Perspective on Risk - March 28, 2025

The Trump/Bessent Approach; Counterpoint: Eichengreen on the Dollar; De-Anchored Expectations; What’s More Sensitive Than War Plans?

My framework on the three big factors driving future economic and financial market developments has been to focus on trends in globalization/deglobalization, demographics and technology.

As such, I’ve spilled considerable electrons thinking about, and watching developments around, the role of the US dollar in the global financial system in concert with the rise of China. This goes back to our early discussion of Zoltan Poszar’s work.1

Of more short-term and practical concern I’ve discussed the Treasury basis trade and Treas. Sec. Bassent’s desire to provide the large banks with Supplemental Leverage Ratio (SLR) relief.

Let’s bring these two trains-of-thought together in a somewhat speculative discussion.2

The Trump/Bessent Approach

We lose hundreds of billions of dollars a year on trade. We have a trade deficit of $500 billion a year. Who makes these deals?

—Donald Trump

Trump views the trade deficit as a form of foreign predation that directly harms American workers. He views the US as ‘losing’ and believes it is due to other countries cheating, such as through currency manipulation, and believes the dollar is too strong.

“China’s been cheating for decades. They’ve been manipulating their currency. They steal our intellectual property. They dump their products.” — Trump, Fox interview, 2019

"I want a strong dollar, but I want a dollar that’s great for our country—not a dollar that’s so strong that it makes it prohibitive for us to do business with other nations." — Trump, 2020

Because of these beliefs, he has no trouble embracing a trade war. It’s either escalate or continue to lose.

“Trade wars are good, and easy to win.” — Trump tweet, March 2, 2018

But it is broader than tariffs - it is a move away from multilateral deals (WTO, TPP) and towards bilateral negotiations with countries with large bilateral deficits.

“I like bilateral deals better. They’re much more efficient.” — Trump, remarks in 2017

But the primary adversary is China.

“We lose hundreds of billions of dollars a year with China and many other countries. It's not going to happen anymore.” — Trump, 2018 press conference

“Somebody had to take China on. This is something that had to be done.” — Trump, 2019 G7 press conference

If the U.S. is successful in reducing its trade deficit, it means it’s importing less than before relative to its exports—but since the balance of payments must still balance, this will have deep implications for capital flows, the dollar, Treasury demand, and interest rates. The trade deficit and capital inflows are mirror images: less one means less of the other.

Foreigners earn fewer dollars via trade surpluses, which reduces their capacity or need to recycle dollars into U.S. assets,

A shrinking U.S. trade deficit, especially with major surplus countries like China or Germany, implies that central banks accumulate fewer dollar reserves.

Reduced capital inflows + less FX reserve accumulation = a weaker USD. Central banks might diversify reserves away from USD toward gold, euro, or other currencies, especially if the dollar weakens. In addition, these trends might also weaken the role of the USD as the ‘safe haven’ currency.

Foreign investors (especially central banks) are key marginal buyers of Treasuries. If they’re not earning trade surpluses, they have fewer surplus dollars to recycle into Treasuries.

This, all else equal, would lead to higher nominal Treasury rates, potentially higher real interest rates as the US must fund its own fiscal deficit, and a steeper yield curve (as foreign central banks and sovereign wealth funds are buyers of longer-dated Treasuries and the Fed anchors the short end).

And all of this doesn’t require getting into the conspiracy theories of China or others ‘dumping’ their holdings of Treasury reserves.

Policies To Address Potential Developments

Sweeping tariffs and a shift away from strong dollar policy can have some of the broadest ramifications of any policies in decades, fundamentally reshaping the global trade and financial systems. (Hudson Bay Capital)

So we’ve covered the background. Perhaps the guiding document for the strategy is Hudson Bay Capital’s A User’s Guide to Restructuring the Global Trading System that was authored by an economist with Hudson Capital, Treas. Sec. Bessent’s firm. This provides the intellectual foundation of Trump’s rhetoric, so let’s review this in detail

The root of the economic imbalances lies in persistent dollar overvaluation that prevents the balancing of international trade, and this overvaluation is driven by inelastic demand for reserve assets. As global GDP grows, it becomes increasingly burdensome for the United States to finance the provision of reserve assets and the defense umbrella, as the manufacturing and tradeable sectors bear the brunt of the costs.

