Perspective on Risk - May 4, 2023 (Bank Supervision; LCR)

Bank Supervision; Applying the LCR; Credit Cycle; Counterfactual Credit Suisse History; A Bloomberg Take on Barr Report; CAT Modeling; InfoSec; Treasury Buyback; HF Loss Reporting; Wirecard

For my new subscribers

Perspective on Risk - April 28, 2023 discusses the Fed’s Barr Report

Perspective on Risk - May 1, 2023 discusses the FDIC’s Signature report

Perspective on Risk - May 3, 2023 discusses the NYDFS’s Signature report

Too-Big-To-Fail > Too-Small-To-Survive

Bank Supervision

Had a conversation with a former colleague who was also a very senior supervisor. Good, far ranging discussion, that reminds me there is some context that I have left out about supervision for my previous messages. This involves process focus, supervisory metrics, and dialogue with management.

On-site supervisors focus on process

The first observation is on what examiners are comfortable talking about. Start by remembering that most examiners join the Fed and the other agencies out of school; there are less with banking experience, and when they do come from industry, they were often in 2nd or 3rd line roles.

As such, most examiners are much more comfortable talking about process weaknesses rather than absolute levels of risk. Each of the reports indicated that the examiners identified weaknesses in the liquidity or interest rate management process. In the case of SVB, they noted that management consistently breached the firm’s internal limits. But none of them said that the examiners determined that the level of risk was excessive. Examiners hesitate to impose their judgment over senior bankers, and will generally let the firms take the risk as long as it is internally transparent to the proper individuals, including the Board.

Again, it is much easier for an examiner to get their management’s agreement that a process needs enhancement than that the absolute risk level is too high. And even if they succeed at convincing their management, picture a young MBA trying to convey this to Jamie Dimon and the JPM Board.

In my time at the Fed, I can only think of a handful of times the on-site examiners expressed concern about the absolute risk level. More often, it would be off-site staff that were monitoring the entire industry that would raise concerns about the level of risk at individual firms.

Supervisory metrics

A second issue is that SVB failed economically, and not on the supervisory metrics. Examiners in some way are constrained by the flawed metrics that are used to calculate regulatory capital and liquidity (more on the LCR below). It is difficult, but not impossible, for an examiner to say “while this bank looks fine on our supervisory capital metric, we are concerned about the firm’s real solvency.” Firms are closed and actions taken under law when they breach the supervisory metrics. The examiners are forced to use the tools they have, particularly if the firm’s internal metrics for capital adequacy and the rating agency metrics pass the test.

Dialogue with the banks

Typically, examiners will convey their exam findings to management as they complete a target, significantly before they send the actual letter conveying the findings. Some firms welcome the examiner feedback, but others are assholes and treat examiners with distain. The examiners will generally avoid confrontation unless they are backed up by their management team. And as was stated in many of the reports, the “vetting” of the findings typically happens after the target exam has been completed and while the letter is being written. It takes an experienced and confident senior examiner to have a direct and blunt conversation with management (at which point they will often hear back from their management after the bank complains!).

When it comes to telling a bank that they need to raise their capital or liquidity levels, this conversation will have to happen at a more senior level; in my experience this can happen at levels from the examiner’s manager all the way up to the Reserve Bank president.

Applying the LCR to SVB, First Republic and Signature Bank

One policy proposal that is being bandied about is whether the Liquidity Coverage Ratio (LCR) should be applied to a broader set of banks.

Silicon Valley Bank

There are differing views as to whether SVB would have passed the LCR’s test. The difference is in assumptions they use to classify outflows, and in whether SVB would be held to the 75% or 100% standard.

Bill Nelson writes that Silicon Valley Bank Would Have Passed The Liquidity Coverage Ratio Requirement

SVB would have had $52.8 billion in HQLA for LCR purposes.

Estimated net cash inflows is $50.3 billion, or $35.2 billion after multiplying by 70 percent.

SVB’s LCR would therefore have been 150 percent ($52.8 billion/$35.2 billion) on Dec. 31, 2022. The requirement is that the LCR be equal to or above 100 percent.

However, in Lessons from Applying the Liquidity Coverage Ratio to Silicon Valley Bank (Yale) the authors suggest SVB would have failed the test:

We made the following different assumptions: assuming the company would be subject to the full 100% LCR; defining the bulk of SVB’s nonfinancial business customers as wholesale, rather than small business-cum-retail, per the Y-15; finding that the bulk of SVB’s loans would not provide much cash inflows over a 30-day period; and excluding half of inflows from deposits held at other banks, since it’s reasonable to assume much of those would be needed for operational purposes.

