Perspective on Risk - May 1, 2023 (First Republic, Signature, etc.)

First Republic; FDIC Deposit Insurance Fund; Fed Should Get Out Of Small Bank Supervision; FDIC’s Supervision of Signature Bank; Compliance Controls At The Fed; Deleveraging The LBO Market; Real Risk

First Republic Is Gone

Some thoughts:

Glad this was handled in normal course under the existing law rather than seeing the twisted ‘systemic risk’ exception utilized.

Makes one think that SVB and Signature were a “surprise” to the FDIC (and Fed) and that is what led to the systemic risk exception.

Somewhat surprised to see JPM as the winner. There is a tension here between the FDIC’s obligation under the FDIC Act to obtain a least-cost resolution, and the Rieger-Neal Act which bars any bank merger that results in a bank controlling more than 10% of US insured deposits.

Because of Riegel-Neal, one might have wanted to see a regional like PNC acquire First Republic.

Evidently, the Riegel-Neal deposit cap doesn’t apply when the acquired bank is "in default or in danger of default." See 12 USC 1828(c)(13). Hat-tip to Todd Phillips on Twitter for pointing this out.

Uninsured depositors made whole

Interesting that debt, including senior debt, has been wiped out. This is a major difference from the treatment of firms in 2008, when it was perceived that imposing losses on senior debt would increase systemic risk.

In some ways, the rules of the new regime look pretty clear; all deposits will be protected, and all capital markets debt and equity will be at risk. The potential spillover risk to institutional MMF needs to be looked at, but this would be a clean regime and would allow for market signals from debt as well as equity.

Here are the announcements:

The FDIC and JPMorgan Chase Bank, National Association, are also entering into a loss-share transaction on single family, residential and commercial loans it purchased of the former First Republic Bank.

BP Note: From the JPM deck, the FDIC is providing 80% loss coverage on single-family residential. and commercial loans, for seven and five years respectively.

The resolution of First Republic Bank involved a highly competitive bidding process and resulted in a transaction consistent with the least-cost requirements of the Federal Deposit Insurance Act.

The FDIC estimates that the cost to the Deposit Insurance Fund will be about $13 billion. This is an estimate and the final cost will be determined when the FDIC terminates the receivership.

BP Note: This is about 10% of the current FDIC Deposit Insurance Fund.

BEFORE THE DEPARTMENT OF FINANCIAL PROTECTION AND INNOVATION OF THE STATE OF CALIFORNIA

FDIC will provide a new $50B five-year fixed-rate term financing. There is no disclosure of the rate on the loan, though JPM’s CFO said it was “at market” on the conference call. The loan is an artifact of the accounting, since more assets were acquired than deposits; no cash came out of the DIF.

The loss-sharing reduces the risk-weight on the loans.

This deal looks pretty good for JPM; looks immediately accretive.

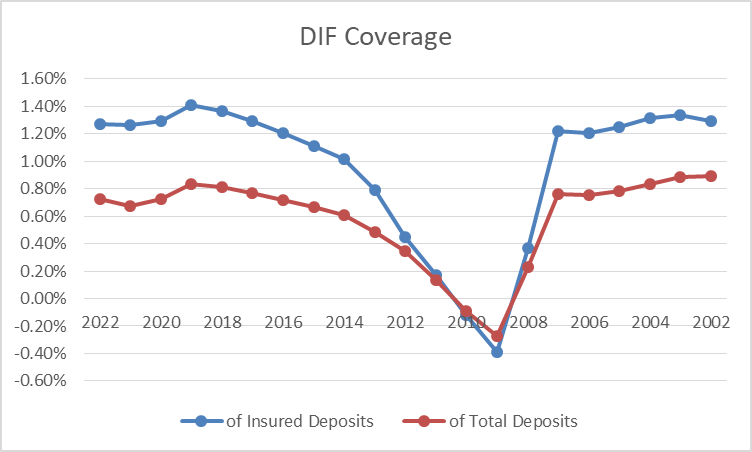

The FDIC Deposit Insurance Fund

As of December 2022, the FDIC deposit insurance fund stood at $128.2 billion. The DIF currently receives quarterly assessments of around $2 billion; in addition it earns interest on its balance so overall the DIF’s income is around $2.8 billion.