A Triffin World

The core of the problem according to Bessent is that the US has shrunken as a share of global GDP with the growth of China.

Because America provides reserve assets to the world, there is demand for U.S. dollars (USD) and U.S. Treasury securities (USTs) that is not rooted in balancing trade or in optimizing risk-adjusted returns. These reserve functions serve to facilitate international trade and provide a vehicle for large pools of savings, often held for policy reasons (e.g. reserve or currency management or sovereign wealth funds) rather than return maximization. Much (but not all) of the reserve demand for USDs and USTs is inelastic with respect to economic or investment fundamentals.

Such phenomena reflect what can be described as a “Triffin world,” after Belgian economist Robert Triffin. In Triffin world, reserve assets are a form of global money supply, and demand for them is a function of global trade and savings, not the domestic trade balance or return characteristics of the reserve nation.

When the reserve country is large relative to the rest of the world, there are no significant externalities imposed on the reserve country from its reserve status. The distance from the Triffin equilibrium to the trade equilibrium is small. However, when the reserve country is smaller relative to the rest of the world—say, because global growth exceeds the reserve country’s growth for a long period of time—tensions build and the distance between the Triffin equilibrium and the trade equilibrium can be quite large. Demand for reserve assets leads to significant currency overvaluation with real economic consequences.

America runs large current account deficits not because it imports too much, but it imports too much because it must export USTs to provide reserve assets and facilitate global growth.

As the United States shrinks relative to global GDP, the current account or fiscal deficit it must run to fund global trade and savings pools grows larger as a share of the domestic economy. Therefore, as the rest of the world grows, the consequences for our own export sectors—an overvalued dollar incentivizing imports—become more difficult to bear, and the pain inflicted on that portion of the economy increases.

Have We Reached The Triffin Tipping Point?

Eventually (in theory), a Triffin “tipping point” is reached at which such deficits grow large enough to induce credit risk in the reserve asset. The reserve country may lose reserve status, ushering in a wave of global instability, and this is referred to as the Triffin “dilemma.”

Some will argue yes.3

Moody’s warns on deteriorating outlook for US public finances (FT)

[Moodys] said on Tuesday that America’s “fiscal strength is on course for a continued multiyear decline”, having already “deteriorated further” since it assigned a negative outlook to America’s top-notch triple A credit rating in November 2023.4

But Bessent argues ‘not yet.’

The United States … is still far from such a tipping point, in part because there are no meaningful alternatives to the dollar or the UST.

While we are likely far from the economic crises that comprise the tipping point of the Triffin dilemma, we must nonetheless reckon with the consequences of the Triffin world. Reserve nation status comes with three major consequences: somewhat cheaper borrowing, more expensive currency, and the ability pursue security goals via the financial system.

The Narrow Path: Maintaining USD Reserve Status While Addressing Externality Problems

There is a path … but it is narrow, and will require currency offset for tariffs and either gradualism or coordination with allies or the Federal Reserve on the dollar.

Despite the dollar’s role in weighing heavily on the U.S. manufacturing sector, President Trump has emphasized the value he places on its status as the global reserve currency, and threatened to punish countries that move away from the dollar. … International trade policy will attempt to recapture some of the benefit our reserve provision conveys to trading partners and connect this economic burden sharing with defense burden sharing. Although the Triffin effects have weighed on the manufacturing sector, there will be attempts to improve America’s position within the system without destroying the system.

Bessent argues that the inflationary effect of tariffs will be offset by currency depreciation.

… the critical question is to what extent currencies adjust to offset changes in international tax regimes.

