Perspectives on Risk - Oct. 14, 2022 (Decoupling)

Some Basic Statistics; Some Say We Are Not Deglobalizing; There Are Frictions to Decoupling; China’s Development of a Domestic Economy; Decoupling Technology; Supply Chains; Payments;

Warning: very long post. If it doesn’t fully display in your email, click on over to the Substack site.

I worry a bit that our thesis on deglobalization is in fact conventional wisdom, and may prove incorrect. It’s on everyone’s lips. Most of you know how much I hate being consensus.

Martin Bandbu write in the FT that The death of globalisation has been greatly exaggerated. He writes:

The global elite gathered at Davos this week for what by all accounts has been a gloomy affair. The head of the IMF, Kristalina Georgieva, set the tone by warning against “geoeconomic fragmentation”. Among business leaders the talk is all about globalisation going into reverse. … So far, the curious thing is that fragmentation can, as Robert Solow quipped about productivity, be seen everywhere but the statistics.

Start with trade, which has grown strongly from the short-term collapse in the early months of the pandemic. As the chart below shows, until the first quarter of this year merchandise trade gave little indication of deglobalisation for rich countries, China, or the 20 biggest economies (advanced and emerging) taken together.

We can make the same observation about financial globalisation. Banks’ total cross-border liabilities peaked in 2008 as the global credit boom turned to bust (see the chart below). But since about 2016 cross-border entanglements …remain near peak levels.

The question, then, would be whether further globalisation within such regional, politically delineated blocs could be as efficient and productive as a literally global integrated economy.

@LizAnnSonders (Chief Investment Strategist, Charles Schwab) tweets lots of useful information, and recently posted this chart showing that the level of world trade remains quite elevated - said another way we haven’t yet seen the effects of deglobalization.

I’m going to start by changing the language I use to describe what I think is underway. Deglobalization may be a bad moniker. It probably has several sub-components:

Cutting Putin/Russia out of the global system

US/China tensions leading both countries to insure supply chains for critical goods are in friendly hands (bifurcation rather than deglobalization)

Protectionism (if things go too far, and countries find the need to stabilize local economies/employment). Here is a recent example in the US.

Deglobalization implies a global process of retrenchment where each country retreats within its borders; instead it appears what we are seeing s a reversal of the period following China’s WTO entry - a conscious decoupling of East and West, and a realignment of geopolitical agreements.

Some Basic Statistics

Let’s set the stage with a review of some basic trade statistics.

“Overall, the value of global trade reached a record level of $28.5 trillion in 2021,” the report says. That’s an increase of 25% on 2020 and 13% higher compared to 2019, before the COVID-19 pandemic struck.

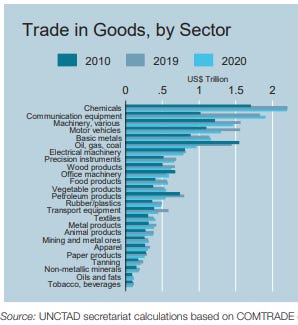

Goods account for $5.8 trillion, while services total $1.6 trillion. Trade in chemicals, communication equipment and machinery are the top sectors.

Reflecting “globalization” and off-shore manufacturing to capture the wage arbitrage, China’s exports tend to be ‘sophisticated’ for their level of GDP, while the US tends to export less sophisticated (aka primary inputs) goods.

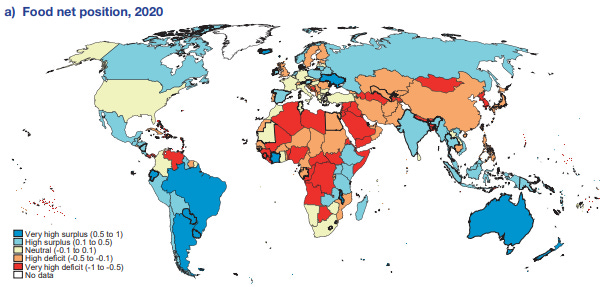

As we discussed in the Sept. 7, 2022 Perspectives, China is a net food importer, with Russia, Brazil and Australia net exporters.

You see a similar pattern in energy.

Some Say We Are Not Deglobalizing

Alan Beattie writes1 in the FT that:

[M]ost standard measures of globalisation — cross-border movement of goods, services, capital, data and people [are] doing pretty well

Wells Fargo published a research note2 concluding that:

Globalization is adapting, not ending or reversing.

