Perspective on Risk - Jan. 9, 2025

A Possibly Wild Year; Bank Regulation; China Is Deflating/Deleveraging; More Credit Suisse; Maybe Things Have Gotten Too Complex

Back from vacation. Went to a wedding in Jersey (not NJ), and vacationed in Morocco. Great trip.

A Possibly Wild Year

We Need To Move From Preventing Climate Change To Mitigating The Effects

We’ve already hit the 1.5C limit and are blowing past it.

Global warming is worse than IPCC's worst case from 2014, and warming is accelerating as we reduce sulfur in the atmosphere.

We will be faced with climate-induced migration and political instability. Possibly massive displacement of populations due to climate disasters, leading to humanitarian crises and political instability in regions like South Asia, Africa, and coastal areas globally. Key infrastructure breakdowns, particularly in energy and food systems, due to extreme weather events.

Artificial General Intelligence Is About To Occur

“Independent evaluations of OpenAI’s o3 suggest that it passed benchmarks that were previously considered far out of reach for AI including achieving a score on ARC-AGI that was associated with actually achieving AGI (though the creators of the benchmark don’t think it o3 is AGI)” Ethan Mollick

“We are now confident we know how to build AGI as we have traditionally understood it. We believe that, in 2025, we may see the first AI agents “join the workforce” and materially change the output of companies.” Sam Altman

“… when can models reliably do professional … when can you go to a model and have it do reasonable tasks at … a level where a professional would look at it and say … this is up to Snuff - I trust it in finance in legal in biomedical in areas like insurance and productivity software uh in programming … I think we're maybe at the start of a two-year period where we're going to pass successively all of those thresholds." Dario Amode

China deleveraging/deflating/Japanification

Irving Fisher debt deflation in real time. The measures they have taken are no where near strong enough. Currency devaluation is really not an option.

See below discussion.

The World Order, As We’ve Known It, Is Changing

Ian Bremmer’s Eurasia Group has “The G-Zero Wins” as its top risk for 2025.1

The central problem facing the global order is that core international institutions—the United Nations Security Council, the International Monetary Fund, the World Bank, and so on—no longer reflect the underlying balance of global power.

The United States is powerful enough but unwilling to lead. Much more than in 2017, Trump’s return with a politically consolidated, solidly unilateralist administration will accelerate America’s decisive abdication of its longstanding role as world sheriff, champion of free trade, and defender of global values.

The US no longer can be, or wants to be, the free-worlds policeman. We are in a multi-polar world with China, and historic alliances and relationships are changing.

Resurgence of nationalism and populism. And the continued erosion of global institutions like the United Nations and WTO as countries prioritize nationalist agendas. China will want to shape institutions in its interest

Economic Turmoil Due to Debt and Fiscal Realignments

Major economies may face fiscal crises as debt levels become unsustainable. Potential sovereign debt defaults or restructuring could ripple through global markets. There will be pressures to allow inflation to run a little bit hotter to inflate away the debt.

FX markets may be at the fore once again. Trump would like a weaker USD, but Europe has weaker fundamentals. China’s RMB is undervalued, but could China devalue to spur its domestic economy (in response to tariffs). Japan is raising rates (albeit slowly) which could change carry trade dynamics.

Bank Regulation

Plenty of developments here.

Regulatory Independence And Consolidation

Barr steps down as VC of Supervision at the Fed to avoid a political showdown. As a result, Basel III Endgame revisions will either be DOA, or minimal in ways favoring the banks.

By not stepping gown from the Board, this will likely lead to Bowman taking that VC. If you’ve read my past posts, this isn’t such a bad thing.

The big takeaway is that the Fed will do whatever is needed to keep their independence on monetary policy, up to and including weakening or giving up its supervisory role.2

The OCC is led by an Acting Comptroller (who came in under a Democrat) and the FDIC is weakened with its internal issues.

Politico has a good article if you want more of the political inside-baseball: What Michael Barr’s decision means for Fed independence

If there ever was going to be an opportunity for regulatory consolidation, it is now.

Rob Blackwell, formerly of American Banker, has an only slightly cynical tweet stream:

With Barr's resignation as Fed VC for bank sup, this is officially the end of independent bank regulation. From here on out, the Fed VC job will turn over with new administrations. We've been coming to this point for a while.

First, the Supreme Court said the CFPB director was fireable at will. That had immediate implications for the FDIC board, on which the CFPB director sits. OCC's independence was real, but always tenuous, and it's had an acting for three plus years.

Once CFPB and OCC were essentially no longer independent, FDIC board was next, as they have two board seats. It meant that you could have FDIC chair overruled by own board. That's why Jelena McWilliams left in 2022.

So the Fed vice chair of supervision was the last position standing. In theory, it was independent, so a new administration could not immediately nominate their person for it until it was up after four years. But that too turned out to be tenuous.

