Perspective on Risk - May 31, 2023

Real Estate; Welcome Back, Examiners From Hell; Vector of Instability; Long Live Libor; R**; I guess Credit Suisse Didn't Fail, and There Was No Government Intervention

Real Estate

I’ve written for months that the commercial real estate industry was in for pain; the pain has begun.

Commercial Anecdotes

Office Owners Dump Lesser Buildings for Whatever They Can Get (WSJ)

RXR defaulted on the $240 million loan on its 33-story office tower in lower Manhattan. The developer, which owns and manages dozens of commercial and residential properties in the New York City area, has said that it will turn over ownership of the office tower at 61 Broadway to whoever buys the defaulted debt. That mortgage is being marketed by commercial real-estate services firm JLL and will likely go for about half the $440 million valuation of the building in 2016, market participants said.

Silverstein Properties, best known for its redevelopment of the World Trade Center, has agreed to sell a 20-story office building on Fifth Avenue near Bryant Park for $105 million, or $66 million less than the amount that Silverstein refinanced the building for in 2020.

Blackstone also recently sold a 49% stake in One Liberty Plaza valuing the tower at $1 billion, down from the $1.5 billion valuation when Blackstone bought the stake in 2017, according to people familiar with the matter.

The Fed thinks there is more to come. From the May minutes:

The staff noted that the CRE sector remained vulnerable to large price declines. This possibility seemed particularly salient for office and downtown retail properties given the shift toward telework in many industries. The staff also noted analysis that found that while losses to CRE debt holders could be moderate in aggregate, some banks and the CMBS market could experience stress should prices of these properties decline significantly.

Residential

Residential real estate has held up comparatively well. This is because there is a lack of sellers due to owners ability to continue to hold the properties having financed them at ridiculously low rates. Simply, this is a supply-constrained market ATM.

Zillow, Redfin and Realtor.com all provide the most timely data. They all have certain biases, but that is not relevant for seeing the overall trend. They all show that price APPRECIATION has stalled, but we are not seeing the major declines as in CRE.

The Fed is watching residential; it probably doesn’t need/want to see falling prices, but it certainly doesn’t want to see further appreciation.

While we expect lower rents will eventually be reflected in inflation data as new leases make their way into the calculations, the residential real estate market appears to be rebounding, with home prices leveling out recently, which has implications for our fight to lower inflation,” Bowman said Wednesday at a Fed Listens event in Boston.

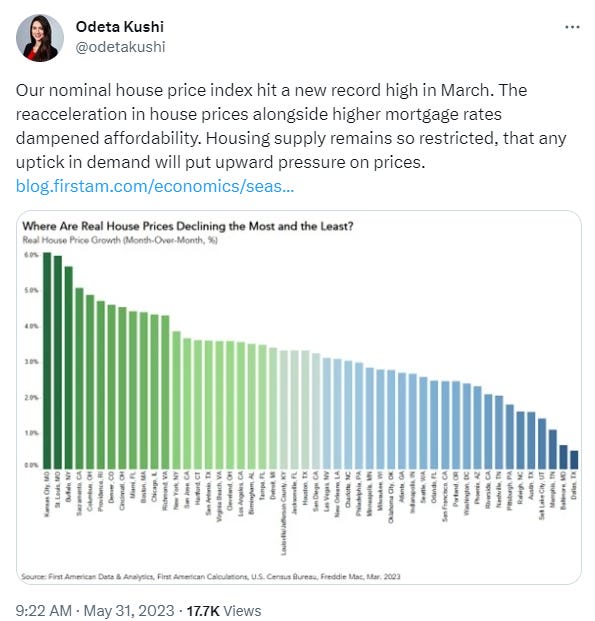

First American says there is a reacceleration in home prices. Not good for those who want the Fed pause to extend or reverse.

Realtors are seeing continued demand.

Welcome Back, Supervisors From Hell

The OCC is nothing if not transparent. We stated following the recent failures that the normal response is to crank up the examination engine, whether it is warranted or not. It was clear in Barr’s remarks, and now the OCC has put it in writing, issuing revisions to its guidance on bank enforcement actions: PPM 5310-3 Bank Enforcement Actions and Related Matters. They key here is a new Appendix C that discusses how to address banks with greater than $50 billion that exhibit ‘persistent weaknesses.’ However, they may apply it more broadly:

In addition, it applies to other banks with operations that are highly complex or otherwise present a heightened risk throughout the bank. … In its discretion, the OCC may apply this framework, including the restrictions discussed below, to any bank.

There is a presumption of escalation.

