Good move on the later, if a bit late.]

The Yale Financial Stabilty folks have published a nice article on the economic advantages of borrowing from the FHLBs (as opposed to the Discount Window): FHLB Dividends: Low-Hanging Fruit for Reconfiguring FHLB Lending. They conclude:

If FHLB credit remains structurally competitive with—and often cheaper than—the Fed’s primary credit, discount window stigma will remain.

Finally, JPMC published a piece with this nice table highlighting the differences between primary credit, the BTFP and FHLB advances.

Macrofinance & Resilience

Markus Brunnermeier delivers the American Finance Assn. Keynote Macrofinance and Resilience (Youtube). Markus is among the best economists discussing financial crises. Possible future Fed Vice Chair or even Chairman. Fun introduction by Monika Piazzesi.

He discusses the need for economic policymakers to change from ‘risk management’ to ‘resilience management.’ At time t you must invest in your potential response at time t+1.

Much of the talk is about second generation economic models, and how they may need to evolve. Not for everyone.

This paper analyzes a model of the mortgage market, considering scenarios with and without government-sponsored mortgage securitization. Conventional wisdom says that securitization, by fostering diversification and creating a “safe” asset in the form of mortgage-backed security (MBS), will reduce risk and enhance liquidity, thereby mitigating financial crises. We construct a strategic-game framework to model the interaction between the securitizer and banks. In this framework, the securitizer initiates the process by setting the MBS contract terms, which includes the guaranteed rate and the criterion that qualifies a mortgage for securitization. The bank then selects which qualifying mortgages to exchange for the MBS. Our investigation leads to a key result: government-sponsored securitization, somewhat counterintuitively, is more likely to exacerbate the severity and frequency of financial crises.

R* Wars

Some will remember that I have periodically written about what the economists call the “natural” rate of interest, or r*1 The more formal definition is:

the the inflation-adjusted, short-term interest rate that is consistent with full use of economic resources and steady inflation near the Fed’s target level.

There have been a few developments, so here is a brief summary.

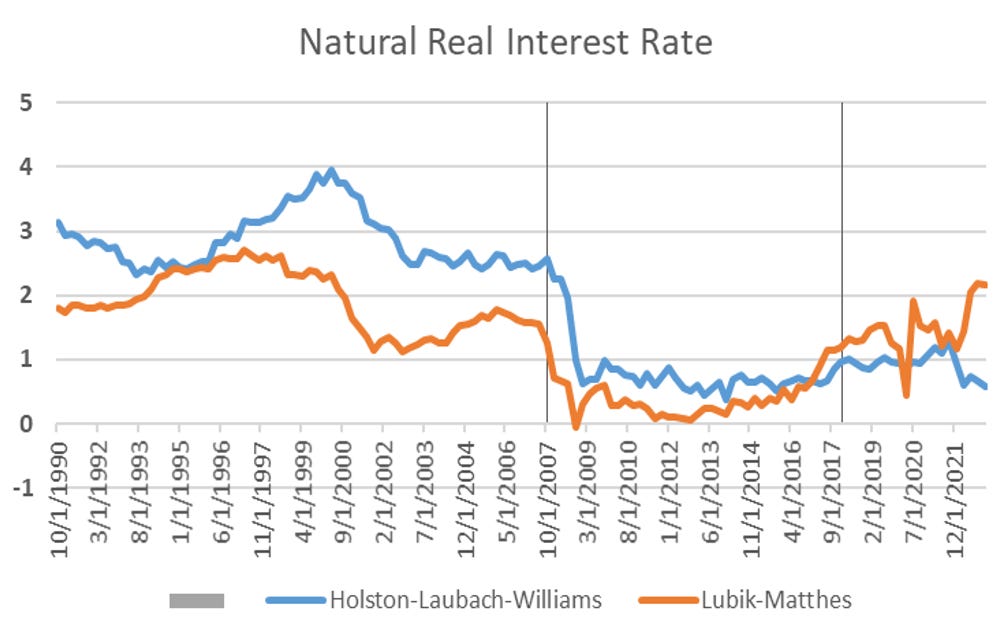

The two primary models that estimate r* have diverged, with the “Richmond” Lubik-Mathes model showing substantially higher real natural rate than the HLW model. Interestingly, the 5yr-5yr forward TIPs premium is right in the middle of these two.\

In part this matters because it could indicate whether the economy is performing above capacity, in which case a higher rate is justified, or not.

Williams

John Williams, President of the NY Fed, and the Williams in the HLW model, gave a speech in November Restoring Price Stability where he cited the level of the HLW model when stating:

Based on model estimates of the longer-run neutral interest rate that incorporate forecasts for the current quarter, the stance of monetary policy is quite restrictive; indeed, it is estimated to be the most restrictive in 25 years.

The estimate of r-star from the so-called “HLW” model for the first quarter of this year was actually below pre-pandemic levels, leading NY Fed President Williams to conclude that “there is no evidence that the era of very low natural rates of interest has ended.”