Total HQLA: $52.9 billion.

The total cash outflow comes to $73.7 billion.

Cash inflows: $2.8 billion.

The resulting LCR is 75%: 52.9/71.0.

We reviewed SVB’s public financials and concluded that its LCR would have been 75% at the end of 2022, substantially below the threshold. This result suggests that the 2019 tailoring rule was complicit in the run and failure at SVB

Both agree that even if SVB passed the LCR test it would have been insufficient to handle the run.

To be sure, compliance with the LCR alone would not have saved SVB’s management from its mistakes managing interest-rate risk in the bank’s massive, long-dated portfolio of agency mortgage-backed securities (MBS). If faced with the LCR rule two or three years ago, they could have simply shifted from long-dated MBS to long-dated Treasuries—bringing their LCR in compliance while staying extraordinarily exposed to rising rates.

Signature Bank

As discussed in the last Perspective, the NYDFS implies that Signature Bank would have complied with the LCR test.

The rapid collapse of Signature underscores the need to revisit the assumptions used to model and manage liquidity risk. In particular, both the types of Signature’s depositors that ran and the speed at which they initiated withdrawals far outpaced assumptions many institutions use to model and assess liquidity risk.

The mismatch between recent lived experience and defined regulatory expectations is apparent when considering recent depositor behavior versus the mandated assumptions of the liquidity coverage ratio (“LCR”).

The observed behavior of Signature’s depositors beginning on March 10 did not align with these [LCR’s] assumptions, in many instances exceeding them, despite the fact that the rule is intended to provide a uniform and conservative liquidity risk-management framework.

First Republic

The Fed’s Barr report states:

An analysis of SVBFG’s December 2022 capital and liquidity levels against the pre-2019 requirements suggests that SVBFG would have had to hold more high-quality liquid assets (HQLA) under the prior set of requirements. For example, under the pre-2019 regime, SVBFG would have been subject to the full LCR and would have had an approximately 9 percent shortfall of HQLA in December 2022, and estimates for February 2023 show an even larger shortfall (approximately 17 percent), which would have required different actions from SVBFG.

Changes are needed to the LCR

The NYDFS states:

In particular, in light of the experience with Signature, regulators should consider whether the assumptions used by regulated banks to classify their deposits (including which types of deposits may be considered “stable” and the appropriate conservative assumed outflow rates) adequately capture the risk such deposits may represent.

From the Yale study:

The LCR as currently written does not distinguish securities by their maturity or recognize that a bank may be reluctant to take losses by selling them.

The lesson is that securities with mark-to-market losses are not perfectly liquid. But the LCR does not distinguish between short- and long-dated securities, or between securities with unrealized losses and securities trading at par. Perhaps the LCR needs a new approach to held-to-maturity securities, or a penalty for assets that you can't sell without a loss. Alternatively, the LCR could require banks with concentrated uninsured deposits to hold a portion of their HQLA in reserve balances and short-term Treasuries. There are many options to insert maturity and potential losses into the calculation.