The OCC has a presumption in favor of additional and increasingly severe action(s) when a bank has continuing, recurring, or increasing deficiencies for a prolonged period, particularly when a bank has not made sufficient progress toward correcting the deficiencies. If a bank exhibits persistent weaknesses, the OCC will consider additional actions, such as assessing CMPs [civil money penalties] and issuing other enforcement actions against the bank, consistent with this presumption. A resulting enforcement action may include requirements or restrictions such as one or more of the following:

a requirement for the board to oversee the development and implementation of an enterprisewide action plan to promptly resolve the bank’s persistent weaknesses, including to improve composite or component ratings or quality of risk management assessments.

restrictions on the bank’s growth (overall or in discrete areas), business activities, or payment of dividends.

requirements for the bank to take affirmative actions, including making or increasing investments targeted to aspects of its operations or acquiring or holding additional capital or liquidity.

None of this is new. Nothing wrong in any of this, but the signaling effect to the examiners could result in an over-reaction to the way SVB and the other banks were managed.

Vector of Instability Was From Banks To Crypto

Pretty funny. We all worried about crypto contagion to the banks. Had it backwards. The banks could have taken down stablecoins.

We all knew Silvergate Bank was in crypto. They advertised that they were the ‘gateway to the digital asset space’ and FTX was a major client.

Similarly, we all knew Signature Bank operated Signet, that allowed customers to easily transfer money into and out of crypto. They had $10 billion of crypto deposits at one time.

Now FT Alphaville has inferred that the largest uninsured depositor at SVB was the Circle stablecoin. SVB’s biggest customers, revealed. Kinda

The document appears to indicate that Circle, the stablecoin issuer, was the biggest depositor at SVB. Circle has previously disclosed that it held $3.3bn of its stablecoin reserves with the bank at the time of SVB’s collapse.

Conspiracy theorist will say the Fed bailed out crypto. Not me. I wouldn’t say that.

Libor Is Dead (long live libor)

UK regulator makes 'final call' to switch off Libor (Reuters)

Markets participants have a month to stop using Libor, the tarnished interest rate banks were fined for trying to rig, Britain's Financial Conduct Authority (FCA) said on Wednesday.

Here is the official notice in regulator speak: ARTICLE 23B BENCHMARKS REGULATION – NOTICE SPECIFYING THE EFFECTIVE DATE OF THE PROHIBITION ON USE OF ARTICLE 23A BENCHMARK

R**

Some of you may remember when I first wrote about this in the [XXXX Perspective]. As a reminder, r* is an economist construct that stands for the equilibrium real rate of interest. r** is the neutral real rate of interest conditioned on financial stability. When r** < r* we are in a world of ‘financial dominance’ and the central bank can’t raise rates to where they need to be without breaking the financial system.

Well, the authors have revised the paper: The Financial (In)Stability Real Interest Rate, r**. The authors also wrote a Liberty Street blog post Financial Vulnerability and Macroeconomic Fragility They summarize their work:

The idea of r** is similar to that of stress tests, except that the size of the shock is not fixed. Rather, we ask the question: How large a shock to real interest rates can the financial system take before entering a crisis? Add this shock to the current level of real interest rates, and you have found r**. If the financial system is strong and robust (r** well above current real interest rates), then it may take a really large shock to cause a financial crisis. If the system is very fragile (r** not too far above current rates), then a small increase in rates may be enough. Summing up, the gap between r** and current real rates provides a summary statistic of financial vulnerabilities.

The folks at FT Alphaville like the paper, but question the forward-looking use of the measure:

The problem is that R** cannot in practice actually be used as a way to predict financial disasters. So unless we’re missing something it’s of questionable practical use, beyond as a new conceptual take on an ancient realisation: rate shocks often reveal financial faultlines.

As the paper points out, the modelled R** readings looked comfortably high in the late 1990s — until LTCM suddenly blew up. It was similarly sanguine in the noughties — right up until the global financial crisis erupted.

Credit Suisse CDS

The law and common sense are sometimes at odds.

Credit Suisse Didn’t Fail

CDS Panel Rules Credit Suisse Takeover Not a Bankruptcy Event (Bloomberg)

The Credit Derivatives Determinations Committee said the fire sale of Credit Suisse to UBS Group AG was not a bankruptcy credit event, according to a notice on its website.

And There Was No Government Intervention

The committee last week ruled against a payout query related to the write-down of Credit Suisse’s Additional Tier 1 securities during the March takeover of the lender by UBS Group AG, saying that a so-called governmental intervention credit event hadn’t occurred.

Lesson to never presume you are perfectly hedged.

Also, Will The Last Member Turn Off The Lights

Shrinking CDS committee sparks questions over US$9trn market's future (IFR)

A crucial part of infrastructure underpinning the US$9trn credit default swap market has become shakier this year as the industry body that rules on CDS events has shrunk further in size, raising questions over whether it remains fit for purpose at a pivotal juncture for the market.