The assessment level is currently set at 2% of insured deposits.

As of year-end, there were apx. $17.7 trillion of deposits in the US banking system. Of this, apx. $10 trillion represented insured deposits.1

As a result, the DIF covered 1.27% of insured deposits. However, if all deposits are now defacto insured, the coverage ratio falls to 0.72%.

Since 2012, the share of uninsured deposits funding the banking system has grown from 22% to 43% of total deposits.

(Sorry that these charts read right-to-left, it’s how the FDIC had the data and I was too lazy to transpose)

In effect, with defacto full deposit insurance, banks with a greater share of insured deposits (think small local banks) have to date paid the deposit insurance cost for banks that relied more on uninsured deposits. This makes the blanket deposit guarantee seem even more egregious.

There may be some noise that the FDIC’s deposit insurance fund risks running out of money. It should be noted that this has happened before, most recently following the GFC. The three failures (SVB, Signature and First Republic) will cost the DIF $35.5 billion. This would take the fund down to ~$93 billion, which is 0.93% of insured deposits or 0.52% of total deposits.

Because the share of uninsured deposits has risen, the DIF coverage of total deposits (again, not something that is in the law) has fallen 10-20bp.

Fed Should Get Out Of Small Bank Supervision

Many of my former colleagues will hate me for saying this.

For years, we have had this tangled morass of agencies that regulate banks and bank holding companies. Firms can choose to have a state or federal charter. Federally chartered banks are automatically part of the Federal Reserve System. State-chartered banks can choose to be Fed members or not.

Each bank has a ‘primary federal supervisor.’ For federally-chartered banks, the Office of the Comptroller of the Currency (OCC) is the primary supervisor. For state-member banks that are part of the Federal Reserve System it is the Fed. For non-Fed-member state-chartered banks it is the FDIC.

In addition, state chartered banks are overseen and examined by the relevant state banking authority.

Further in addition, all bank holding companies are regulated by the Fed.

Now is where what I say will get controversial.

Arguably, the Fed and OCC have a comparative advantage supervising the largest, most complex, and typically federally-chartered banks. The FDIC arguably has a comparative advantage overseeing the vast number of smaller. state-chartered banks. There is nothing about being a member of the Federal Reserve System that gives the Fed an advantage supervising these banks.

Recently, we’ve seen a stream of bank failures; SVB being the largest, but also Signature Bank and now First Republic. The Fed and FSOC decided that the failure of SVB and Signature was a ‘systemic event’ that allowed them to take an extraordinary set of actions under the Dodd-Frank Act. Many of you know that I am not sure I agree with that determination, but that doesn’t matter for this proposal.

The problematic fact was that SVB and Signature Bank were not ex-ante determined to be a systemic risk, but rather this occurred at the very last moment. The Fed did not make this determination.

In my opinion, we should strengthen the incentives for the Fed to identify the systemic risk in advance. The Fed may have had a weaker incentive to determine whether SVB posed a systemic risk or not in advance because they were already the supervisor of the organization. Perhaps, in some way, being too close prevented them from taking the ex-ante steps required to make the systemic risk determination.

To that end, from an incentives point of view, I think the Fed should give up the supervision of non-systemic state-member banks to the FDIC. The Fed should have the right to make an a priori determination that a bank is systemic, which would them bring them under Fed supervision, and subject them to the enhanced prudential standards contained in the law, such as compliance with heightened capital and liquidity requirements.

The distance from existing day-to-day supervision would force the Fed to more actively identify the systemic risk, and to make the determination that the resolution regime written in the law would be inadequate to mitigate the risk.

In my opinion, this would be vastly superior to hard-wiring a lower threshold for the application of the enhanced requirements into the law, though this is much more likely the direction Congress and the Fed will go.

This, of course, will be fiercely opposed by the majority of the Fed’s District Banks. See this Perspective on Risk for some discussion of intra-Fed-Bank-Supervision politics.