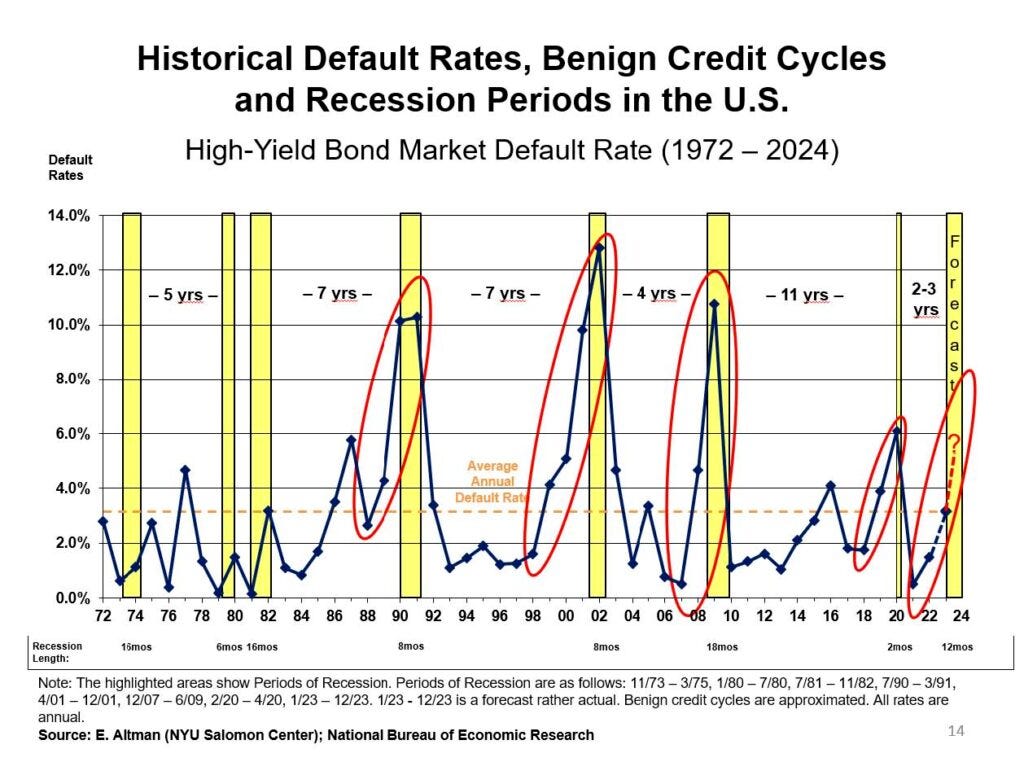

Altman on the Credit Cycle

Professor Ed Altman on Where We Are In The Credit Cycle

My current assessment is that the Benign credit cycle we have enjoyed since 2010, with the exception of a few months in early 2020, is over.

We recently reached an inflection point to an Average credit risk scenario. The later assessment is based on a number of historical indicators over the last 60 years.

This conclusion is tempered by the strong likelihood that the U.S. credit picture will continue its heightened risk trend toward a Stressed scenario by year’s end, and if we continue to incur unexpected shock catalysts, similar to the recent Crypto and Silicon Valley Bank and other banking meltdowns, combined with a “hard-landing” economic recession, we could witness another financial-credit crisis, with non-financial corporate risky debt default rates rising to perhaps 10%, or more, over one or two years.

Our forecast is a 2023 HY Bond Default Rate of just about the historical average of 3.5%. This forecast is actually fairly conservative compared to other forecasters, namely the various rating agencies, e.g. Moody’s is 5.2%, KBRA’s rate is 4.5%, Fitch’s rate is 3.5%, S&P’s current forecast is 4.0%. Fitch and KBRA’s rate is dollar based rate, as is our forecast, while Moody’s and S&P are issuer based.

Counterfactual Credit Suisse History

Reuters BreakingViews imagines how a resolution of Credit Suisse would have played out in Resolving Credit Suisse: an alternative history.

Though regulators have designed systems for winding down or shoring up big lenders after the 2008 financial crisis, they had never been tested in real life. FINMA insists that one of the first steps in a resolution is converting $64 billion of bonds issued by Credit Suisse into equity, creating a buffer to fund any losses incurred during the subsequent restructuring.

Adding together the equity, bail-in bonds and funky hybrid instruments, it has about $110 billion of total loss-absorbing capacity against a $605 billion balance sheet. That implies uninsured depositors and other senior creditors will be untouched even if almost one-fifth of the assets go up in smoke.

Angehrn explains how a Credit Suisse resolution will work. FINMA will wipe out the bank’s existing shares and hybrid debt instruments, and then convert the $64 billion of bail-in bonds to ordinary shares. This will cover any losses incurred during a FINMA-supervised breakup. It also enables the Swiss National Bank to offer Credit Suisse an open-ended credit line, hopefully ending the bank run.

Next will come a restructuring designed to keep any viable bits of the bank going and wind down the rest. Credit Suisse’s Swiss unit will be carved out and run as a separate entity. The investment bank will be closed. … Meanwhile FINMA will shop Credit Suisse’s asset-management unit around to possible suitors. That leaves international wealth-management, a once-proud business that had seen almost $160 billion of client outflows in the past six months.

A Bloomberg Take on Barr Report

Mark Rubenstein writes in You Don’t Want to Know How Banks Make Their Sausage

One thing they reveal is how haphazardly these institutions were run compared with the super-professional show they put on for investors.