If the currency markets adjust, tariffs can have quite modest inflationary impacts... the tariffed nation pays via reduced real wealth, and the U.S. raises revenue.

And he cites the 2018-19 tariffs as providing reassurance as to the magnitude of the offset:

The effective tariff rate on Chinese imports increased by 17.9 percentage points... [and] the Chinese renminbi depreciated... by 13.7%... so that the after-tariff USD import price rose by 4.1%.

The argument Bessent (and the Jeanne and John paper he cites) are correlation-based, rather than causal, arguments. I will say that Bessent is cautious in making his argument, disclosing his assumptions along the way. There is other published research that also supports his findings without proving causality.

Unilateral or Multilateral?

So how does he propose to depreciate the US dollar?

He discusses multilateral and unilateral approaches.

The multilateral approach is referred to as “The Mar-a-Lago Accord” - you may have heard reference to it. This would be a coordinated approach by countries to adjust currencies to an agreed upon exchange rate.

Just as the Plaza Accord helped realign misvalued currencies through coordinated action in the 1980s, a modern-day version—what one might call a 'Mar-a-Lago Accord'—could realign today’s misaligned currencies, especially vis-à-vis the dollar.

The paper, however, discounts this pretty quickly:

As things stand, there is little reason to expect that either Europe or China would agree to a coordinated move to strengthen their currencies.

It is in the multilateral approach where the paper references Poszar’s proposal5 to have foreign central banks swap their existing Treasury holdings for ultra=long duration Treasury bonds (more on this later).

For the unilateral approach, the paper suggests four mechanisms:

IEEPA Powers (International Emergency Economic Powers Act). This authorizes the president to restrict financial flows, possibly including capital inflows that drive up the dollar.

U.S. Reserve Accumulation. The paper floats the idea that the U.S. itself could build FX reserves, similar to how surplus countries accumulate dollars to suppress their currencies.

Selective Capital Controls

Administrative Measures

In one view, the tariffs and the coming threats of unilateral approaches to address the exchange rate are just a way to get agreement on the multilateral approach. The paper even directly suggests this:

Tariffs are a tool for negotiating leverage as much as for revenue and fairness. Tariffs will likely precede any shift to soft dollar policy that requires cooperation from trade partners for implementation, since the terms of any agreement will be more beneficial if the United States has more negotiating leverage.

There is another potential use of the leverage provided by tariffs: an alternative form of Mar-a-Lago Accord that sees the removal of tariffs in exchange for significant industrial investment in the United States by our trading partners, China chief among them.

I expect this tension to be resolved by policies that aim to preserve the status of the dollar, but improve burden sharing with our trading partners.

Sweeping tariffs and a shift away from strong dollar policy can have some of the broadest ramifications of any policies in decades, fundamentally reshaping the global trade and financial systems.

The paper does include one very useful caution:

… many of these policies are untried at scale, or haven’t been used in almost half a century.

How This Relates To The SLR, Treasury Basis Trade & Other Topics

Now let’s discuss what is being proposed to handle these changes. Here’s a list I’ve come up with.

Focus on preparation for Treasury Basis Trade problems/blowups

Supplemental Leverage Ratio relief

Creation of a Permanent Government Backstop Facility (a la Bank of England's Gilt Facility)

All of these are designed for a world where foreigners, and foreign central banks in particular, are accumulating less Treasuries.

The Treasury basis trade profits from the difference between Treasury cash securities and Treasury futures. This “basis” has already widened significantly.

Different dynamics drive the cash and futures. Foreign central bank holdings are composed of cash bonds. Futures prices, however, are driven more by speculative demand, hedging flows, and margin dynamics—not by foreign reserve management.

TIC data (Treasury International Capital) shows that foreign official holders, particularly in Asia, have been reducing their Treasury holdings since mid-2023. China and Japan, the two largest holders, have both trimmed their positions. Countries like Saudi Arabia, India, and others have also dipped into reserves.

Foreign central banks currently hold, and often sell, off-the-run Treasuries, which are less liquid and may already be used in basis trades.

