Perspective on Risk - April 28, 2023 (Review of SVB Supervision + much more)

Review of the Fed’s Supervision of SVB; Managing A US Debt Default; BoJ Financial Stability Report; Revised FSOC Framework; CAT Rates Increasing; Deriving ERP From Options; Factor Information; Munchie

Disclaimer

As background for my newer readers, for 20+ years I worked in Bank Supervision for the Federal Reserve Bank of New York. My last role was as SVP responsible for about 200 risk specialists. I was involved in supervising the largest banks in the country up to and through the 2008 GFC. I was also one of the primary developers of the RFI supervisory rating scale1 used for bank holding companies that is referred to in the report. I was also instrumental in developing the ‘target exam’ approach referenced herein.

My take on the report may be a little different from the more salacious press reports. I hope this provides you with some insight. Here is my initial take after a first read-through. I am sure my views may evolve.

If you are new here, you may first want to read this below link where I have some initial thoughts based on Barr’s remarks.

Perspective on Risk - March 28, 2023 (The Supervision of SVB)

Review of the Federal Reserve’s Supervision and Regulation of Silicon Valley Bank

The Federal Reserve has released its Review of the Federal Reserve’s Supervision and Regulation of Silicon Valley Bank.

My Major Conclusions

I did not see any discussion of why SVB was not ex-ante identified as ‘systemic’ and who was responsible for making that determination. This IMO is the big issue and it is not addressed at all.

The rapid growth of SVB was a clear red-flag that was perhaps appreciated at the firm-specific micro level, but missed in the larger context that should have driven an even more aggressive Fed response.

The on-site examiners from the FRBSF seem to have made the correct and timely determinations in almost all cases (they may have missed more aggressively raising interest rate risk concerns).

There was a clear failure to issue a supervisory action (a Memorandum of Understanding or MOU) in a timely manner once the on-site examiners made their findings. Barr dances around why this took so long, especially as SVB was identified as a poster-child for interest rate and deposit risk in a presentation to the Board of Governors. It is also deeply concerning that an earlier MOU was “subsequently dropped the matter because they felt it would not be pursued by policymakers at that time.”

The call to “develop a culture that empowers supervisors to act in the face of uncertainty” has been made before, but is antithetical to a culture that prioritizes getting findings correct and treating firms in an equivalent manner. Changing the culture here would raise a different set of risks.

The discussion and blaming of the Economic Growth, Regulatory Relief, and Consumer Protection Act is a bit of a canard. The Fed did exactly what is correct in tailoring supervision to the risk a firm poses to the financial system. Resources devoted to small non-systemic firms are resources not devoted to systemic risks. Again, the miss was in identifying the supposed systemic risk.

I’m going to provide my comments sequentially in the order the report was written.

Executive Summary

At the core of the Federal Reserve’s oversight framework is the expectation that boards of directors of supervised firms provide effective oversight, and that management is responsible for daily and operational decisions. Supervisors assess the effectiveness of those individuals and the bank’s risk-management processes but do not manage or run the banks. The objectives of boards and management are not perfectly aligned with those of the public, which is why prudential oversight through supervision and regulation is essential.

This opening statement is important context to understand. This is how the Fed trains its examiners and officers to think about supervision. In saying that supervisors “do not manage or run the banks” it defacto leads supervisors to identify issues, but not tell the banks how the issues must be fixed.

The lack of “perfect alignment” of bank interest with the public is reflected in the “tailoring” of supervision to firm size and complexity. Misalignment occurs when a firm’s failure has negative externalities. This perspective is probably stronger in Fed supervision than it is at other regulatory agencies (OCC, FDIC).

It rightfully starts by putting the majority of the blame on SVB, its management, and its Board of Directors.

Silicon Valley Bank (SVB) failed because of a textbook case of mismanagement by the bank. Its senior leadership failed to manage basic interest rate and liquidity risk. Its board of directors failed to oversee senior leadership and hold them accountable.