FDIC’s Supervision of Signature Bank

Just as the Fed issued their review of the supervision of SVB, the FDIC has issued FDIC’S SUPERVISION OF SIGNATURE BANK. I have less insight into the FDIC’s operations and culture than I do with the Fed, so I will not speculate as much in this review. The report does read a bit more like the work of an auditor or Inspector General. It doesn’t address some core issues that are raised, like the inability to attract and retain a sufficient number of qualified staff.

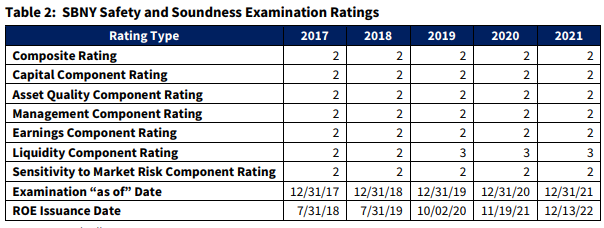

They admit they blew the rating

From 2017 through March 11, 2023, the NYRO assigned a Composite “2” CAMELS rating1 to SBNY, indicating that the overall condition of the bank was satisfactory. In 2019, the NYRO downgraded SBNY’s Liquidity component rating to “3” reflecting a need for improvement. However, the NYRO rated SBNY’s board and management performance as satisfactory until March 11, 2023.

Given the recurring liquidity control weaknesses, SBNY’s unrestrained growth, and management’s slow response to address findings, it would have been prudent to downgrade the Management component rating to “3,” (i.e., needs improvement) as early as the second half of 2021. Doing so would have been consistent with RMS’ forward-looking supervision concept, likely lowered SBNY’s Composite rating, and supported consideration of an enforcement action.

The failure to downgrade the management component seems particularly concerning given the following comments in the report:

SBNY management was sometimes slow to respond to FDIC’s supervisory concerns and did not prioritize appropriate risk management practices and internal controls. Management was described by FDIC supervisors as reactive, rather than proactive, in addressing bank risks and supervisory concerns.

SBNY executives were sometimes disengaged from the examination process and were generally dismissive of examination findings. When SBNY did take action to address examination findings, SBNY’s actions were more “check-the-box” or done to assuage the examiners, versus management understanding and appreciating the importance of underlying findings or control weaknesses.

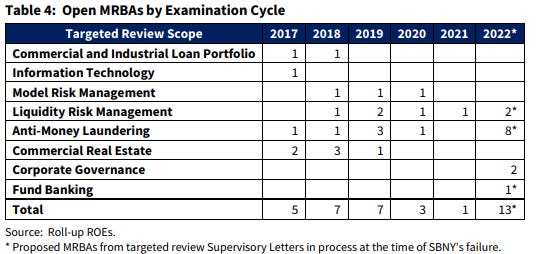

SBNY’s responsiveness to SRs was mixed. In many instances, the FDIC documented and discussed repeat findings or SRs and MRBAs across multiple examination cycles, particularly related to liquidity risk management, BSA/AML, and MRM, without management effectively addressing the underlying supervisory concern.

The report further discloses that the FDIC wrote up a more severe take even while leaving the ratings satisfactory.

In some instances, ROE narrative supporting the Management component rating appeared incongruent with the numerical (“2” Satisfactory) rating assigned. For example, from the 2019 roll-up ROE (which did downgrade the Liquidity rating)

A 2016 informal enforcement action appears to have been lifted prematurely

In 2016, the FDIC pursued an informal enforcement action against SBNY related to BSA/AML internal control weaknesses. In June 2018, the FDIC concluded that SBNY’s management had taken appropriate action to address those weaknesses and terminated that informal enforcement action.

However, the FDIC still had an open MRBA, their more significant type of findings, and had two additional open BSA/AML items in 2019.

Like the Fed, the FDIC was slow to issue enforcement actions

Due to weaknesses emerging from the 2022 targeted reviews, the FDIC was considering pursuing two new enforcement actions — a formal consent order related to AML/CFT and OFAC weaknesses and apparent violations and an enforcement action (the form of which had yet to be determined) related to longstanding funds management deficiencies as well as other risk management weaknesses.

Like the Fed at SVB, communication was not timely

The FDIC’s communication of examination results to SBNY’s board and management was often not timely. Targeted review Supervisory Letters and annual roll-up ROEs frequently exceeded elapsed-day benchmarks and in some cases were significantly delayed.