Treasury dealers are less willing or able (than in the past) to warehouse this inventory due to post-2020 regulatory pressures (e.g., SLR, GSIB surcharges). As a result, off-the-run Treasuries cheapen further, widening the "cheapest-to-deliver" spread in futures contracts.

This business is quite profitable, but requires considerable leverage.

The Fed and the BIS are aware of the risks of a blowup here. After all, this is a somewhat analogous LTCM’s problems in 19986. A key here is that the leveraged investors margin position gets worse as the basis widens. The inability to hold what appear to be profitable positions forces an unwind.

All of this goes under the euphemism “Treasury market disfunction.”

Several prominent financial economists have written a Brookings paper Treasury market dysfunction and the role of the central bank. The authors argue that the Fed should be prepared to take over both the cash and futures leg of the basis trade if/when a hedge fund investor fails. They argue that the Fed has the ability to hold the (arguably) profitable, self-liquidating trades to maturity and does not face the same liquidity concerns.

This would be in contrast to the approach that was taken when LTCM failed. When LTCM failed, the NY Fed coordinated a private consortium of 14 banks to inject capital and manage/wind-down the books.

I think this is a proposal carefully worth considering: it is a proactive rather than reactive approach, and it is an institutionalized version of the backstop that LTCM needed—just applied in a way that aims to support the market, not rescue firms.

At first glance, one could ask “why should the Fed even care about the level of the Treasury basis? Won’t a wide basis attract capital to arbitrage away the issue?”

I think the answer to that question in the short-term is “no” in large part due to dealer balance sheet constraints (and hence Bessent’s desire to provide SLR relief).

Treasuries are the benchmark collateral for financial markets. Their pricing affects repo rates, interest rate derivatives, and credit spreads. If Treasury pricing is dislocated, policy signals get muddled. Even small basis dislocations can throw off hedging, duration targeting, and the plumbing that ensures policy rates propagate smoothly across markets.

The third bullet, the creation of a permanent government backstop facility (a la Bank of England's Gilt Facility) is an alternative to the Kashyap proposal. This would likely be a formal US government backstop, with the Federal Reserve executing as its agent. This approach has a few advantages vis-a-vis Kashyap: it is a fully institutionalized approach with formal USG backing, and it would likely come with a preset trigger and rules making its execution very transparent. It would need pricing and eligibility rules to mitigate moral hazard risk.

The advantage of the Kashyap proposal, if I understand it correctly, is that by addressing the futures leg it will narrow the basis, whereas a government backstop for the cash leg only would widen the basis, risking being the transmission mechanism for further failures!

Other Policy Considerations

This transformation of the financial system is another reason why it is important to reduce the current level of fiscal deficit. Addressing the externalities of the currency misalignment means we should be reducing the level of Federal borrowing as the level of foreign Treasury demand decreases.

Is Poszar’s Commodity-Driven Currency Correct In The Long-Term

Many of you will remember an extensive discussion of Zoltan Poszar’s work back in 201X. He thought that the dollars hegemony was threatened by the rise of China and that we were headed for more of a commodity backed currency regime.

I remember back in the 1970s and 1980s, before the rise of trade imbalance first with Japan and later with China, the discussion often centered around the concept of ‘petrodollar recycling.’ This is where oil-exporting nations (e.g., Saudi Arabia, UAE, Kuwait) sell oil priced in dollars, accumulate large surpluses of USD from these sales, and invest/recycled these dollars into U.S. assets. This still occurs, but because these countries have no ability to threaten us militarily, and because they’ve agreed to play by our rules, it is not deemed nearly the same level of threat as China.

But the world needs to change (sorry TC). We are transitioning off of oil to an energy regime based on critical minerals. In this new world, China currently has something of an advantage, but the source of these minerals is much more diffuse. With these changes being proposed to the global trade and exchange rate order, with a weaker dollar, are we increasing the risk of reserve currency fracturing? To a world of more balanced reserves based on GDP? To a world where goods are not primarily/solely priced in USD? To a world of critical-mineral-dollar recycling?