And then turns inward:

And Federal Reserve supervisors failed to take forceful enough action

Our first area of focus will be to improve the speed, force, and agility of supervision. As the report shows, in part because of the Federal Reserve’s tailoring framework and the stance of supervisory policy, supervisors did not fully appreciate the extent of the bank’s vulnerabilities, or take sufficient steps to ensure that the bank fixed its problems quickly enough.

The Fed’s focus has long been to prioritize “getting the findings/rating correct” and “treating firms consistently.” To this end, there has long been layers of “vetting” of the findings. This is further complicated by the frequent need to reach agreement with the state bank supervisors that participate on the exams. Over time, this vetting process has expanded as the DC Board staff exerted increased influence. This is not a bad thing, just a choice of accuracy over speed.

We need to develop a culture that empowers supervisors to act in the face of uncertainty. In the case of SVB, supervisors delayed action to gather more evidence even as weaknesses were clear and growing. This meant that supervisors did not force SVB to fix its problems, even as those problems worsened.

So this is the opposite of the culture that the existing rules promote. Examiners are aware that findings and ratings can be “appealed” either informally (calling more senior Reserve Bank staff or DC) or formally (by asking for an appeal).

This causes me to remember a press brouhaha around Goldman Sachs and a Federal Reserve Bank of NY examiner named Carmen Segarra. Ms. Segarra was an examiner that raised a number of issues about how GS handled conflicts of interest. Messages were release that purported to show Ms. Segarra’s findings being over-ruled by the Examiner-in-charge Michael Silva. The press sold the public on the story that GS was being coddled by the Fed, but my reading of the emails showed an EIC looking to get the findings correct, listening to the banks arguments to find balance, and coach the more junior examiner to a more appropriate outcome. In this case, if Ms. Segarra was “empowered to act” we would have likely had a sub-optimal outcome.2

In general, the Reserve Banks are responsible for the assessment of firms, such as SVBFG, in each District as part of delegated authority from the Board. In this arrangement, the Board staff provide input and support in supervision and also provide oversight of the Reserve Banks.

This downplays the reality of Board staff’s role; it makes it seem as if the delegation is greater than is actually the case.

Key Takeaway 1: Silicon Valley Bank’s board of directors and management failed to manage their risks.

It rightfully starts by putting the majority of the blame on SVB, its management, and its Board of Directors.

Silicon Valley Bank (SVB) failed because of a textbook case of mismanagement by the bank. Its senior leadership failed to manage basic interest rate and liquidity risk. Its board of directors failed to oversee senior leadership and hold them accountable.

The full board of directors did not receive adequate information from management about risks at SVBFG and did not hold management accountable.

The board put short-run profits above effective risk management and often treated resolution of supervisory issues as a compliance exercise rather than a critical risk-management issue.

This is fairly standard Fed approach; put the onus on the board, and subsequently management, for failures. In this case, as will be evidenced later, this was not just ex-post rationalization; the Fed had put the board and management on notice.

One issue that might have been at play is the reluctance of management to understand the need to change; that the practices that worked in the past were not sufficient for the current size and scope.

There is additional anecdotal information, not in this report, that management (and perhaps the board) was disdainful of supervision and actively tried to avoid it. This in and of itself is a red flag and a sign of management immaturity.

Key Takeaway #2 - Supervisors did not fully appreciate the extent of the vulnerabilities as Silicon Valley Bank grew in size and complexity.

It appears to me that the field examiners mostly got things right:

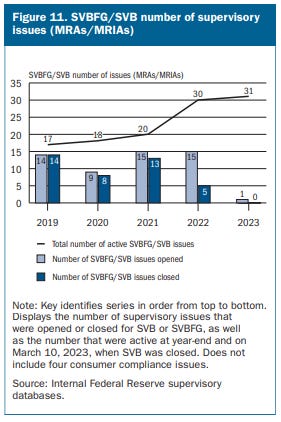

SVBFG had 31 open supervisory findings when it failed in March 2023, about triple the number observed at peer firms. The supervisory findings at SVBFG included core areas, such as governance and risk management, liquidity, interest rate risk management, and technology.

It is clear from the above table that there was a material increase in supervisory findings once SVB moved to the more-aggressive LBO supervision.