There Are Frictions to Decoupling

Alan Beattie further notes that most countries, like India and Brazil, will try and keep relations with both sides. He succinctly describes each sides strengths and weaknesses:

The US has control of the global dollar payments system and the biggest military on earth. But the current phobia of trade deals in Washington limits its ability to reward allies with juicy market access, evidenced by the feebleness of the Indo-Pacific Economic Framework being offered in Asia. … The EU’s a better bet for a meaningful trade deal, assuming you don’t mind it hedged around with increasingly restrictive rules on the environment and labour rights. But it has little unified military capability to underpin a strategic alliance.

China is a big commodities export market, the source of key industrial inputs like rare earths and a provider of infrastructure through the Belt and Road Initiative — assuming you consider that a bonus. But the renminbi isn’t an internationalised currency, and Beijing’s belligerent foreign policy alarms countries in the region.

Wells Fargo notes:

We do foresee a bipolar competition in the coming decade between China and the U.S., but their economic symbiosis is deep and the evidence suggests that the link will be difficult to break.

Thinking more broadly about trade, U.S.-China economic and political competition seems set to increase, but this is very different from the economic and political separation that characterized the U.S.-Russia standoff that during the Cold War.

China’s Development of a Domestic Economy

Economists have noted for a while that China needed to move away from an export-led economic model to one that emphasized more domestic consumption. As a result, the statistics show that China has been “deglobalizing” since 2006.

Importantly, China’s exports have continued to grow, just at a slower rate than the domestic economy.

Pettis argues that China hasn’t gone nearly far enough to create a consumer-led economy, and argues that the Chinese are locked in to a model where consumers subsidize government and businesses. Tweet thread.

Decoupling Technology

The US has recently taken some very strong actions to restrict Chinese access to Western technology. These go beyond the restrictions the Trump administration implemented against Huawei.

Jordan Schneider at the ChinaTalk substack3 points us to remarks4 by National Security Advisor Jack Sullivan; he highlights these remarks, calling them "the Sullivan doctrine:"

Fundamentally, we believe that a select few technologies are set to play an outsized importance over the coming decade.

Computing-related technologies, biotech, and clean tech are truly “force multipliers” throughout the tech ecosystem. And leadership in each of these is a national security imperative.

On export controls, we have to revisit the longstanding premise of maintaining “relative” advantages over competitors in certain key technologies. We previously maintained a “sliding scale” approach that said we need to stay only a couple of generations ahead.

That is not the strategic environment we are in today.

Given the foundational nature of certain technologies, such as advanced logic and memory chips, we must maintain as large of a lead as possible.

Greg Allen at CSIS has a good article summarizing the US/West’s new export controls on semiconductors: Choking Off China’s Access to the Future of AI.

With the new policy, which comes on the heels of the CHIPS Act’s passage, the United States is firmly focused on retaining control over “chokepoint” (or as it is sometimes translated from Chinese, “stranglehold”) technologies in the global semiconductor technology supply chain.

In short, the Biden administration is trying to (1) strangle the Chinese AI industry by choking off access to high-end AI chips; (2) block China from designing AI chips domestically by choking off China’s access to U.S.-made chip design software; (3) block China from manufacturing advanced chips by choking off access to U.S.-built semiconductor manufacturing equipment; and (4) block China from domestically producing semiconductor manufacturing equipment by choking off access to U.S.-built components.

The targeted nature of the Biden administration’s actions here suggests three important implications about its worldview.

First, the United States believes that China is willing to take extraordinary measures—including but not limited to spending hundreds of billions of dollars, hacking U.S companies, and creating networks of shell companies—in order to evade export controls and free itself from dependence on U.S. semiconductor supply chains.

Second, … the United States is wielding its power forcefully, but at a limited set of Chinese targets, in order to preserve U.S. chip power and leverage over the long term.

Third, this policy signals that the Biden administration believes the hype about the transformative potential of AI and its national security implications is real.

Ben Thompson, who writes the excellent Stratergy substack, notes that the bifircation in technology has been underway for a while, and started due to the Great Chinese Firewall. He highlighted back in 2018:

The other major impact of both the trade war and this action against ZTE will be the further bifurcation of Chinese and Western technology; already there is a major separation at the services layer: Facebook/WeChat, Google/Baidu, Amazon/Alibaba, etc. No, they aren’t perfect comparisons (particularly Amazon and Alibaba), but they are symbolic of how the Great Firewall has resulted in two Internets.