You’d have thought Silicon Valley Bank — a tech bank focused principally on the tech sector — would have had good tech. Not so. In a May 2021 letter to the board, [regulators] observed that “SVB’s overall IT function is less-than-satisfactory.” … “The IT function continues to deteriorate and is now a supervisory concern,” it concludes.

Or take risk management … “When you think about the growth I talked about a few minutes ago,” Silicon Valley Bank Chief Executive Officer Greg Becker told shareholders at a presentation in 2018, “growing 400%, 500% in 7 years — you have to make sure that your risk management systems and structures are as robust as possible.” Yet, according to the Fed, they weren’t. Three years after that statement, Fed supervisors found that … “risk-management practices had not kept pace with its growth.

Evidence also emerges about how flaky management was when it came to modeling its business. The Fed now discloses that “SVBFG had breached its long-term interest rate risk limits on and off since 2017.” In response, “in April 2022, SVBFG made counterintuitive modeling assumptions about the duration of deposits to address the limit breach rather than managing the actual risk.”

The thing is, Silicon Valley Bank may not be alone here

Yeah, its not. Trust me.

Catastrophe Modeling

Catastrophe modeling used to be about wind damage. But over the last few years, storm surge has received much more attention as a driver of losses. Because of this, NOAA upgrades model to improve storm surge forecasting.

Today, NOAA upgraded its Probabilistic Storm Surge (P-Surge) model — the primary model for predicting storm surge associated with high-impact weather like hurricanes and tropical storms — to version 3.0. This upgrade advances storm surge modeling and forecasting for the contiguous U.S. (CONUS), Puerto Rico and the U.S. Virgin Islands, and comes just in time for the 2023 hurricane season beginning on June 1 and running through November 30.

The upgrade includes a number of new capabilities that will help forecasters better understand the risk of storm surge, such as:

New forecasts for surge, tide and waves for Puerto Rico and the U.S. Virgin Islands.

The ability to run the model simultaneously for two storms. This capability can help during two landfalling storms impacting the CONUS, or one storm impacting the CONUS and one impacting Puerto Rico and/or the U.S. Virgin Islands.

Improved model calculations of friction over different types of land surfaces, which helps more accurately compute the extent of water inundation along the coast.

Information Security

As a non-techy, I am usually quite impressed with the work of the Cybersecurity & Infrastructure Security Agency (CISA). They have developed a a self-attestation form in which software producers serving the federal government will be required to confirm implementation of specific security practices.

Request for Comment on Secure Software Self-Attestation Common Form

Worth making sure the right folks know about this and a way to benchmark your firm against current minimum standards.

Note: Software-as-a-Service (SaaS) now also requires attestation.

Treasury Launching Buyback Program

Treasury to Launch First Buyback Program Since 2000

The U.S. Treasury says it will launch a program for buying back government securities some time next year, a move intended to ease liquidity in the roughly $24 trillion market at the center of the global financial system.

Liquidity in the Treasury market has been constrained by dealer balance sheets in recent years; this would be a way to insure that the Fed can get sufficient cash into the right hands when needed.

Hedge Fund Reporting

Big Hedge Funds Face New 72-Hour Deadline to Report Major Losses (Bloomberg)

Large hedge funds would have just three days to privately tell US regulators about extraordinary investment losses and major margin events under a new rule that’s set to be approved by the Securities and Exchange Commission.

Wirecard

Most of you could care less about this, but I find it fascinating.

EY banned by German audit watchdog over Wirecard work (FT)

EY has been banned from taking on any new listed audit clients in Germany for two years over failures in its work for collapsed payments company Wirecard.

In a statement on Monday morning, Apas said it “considered violations of professional duties during the audits of Wirecard and Wirecard Bank from 2016 to 2018 as proven”, without giving further details of the violations.

According to people familiar with the regulator’s thinking, there has not been a formal decision about whether EY acted with intent or just with negligence, which will be a key question in deciding the firm’s criminal and civil liabilities.

Wirecard boss threatened ‘legal steps’ against KPMG over special audit (FT)

“There were multiple attempts to influence us,” said Leitz, adding that in January 2020 Wirecard had sought the replacement of key KPMG team members who had vehemently pushed for access to data, a request KPMG ignored.

When the Wirecard boss was briefed about KPMG’s findings, he said “you failed to prove that the money does not exist”, according to Leitz, who said he had responded to Braun that “you failed to prove to us that the money is there”.