Table 2 indicates that there were a large number of the more significant ‘Matters Requiring Immediate Attention’ issued on governance and control issues. Liquidity risk management was flagged as an MRIA back as far as Nov. 2021.

May 2022 saw the issuance of a number of very significant MRIAs. These are three of the most significant types of supervisory findings that the Fed can make. The firm and its board was clearly on notice that there were significant deficiencies.

[S]upervisors assessed SVBFG … Governance and controls: “Deficient-1,” a rating that is less than satisfactory.

This is perhaps the most critical ratings component, and one that is less of a mechanical call and requires more examiner discretion.

When SVBFG moved to the LFBO portfolio, supervisors recognized that SVBFG’s risk management was not robust and proceeded to build evidence, issue MRIAs, and downgrade SVBFG. Governance and Controls were ultimately rated “Deficient-1,” but not until August 2022

This was a downgrade by the new large banking organization (LBO) examiners as compared to the previous satisfactory ratings when reviewed in the Regional Bank Organization (RBO) portfolio.

The examiners seem to have made the correct and timely call downgrading the firm.

Liquidity: “Conditionally Meets Expectations (CME),” a satisfactory rating. Supervisors had informed SVBFG that its “liquidity risk management practices are below supervisory expectations” and identified foundational shortcomings in key areas as part of the issuance of six supervisory findings in November 2021.

I’m not sure ex-ante the examiners could have gone further than this, based on the numbers reviewed back in mid-2022.

But the examiners were not tough enough on interest rate risk. That was a miss, though they probably factored it into the Governance component rating

For IRR, SVBFG was rated as “Satisfactory-2” despite the firm repeatedly breaching its internal risk limits for long-term risk exposure over several years. IRR was not viewed as a material risk at SVBFG until late 2022 and therefore not subject to a thorough examination

It should be doubly-noted that the failure to address this more forcefully is notable since SVB was the poster-child for the interest rate risk of rapidly rising rates.

The Board received a briefing on these topics (the impact of rising interest rates on securities valuation and potential deposit impacts) in mid-February 2023 in which SVBFG was specifically identified as an example of a large firm with “significant safety and soundness risks.”

Key Finding #3 - When supervisors did identify vulnerabilities, they did not take sufficient steps to ensure that Silicon Valley Bank fixed those problems quickly enough.

The time between when exam findings are developed and when they are conveyed formally to management and the board was significantly delayed.

As a result, the supervisory ratings letter, which was based on supervisory work performed over the course of 2021 and the first half of 2022, was jointly issued by the FRBSF and CDFPI on August 17, 2022.

While the typical process is slow, and this is is a long time even by normal historical performance measures, it is perhaps an artifact of the process. Typically, at the largest banks, after each ‘target’ exam the findings are conveyed to management. Then annually, the findings are ‘rolled-up’ into a report that formally conveys any ratings changes. But the process at smaller regional banks may not be as disciplined about conveying the interim results.

[I]t took more than seven months to develop an informal enforcement action, known as a memorandum of understanding (MOU), for SVBFG and SVB to address the underlying risks related to “oversight by their respective boards of directors and senior management and the Firm’s risk-management program, information technology program, liquidity risk management program, third-party risk-management program, and internal audit program.” SVBFG failed before the MOU was delivered.

BIG ISSUE, and Barr dances around the cause.

The root cause of these delays around supervisory actions is difficult to ascertain. Governance issues related to the Board’s approach to delegated authority may play a role. For example, the Board has delegated to the Reserve Banks supervisory authority for firms like SVBFG, including the authority to issue supervisory ratings, but in practice, Reserve Bank supervisors typically seek approval from or consensus with Board staff before making a rating change. Enforcement actions for banks with assets greater than $100 billion are not delegated to Reserve Banks but require

In my experience, there is a tremendous amount of bank-and-forth and vetting’s on supervisory actions. Board supervision staff as well as Board legal staff would be involved. NY had it a bit easier as we had our own powerful Legal function.