On the other hand, estimates of the natural rate of interest from Lubik and Matthes (LM) of the Federal Reserve Bank of Richmond using a different/more flexible modelling approach suggest that the natural rate of interest had increased from a pre-pandemic level of about 1 ¼% at the end of 2019 to a little over 2% in the latter part of 2022 and the first quarter of 2023.

Goldman Sachs released a research report questioning the reliability of the low r-star estimates generated by the HLW model, and suggested that r-star (which is stated in real terms) was probably closer to 1 to 1 1/4%

In addition, “real” interest rates as measured by “Treasury Inflation Protected” (TIP) yields have increased recently to their highest levels in about 15 years, with 5-year TIPS yielding about 2.2% and 10-year TIPS yielding almost 2%.

Importantly, he concludes that the FOMC dot plots shoot too low as the natural rate of interest has risen.

In sum, despite what NY Fed Governor Williams said, there is in fact evidence that the natural rate of interest, or r-star, has in fact risen over the last year, and by some measures it would appear as if r-star may be at levels not that far from the those seen just prior to the financial crisis of 2008. If that were the case, then a “soft-landing scenario where inflation fell back to 2% would be one where the Federal Fund Rate fell back to the 3 ½-4% level, rather than the 2 ½-2 ¾ % level implied by the HLW model or the FOMC’s “dot plots.”

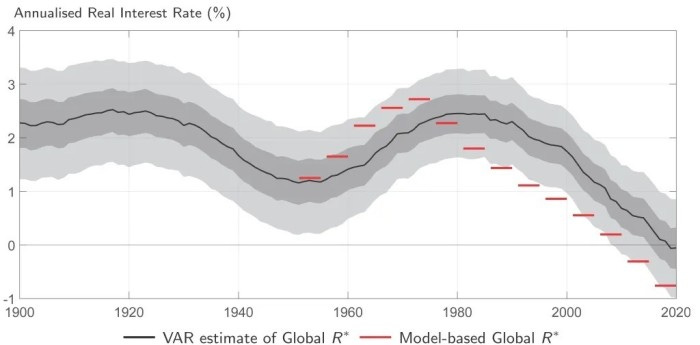

The Bank of England’s Ambrogio Cesa-Bianchi, Richard Harrison and Rana Sajedi have therefore tried to come up with an estimate for the global economy’s R*, and decompose it into its various components.

Their stab at this differs from previous attempts which mostly used different models to come up with more real time estimates. Instead, they wanted to look through shocks to see the longer term trend.

As the economists state:

Within a standard macroeconomic framework, secular movements in real interest rates are determined by the factors that drive the supply and demand for capital. Over the long run, when capital can move freely across countries, there exists a single interest rate that clears the global capital market.

We deliberately abstract from shocks that determine equilibrium real interest rates over shorter horizons in individual economies and therefore cause these shorter-term equilibrium real rates to deviate from Global R*.

Interesting results:

Chart 1 shows our model simulation of Global R* alongside the VAR estimate. We plot the model simulation as five-year lines, to emphasise that the model determines the interest rate for successive five-year periods, though the interest rate is shown as an annualised percentage rate.

The suggestion that the global trend real interest rate could be negative may seem striking, as it would appear to be possible to finance investment projects with negative returns. However, the marginal product of capital exceeds the safe rate of return because of the mark-up charged by imperfectly competitive producers. So the marginal product of capital in our simulations is positive, even when the safe rate of return is negative.

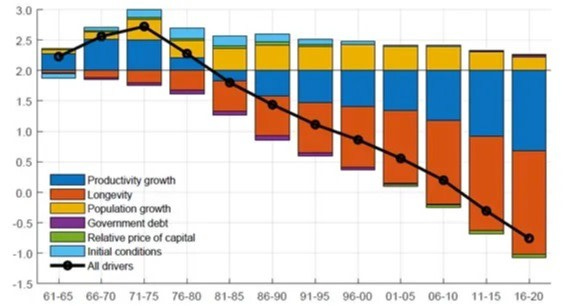

Chart 2 presents a decomposition of the change in Global R* from our model simulations.

The estimated decline in Global R* from its peak has been primarily driven by changes in longevity and productivity growth. Increased longevity, due to falling mortality rates in particular for over-65s, induced a greater accumulation of wealth to finance longer periods of retirement. These higher desired wealth holdings have in turn reduced Global R*. Slower trend productivity growth has also reduced Global R*, since lower expected returns on investment have reduced the demand for capital.

They conclude by implying that low long-term neutral rates are here to stay:

Our simulations imply that increased longevity and slowing productivity growth have resulted in a large fall in Global R*. As noted earlier, forecasting global trends is notoriously difficult. Some of these drivers could reverse, and new forces could emerge to offset them. Nevertheless, the global rise in longevity is not expected to unwind, and so its effect on Global R* is expected to persist.