What seems likely to happen in the long run is a separation at the hardware layer as well; China is already investing heavily in chips, and this action will certainly spur the country to focus on the sort of relatively low-volume high-precision components that other countries like the U.S., Taiwan, and Japan specialize in (to date it has always made more sense for Chinese companies to focus on higher-volume lower-precision components). To catch up will certainly take time, but if this action harms ZTE as much as it seems it will I suspect the commitment will be even more significant than it already is.5

Summarizing recent developments6, he notes:

This gets to the big takeaways from this announcement.

First, in case there was any question, it is clear that China is being viewed as an adversary, and that that view is a bipartisan one.

Second is the point I started with: while Trump deserves credit for upsetting the apple cart in terms of conventional wisdom with regards to China relations, the Biden administration is correct to pursue those previous actions to their logical conclusion.

what is significant about this move is not simply that it bans chips but it also bans equipment as well (and, given the restrictions it places on U.S.-persons, also bans the service of existing equipment).

Will China retaliate, and if so where?

The Belfer Center for Science and International Affairs (Harvard Kennedy School) issued a report last December The Great Tech Rivalry: China vs the U.S that summarized the state of play in six areas, concluding.

China has become a serious competitor in the foundational technologies of the 21st century: artificial intelligence (AI), 5G, quantum information science (QIS), semiconductors, biotechnology, and green energy. In some races, it has already become No. 1. In others, on current trajectories, it will overtake the U.S. within the next decade.

It specifically cites 5G and green energy as areas where China arguably leads:

In 5G, according to the Pentagon’s Defense Innovation Board, “China is on a track to repeat in 5G what happened with the United States in 4G.”12 Despite advantages in 5G standards and chip design, America’s 5G infrastructure rollout is years behind China’s, giving China a first-mover advantage in developing the 5G era’s platforms.

Though America has been the primary inventor of new green energy technologies over the past two decades, today China is the world’s leading manufacturer, user, and exporter of those technologies, cementing a monopoly over the green energy supply chain of the future. Consequently, America’s green push relies on deepening its dependence on China.

In fact, China accounted for more than half of all global EV registrations in 2021.

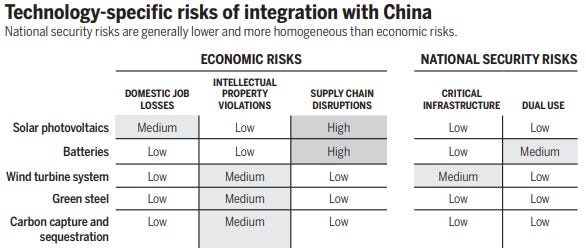

Davidson, Karplus, Lewis, Nahmand and Wang have an interesting paper in Science titled Risks of decoupling from China on low-carbon technologies ($30 paywall)

Calls to decouple from China’s economy would have considerable implications for the future of clean energy technology and the ability to meet climate goals. At present, China accounts for roughly three-quarters of global production capacity for lithium-ion batteries, two-thirds of production capacity for solar PV, and a sizable share of manufacturing capacity for wind turbines and their components.

Given the realities of expected deepening political contests between the United States and China and the real risks of shocks to globalized supply chains, it is increasingly important to manage these risks while recognizing the benefits of integration. Across numerous technology areas, the level of integration is so great that true decoupling would be nearly impossible and potentially counterproductive to national interests.

[W]e highlight five primary risks to integration—separated into their economic and national security implications—and apply them to five leading low-carbon technologies: solar, wind, batteries, “green” steel, and carbon capture and sequestration (CCS).

In contrast to semiconductors, these do not appear to represent national security risks, so I would assume it would be in China’s interest to continue a mercantilist approach.

Decoupling/Realigning Supply Chains

China, of course, has one critical advantage at the moment. It actually produces many of the final goods used in the world. Western companies have exploited the labor arbitrage from globalization, and many supply chains now rely greatly on Chinese manufacturing. Two recent examples of the trend underway:

Kuo: Here’s Apple’s roadmap for shifting more iPhone and Mac production outside of China (9to5Mac)

According to Kuo, Apple is adjusting its “supply chain management strategy” in response to the ongoing “de-globalization trend.” Based on recent supply chain surveys, here’s what Kuo predicts…

Honda considering decoupling supply chain from China -Sankei (Reuters)

Nearly 40% of Honda's automobile production took place in China in the last financial year. … Honda would continue to keep its supply chain in China for the domestic market in the world's second-largest economy, while building a separate one for markets outside of China

Still, there has been little direct evidence in the statistics as of now.