A related complication is that the Board provides substantive input to the supervisory process, including the ratings for firms subject to delegated authority, and also acts in an oversight capacity over the Reserve Banks. This creates conflicting incentives for the Reserve Banks that could be an additional force that pushes toward consensus around supervisory judgments.

Again, consensus is not per se bad. Firms are assumed to be “going concerns” and able to address their weaknesses. But it does come at the expense of timeliness.

There were several occasions where I as management had to “push the process” to get a more timely outcome. One of my mentors, Bob O’Sullivan was perhaps the best at this. The bureaucracy is real.

Later in the report, in Key Takeaway #4, there is this little tidbit:

staff informed SVBFG about a forthcoming MOU around information technology in 2021, but staff subsequently dropped the matter because they felt it would not be pursued by policymakers at that time

There was at least one fairly egregious issue that I remember examiners identified that was ultimately quashed by “policymakers.”

Key Takeaway 4: The Board’s tailoring approach in response to EGRRCPA and a shift in the stance of supervisory policy impeded effective supervision by reducing standards, increasing complexity, and promoting a less assertive supervisory approach.

This seems to me as a bit of a diversion.

The optimal number of bank failures is not zero, and if SVB was not systemic its failure would just be an interesting statistic.

The BIG ISSUE is why was the systemic risk missed.

This section comments quite a bit on the Economic Growth, Regulatory Relief, and Consumer Protection Act (EGRRCPA) as at least the partial cause for a change in culture in Bank Supervision.

What EGRRCPA did was cause the Fed to attempt to tailor its supervisory approach to the overall risk of the institution to the financial system (referred to in the report as ‘tailoring’). The larger, more complex, and more systemically important the institution, the more aggressive the supervisory approach.

There is nothing inherently wrong with this approach; in fact it makes eminent good sense.

In the interviews for this report, staff repeatedly mentioned changes in expectations and practices, including pressure to reduce burden on firms, meet a higher burden of proof for a supervisory conclusion, and demonstrate due process when considering supervisory actions

There is a pejorative implication from this comment, but accept for the reference to ‘a higher burden of proof’ I think that this is exactly what we want. Scarce resources should be devoted to more material risks, and the burden of supervision should be minimized where possible.

Over the same period, the intensity of supervisory coverage of SVBFG declined while SVBFG was in the RBO portfolio. For example, scheduled supervision hours for SVBFG fell over 40 percent from 2017 to 2020 (impacted, in part, by the pandemic), even as SVBFG grew rapidly. Supervisory attention increased dramatically in 2022 when SVBFG entered the LFBO portfolio. Budgetary resources may have mattered also. During this period, the overall number of supervisory resources

Again, exactly what we would want. In a world of finite resources, time devoted to an RBO with assets under $100 billion is time not spent on more important priorities. And as SVB grew to a size of importance “supervisory attention increased dramatically”

This little tidbit was snuck in at the end of this section:

Staff at the Board and the Reserve Banks produce a wide range of analytical work that examines the condition of the U.S. banking system with a specific focus on emerging risks that is designed to provide context for policymakers and staff.

Overall, the analytical and surveillance work seemed largely fit for purpose in terms of traditional assessments of the condition of the banking industry and emerging risks for individual banks.

Here I will disagree. Extremely rapid growth is a well-known risk factor in banking. SVB was an outlier and should have been flagged. One only needs to look at the FDIC’s History of the Eighties—Lessons for the Future

Risk Managing A US Debt Default

How does one risk-manage a potential US technical default on its debt?

Shorten maturities of UST to the window before possible default.

Swap into similar (not identical) securities not subject to the technical default (agencies)

Funny how Prime money-market funds may have lower short-term risk of a break-the-buck scenario than the Govt-only MMMF.

Bank of Japan Financial Stability Report

The Bank of Japan also produces a Financial System Report (April 2023)

This issue of the Report assesses potential vulnerabilities in Japan's financial system and the effects of changes in banks' balance sheets during phases of rising foreign interest rates by analyzing them from the following two perspectives.

First, global tightening of financial conditions has exerted stress on Japan's financial system.