Trump’s desire to control Greenland and the critical minerals in Ukraine suggests he is more aware than he lets on. Drill-baby-drill and its lowered oil prices will not necessarily be welcomed by the oil-exporting nations either.

Counterpoint: Barry Eichengreen on the Dollar

“A perverse ‘America First’ tariff policy destructive of US trade would accelerate [the dollar’s decline]…” — Eichengreen

There is a cult of us who hang on most every word Barry writes about the dollar.

In Can the dollar remain king of currencies? (FT) Barry offers pointed and historically grounded counterweight to the Trump-Bessent-Hudson Bay narrative. Eichengreen is not fundamentally at odds with the diagnosis of the symptoms (e.g., dollar overvaluation, global imbalances, potential erosion of dollar dominance). Instead, he is deeply skeptical of the proposed cure.

In this article, he recognizes that the dollar’s global role imposes burdens, especially on the U.S. trade balance and industrial base. He rejects the idea that size alone (GDP, markets) ensures the dollar’s continued primacy, and he highlights vulnerabilities, including sanctions overuse, fiscal instability, and declining trade share. He acknowledges that if the U.S. acts capriciously—by weaponizing its currency, undermining institutions, or turning its back on allies—confidence in the dollar can and will fade.

That is where the agreement ends. He radically disagrees with the confrontational approach being taken. Where Trump-Bessent prefer disruption, leverage, and unilateral restructuring, Eichengreen wants restoration through trust, alliances, and institutional credibility.

Trump and his appointees question the very values and arrangements on which nearly a century of dollar dominance is based. For the first time in living memory, the survival of the institutions on which that dominance rests has been cast into doubt.

His principal arguments against the Trump-Bessent approach are:

Tariffs shrink U.S. trade role and undermine dollar use in global commerce

The Trump-Bessent approach breaks trust with allies and violates reserve-holder expectations,

The proposal weakens the geopolitical foundations of dollar centrality.

In addition, he argues that rhetoric undermining Fed independence threatens the dollars role as a store of value.

Bessent vs Barry (for giggles)

For giggles, I asked ChatGPT to draw out a scenario tree based on the two proposals.

Regulatory Consolidation

Regulatory Fragmentation (Journal of Finance)

Regulatory fragmentation occurs when multiple federal agencies oversee a single issue. Using the full text of the Federal Register, the government’s official daily publication, we provide the first systematic evidence on the extent and costs of regulatory fragmentation. Fragmentation increases the firm’s costs while lowering its productivity, profitability, and growth. Moreover, it deters entry into an industry and increases the propensity of small firms to exit. These effects arise from redundancy and, more prominently, from inconsistencies between government agencies. Our results uncover a new source of regulatory burden, and we show that agency costs among regulators contribute to this burden.