Decoupling Payments

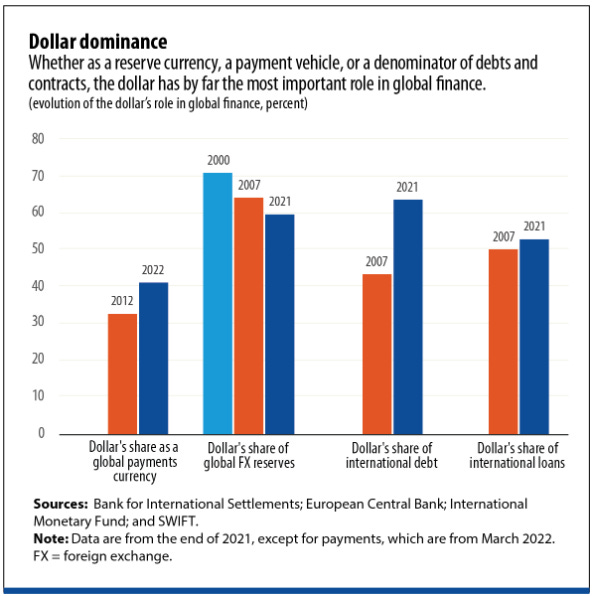

The constant ‘concern’ in the commentariat is that the dollar is/will lose its dominance.

Gourinchas, Rey & Sauzet argue that the centrality of the dollar is fragile as:

With a shrinking share of world output, the United States cannot indefinitely remain the sole supplier of safe assets to the world.7

Adam Toose has a great way of thinking about why this is so:

(2) The world is multipolar and so is global trade. Western policy must adjust to that.

(3) There is a huge asymmetry in the world right now between the financial system that remains spectacularly euro-dollar centered and the new multipolarity of power, trade and economic activity.

(4) Given this asymmetry there is a fascination in the cultural and political sphere with the way this glaring asymmetry could be overcome.8

China has a long way to go until global investors will be comfortable transacting principally in Renminbi.

Still, there are some minor cracks worth watching as Russia and China seek to avoid the weaponized US dollar. These observations below are almost entirely due to Russia looking to weaken its currency.

Gazprom to Shift Gas Sales to China to Rubles, Yuan From Euro (Bloomberg)

The state-run gas giant signed an additional agreement to its existing contract with China National Petroleum Corp. on the issue Tuesday, Gazprom said in a statement. Payment will be made 50% in rubles and 50% in yuan, effective immediately, according to a person familiar with the plans who spoke on condition of anonymity to discuss matters that aren’t yet public.

Russia Mulls Big Purchases of ‘Friendly’ FX to Stem Ruble’s Rise (Bloomberg)

Russia is considering a plan to buy as much as $70 billion in yuan and other “friendly” currencies this year to slow the ruble’s surge, before shifting to a longer-term strategy of selling its holdings of the Chinese currency to fund investment.

Russia's top banks have started lending out yuan and transferring China's currency outside the SWIFT system (Markets Insider)

Sberbank said Tuesday it has started lending out money in yuan as it looks to replace dollar and euro transactions.

VTB also said Tuesday that it is the first Russian bank to launch money transfers to China via the yuan outside the SWIFT messaging network, which is the backbone of the global financial system.

Again, the dollar has at least three key strategic advantages:

Liquidity of dollar-denominated assets

Convertibility

Robust financial institutions and strong legal framework not subject to sovereign whims and interference9

A deeply embedded ecosystem for billing and transactions.

Anyway, if you’ve made it this far, I’ve run out of words.

The de-globalization fallacy, Wells Fargo

Schneider, New Chip Export Controls and the Sullivan Tech Doctrine with Kevin Wolf, ChinaTalk substack

Sullivan, Remarks by National Security Advisor Jake Sullivan at the Special Competitive Studies Project Global Emerging Technologies Summit

Thompson, The ZTE Ban, Tech’s Trade War Risk, China’s Delayed Approval and Apple’s Pain, Stratergy

Thompson, The China Chip Ban; The Logic of the Ban; Chinese Retaliation, or Not, Stratergy

Gourinchas, Rey & Sauzet, THE INTERNATIONAL MONETARY AND FINANCIAL SYSTEM, NBER

Or as Toose puts it:

What holds the actually existing system of global finance together is not so much the dollar - pure and simple - so much as the sinews of finance, law and contractual construction knit by key players above all in Wall Street and - as Katharina Pistor has taught us - in London. The systems of English law and the legal code of the state of New York, are the preeminent codes for big debt deals.