Second, as pointed out in the previous issue of the Report, private debt has increased in Japan against the background of smooth functioning of financial intermediation

An interesting dimension of the Japanese banking system is the prevalence of retail deposits to fund their banks. These tend to be quite sticky as electronic payments is much more widely used in Japan than in the US. Switching costs are high.

And with the Japanese having implemented yield-curve control, it is less likely that they will see the rapid increase in rates that we have experienced in the US. 10 year JGB rates remain below 1%.

This is an excellent report; much more thorough than the US FSOC reports. Considerable detail on banks, insurers, the real estate sector, other non-bank financial institutions, as well as vulnerability analysis of banks to credit conditions and an inverted yield curve scenario (which I will note the US did not run before commencing its recent round of FF rate increases)

Revised FSOC Framework For Analyzing Systemic Risk

The US Treasury has issued for comment a revision to Analytic Framework for Financial Stability Risk Identification, Assessment, and Response

The new guidance drops 2019 requirements that FSOC assess the likelihood of a firm’s financial distress, apply an “activities-based approach” and conduct a cost benefit analysis prior to designation. These will be replaced with a quantitative and qualitative analysis process under which the council determines whether "material financial distress at the company or the company’s activities could pose a threat to U.S. financial stability".

CAT Insurance Rates Increasing

The price of tail risk is increasing. It’s almost as if the climate risk distribution is changing.

SCOR cites 40% average US catastrophe XL renewal rate increases at April

US renewals more orderly, but catastrophe rates up +30% to +100%: Gallagher Re

It keeps getting worse: Florida property insurance rates set to jump up to 60%

Deriving The ERP From Options Prices

I’ve long been a fan of using the information in option prices to inform decisions. Goes back to the interesting work Alan Malz did on deriving risk-neutral probability distributions from FX risk reversals. Here I came across a paper that purports to derive the equity risk premium from option prices. Seems a more systematic approach than the typical Damodaran analysis. It is also able to infer an instantaneous ERP during times of stress. This would seem useful for deriving the pricing kernal in a Litterman type model.

I propose and test a simple model of the equity premium implied by the prices of options on the stock market. The model assumes that markets for the stock index and its options are frictionless and complete to extract as much information as possible from their prices. Its forecasts of the equity premium are more accurate than those in prior work, especially when arbitrage costs are low. It offers new economic insights into why the premium varies, including why it increased for many years after the 2008 crisis. The model also provides a unified explanation of risk premiums for variance and higher-order moments of market returns.

Factor Information Decay

Factor Information Decay: A Global Study

This research addresses a simple but important unanswered question in the factor investing literature: how do the factor exposures of equity factor strategies decay over time?

AlphaArchitect has a nice summary of the importance of the paper:

At least two insights may be gained from this research that benefit portfolio management objectives. Practically speaking, a direct estimate of how a particular factor exposure evolves over a holding period provides information on optimal rebalance schedules. In addition, the ability to plot the estimates of the factor returns combined with knowledge of the optimal rebalancing periods per factor provides a picture of the expected returns for a single or multifactor investment strategy.

Value and low vol have the longest half-life; momentum the shortest.

Pot Gives Worms The Munchies

Drugs give biology’s favourite worms the munchies too

Research proving the obvious.

RFI stands for three components: Risk Management, Financial Strength, Impact of Non-Bank Subs

Full disclosure: I worked with Mike Silva quite closely while at the Fed. I do not believe I knew Ms, Segarra, though I did run the “risk specialists” at FRBNY.

Really insightful analysis Brian

Thank you

Excellent post mortem, as usual. Just one missing piece. The elephant in the room here is that the examiners failed to identify the bank’s direct & indirect exposures to the crypto markets despite the large implosions in the sector throughout 2022.

So when the regulatory climate towards crypto intermediation tightened in January/February, SVB was very exposed. It was a sitting duck when Silvergate went down. The rampant risk management & management failures catalogued in this report compounded the problem.

The Fed’s self-exam is silent on the crypto nexus both on the bank side and in the FRB examiner side, which is disappointing to say the least.