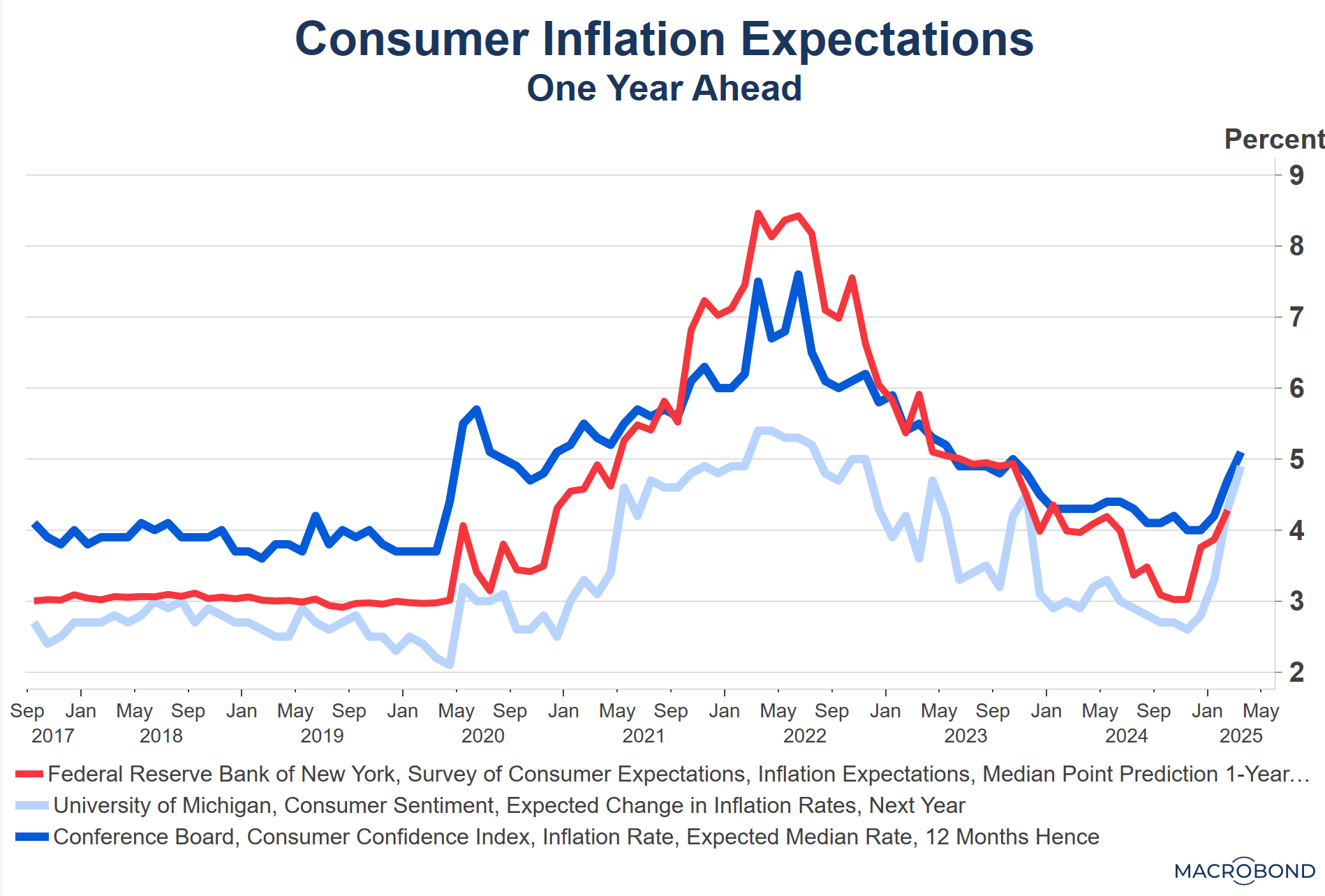

De-Anchored Expectations

What’s More Sensitive Than War Attack Plans?

Clearly, the US bank regulators Basel III negotiating positions.

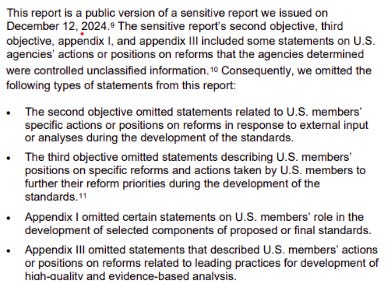

BANK CAPITAL REFORMS - U.S. Agencies’ Participation in the Development of the International Basel Committee Standards (GAO-25-107995)

From an otherwise generally glowing report:

This PoR was motivated by a discussion with several colleagues recently, and in particular prodded by a view from Asia.

A former Chief Credit Officer colleague of mine will say that the US hasn’t been triple-A for 2+ decades already.

S&P downgraded the US to AA+ in 2011.

Poszar, Zoltan. “Money and World Order.” Ex Uno Plures 2(8), 2024.

My understanding is that LTCM had somewhat of the reverse position on - short bonds and long futures.