We observed instances where it took an inordinate amount of time to complete targeted reviews and deliver review results to the bank. … Of the 36 targeted reviews for which Supervisory Letters were issued, 24 took 100 or more days to complete and discuss with bank management, 12 took 100 or more days to issue the Supervisory Letter after discussing the targeted review with bank management, and 17 took 250 or more days from the start of the review until the targeted review Supervisory Letter was issued, with one targeted review taking over 400 days to issue the Supervisory Letter.

We experienced this issue while I was at the Fed. Delays resulted from numerous sources, including extensive wordsmithing to get the message correct, the lack of dedicated examiner time devoted to writing the letter, and the author of the letter often being on a subsequent assignment. It took consistent management attention to improve timeliness.

They understaffed one of their larger banks

The FDIC experienced resource challenges with examination staff that affected the timeliness and quality of SBNY examinations. From 2017 to 2023, the FDIC was not able to adequately staff an examination team dedicated to SBNY (Dedicated Team). Certain targeted reviews were not completed timely or at all because of resource shortages. These vacancies and the adequacy of the skillsets of the Dedicated Team contributed to timeliness and work quality issues and slowed earlier identification and reporting of SBNY weaknesses.

Calling of the “adequacy of the skillsets of the Dedicated Team” seems rather harsh, even if mildly worded. Overall, this comment needs to put more onus on management’s failure to insure proper staffing. Staffing inadequacies then led to additional management oversight, rewriting of reports (which then affects timeliness) and “questions about the quality and sufficiency of work.”

In addition to challenges in filling authorized positions, multiple NYRO and field territory officials commented to us about the adequacy of the skillsets of the Dedicated Team over time prior to the addition of new team members in 2022. These concerns resulted in the need for additional supervisory review, analysis of supporting working papers, substantial re-write of reports, and questions about the quality and sufficiency of work from NYRO officials that would normally not be involved in such activities.

This, of course, could have resulted in a risk-adverse atmosphere and inflated ratings. If management did not believe that sufficient work was done to justify a rating, or did not believe the work was of adequate quality, there would be an inevitable inertia in the ratings.

They do throw NYRO management under the bus

NYRO management is responsible for ensuring that banks in the region are adequately supervised. While resource shortages were a significant factor in the supervision of SBNY, NYRO management is ultimately responsible for prioritizing and risk-focusing the use of scarce resources, ensuring examination activities are completed and communicated timely, ensuring that ratings assigned are forward-looking and reflect management weaknesses, and escalating supervisory actions when bank management is not responsive.

The FDIC’s approach to staffing may have made it difficult to find a qualified examiner-in-charge.

The EIC position is of critical importance. The NYRO had difficulty finding qualified staff to serve that role. During this period, LFI EICs were required to sign a five-year contract to serve as EIC for a large bank. The five-year contract for EIC-1 expired at the end of 2021. The NYRO advertised the EIC vacancy two separate times during late 2021 and early 2022 but identified no qualified applicants.

The FDIC faced similar “vetting” tensions as did the Fed

Each quarter, a regional Case Manager8 prepares a report for the LIDI program, which includes LIDI analyses and ratings for their assigned institutions. LIDI ratings are designed to reflect a large bank’s potential risk to the DIF and specifically incorporate assessments of risk of failure assuming stressed conditions (Vulnerability to Stress) and FDIC losses assuming failure (Loss Severity)

A Large Bank Supervision (LBS) analyst recommended downgrading SBNY’s LIDI rating to a “D” beginning in the second quarter of 2022, but the NYRO did not agree with this change. The NYRO downgraded SBNY’s third quarter 2022 LIDI rating to “D” stable.

Compliance Controls At The Fed

Remember how many members of the Fed Board were found to be trading inappropriately?

Well the Fed’s Office of the Inspector General took a look at the FOMC’s compliance process and issued The Board Can Further Enhance the Design and Effectiveness of the FOMC’s Investment and Trading Rules.

We found that while the list of individuals covered under the Investment and Trading Policy for FOMC Officials includes senior FOMC officials, it does not include all individuals with access to confidential Class I FOMC information. Hundreds of individuals throughout the Federal Reserve System who have access to Class I FOMC information are not subject to any of the additional controls implemented in the policy.

We found that

while the Board must review the Reserve Bank presidents’ financial

disclosure reports, it is not required to review the financial disclosure reports

of other Reserve Bank individuals covered by the Investment and Trading

Policy;

the System does not have standard operating procedures that outline roles and responsibilities for reviewers to promote consistent financial disclosure report review across Reserve Banks; and

the Board does not have a formal process or roles and responsibilities for determining and enforcing consequences for ethics violations for Reserve Bank covered individuals.

We found that while Board and Reserve Bank ethics officers review the financial disclosure reports of covered individuals, they use a trust-based approach and do not take steps to verify that complete and accurate information has been submitted.

Good to see them getting their act together; better late than never; but sort of a fig leaf for the bad behavior of several FOMC members.

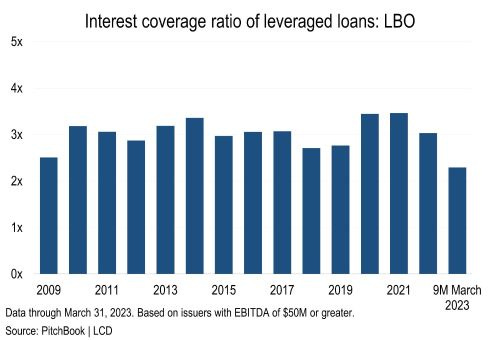

Deleveraging The Leveraged Loan Market

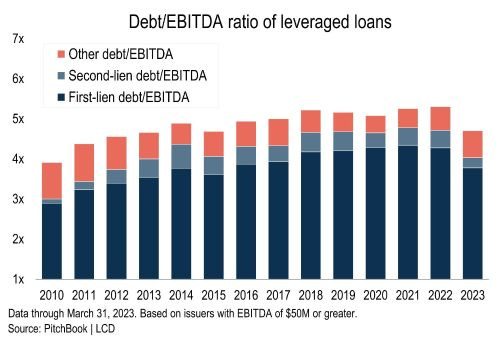

With LBOs scarce, leverage in syndicated US loan market sinks to 7-year low (Pitchbook)

Leverage is down, but so is interest coverage. Refinancings may need more equity.

Loans issued during the first quarter of 2023 had an average debt/EBITDA ratio of 4.7x, based on pro forma adjusted EBITDA, according to LCD, matching 2015 as the lowest reading in the last 10 years. Overall leverage ratios reached their 5.3x peak in 2021

the absence of LBOs has resulted in fewer B-minus borrowers in the loan market, contributing to the drop in overall leverage levels. Only 14% of this year’s issuance fell into the B-minus category, the lowest level in over 10 years.

interest coverage has declined significantly given the skyrocketing cost of debt. Over the last nine months, the EBITDA/interest ratio was at 2.3x for new-issue LBOs, the tightest level since 2007. It stood at 3x last year and 3.5x in 2021.

Based on LCD's sample of 141 loan issuers that report their results publicly, interest coverage on outstanding leveraged loans tumbled in the fourth quarter by roughly half a turn, to the lowest levels of the last seven quarters, to 5x on a weighted average basis, or 5.6x on a straight average basis. The sample is skewed toward higher-rated public names — double-Bs account for roughly half of the sample — so this cohort will have less aggressive leverage and coverage metrics, versus a much larger PE-backed universe, which is dominated by single-B rated borrowers.

For those who want more on the history of the FDIC and the DIF, George Selgin has written this excellent piece: The New Deal and Recovery, Part 27: Deposit Insurance

Of the many steps taken to combat the depression during the Roosevelt administration’s famous first hundred days, none was more significant than the passage of the June 16, 1933 Banking Act providing for the establishment of the Federal Deposit Insurance Corporation (FDIC).

No step was more significant, and none has been more misunderstood.

Now This Is Real Risk

The White Oak Shortage That Could Ruin the Bourbon Industry

In the coming years, the bourbon supply chain could be under threat, due to a shortage of the specific type of wood used in the barrels made for aging the liquor.

Peter - Just occurred to me that it may have made sense for the Fed to move to a Consent Order for SVB. Does the Fed define when a Consent Order should be used?