Steve Kelly of Yale concurs:

Regardless of whether or not this was a kowtow or for other reasons, this will likely be precedent-setting for how political the role of the vice chair for supervision is. Barr stepping down likely means the role will continue to roll over with presidential administrations, much more like the other banking agencies' leadership roles.3

I still think the odds are against a wholesale merger (P=35%). The reason is because House members are very influenced by their local community bank constituents. Eliminating supervisory overlap is secondary to reducing regulatory burden, an consolidation into a national supervisor makes a more efficient promulgator of regulation.

Ideally, we’d merge the FDIC, OCC, Fed Supervision, NCUA Supervision. One could also merger FHFA, HUD and Farm Credit supervisors. And let’s not forget the SEC and the CFTC. Not sure what to do with the CFPB - probably keep them separate.

Biden Adding Roadblocks To Ending GSE Conservatorship

Bad form. Fixing definitively the mortgage financing business is unfinished work from the GFC. On their way out the door, the current administration is adding roadblocks to reprivatization: FHFA and U.S. Treasury Announce Amendments to the Preferred Stock Purchase Agreements (PSPAs)

FDIC Workplace Culture

I wrote4 about the FDIC’s cultural problems back in May when the Cleary Gottlieb report was issued.

The FDIC’s Inspector General has released their final report: Special Inquiry of the FDIC’s Workplace Culture with Respect to Harassment and Related Misconduct – Part 1 (FDIC Office of Inspector General) and it’s pretty damning.

Both reports found a patriarchal, insular, and hierarchical culture that led to harassment, discrimination, and related misconduct, creating a hostile work environment. Both reports, highlighted insufficient leadership accountability that exacerbated the misconduct and discouraging open communication.

The Cleary report provides detailed allegations against specific leaders, including the Chairman, highlighting how leadership behaviors contribute to cultural challenges. The OIG report, on the other hand, focuses more broadly on leadership's inconsistent application of policies without delving deeply into individual cases.

There is a need for systematic cultural change at the FDIC.

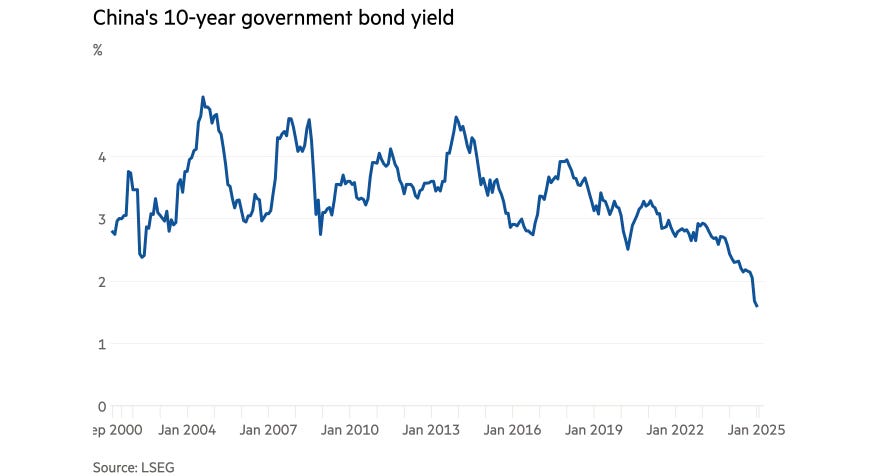

China Is Deflating/Deleveraging

Irving Fisher famously discussed a debt deflation trap in 1933. A debt deflation trap is self-reinforcing. He described the cycle approximately as:

Prices start falling while nominal debt levels remain fixed. This means the real value of debts increases.

As debtors struggle with their increased real debt burden, they start selling assets to make payments. This "fire sale" of assets drives asset prices down further, leading to more deflation.

However, the falling asset prices now reduce the net worth of businesses and individuals, leading to bankruptcies and business failures. This causes reduced business investment and production, rising unemployment and falling consumer spending

Banks face mounting loan defaults, leading them to reduce lending and contract the money supply, which causes even more deflation.

Japan faced this trap with its “lost decade” in the 1990s. The Global Financial Crisis was a debt deflation trap, with declining housing prices at the core. The major concern was to prevent the “fire sale” externality, and the US approached the crisis by firing all of the guns that it had.

Arguably, China’s deflationary trap began in 2014 when property prices first started declining. China responded at that time with looser monetary policy and numerous property-market specific policies.

But this appears to have only delayed the trap. Property prices began to decline again in 2021/22. This time, it was a broader decline, with weaker developer and local government balance sheets (which of course are closely tied), higher leverage, and in a slower growth environment with Chinese demographics turning unfavorable.

The Chinese appear to be taking a narrow and cautious approach to the problem, which is much larger now than before.

Ironically, a currency devaluation may not help the property sector as Chinese developers have been major issuers in the offshore USD debt market.

With deflation underway, even these low nominal rates represent a significant real rate.

Credit Suisse

As is typical following the failure of a large bank, the political authorities in Switzerland conducted an investigation

Press Release: Lessons from the Credit Suisse crisis – PInC identifies need for action (Swiss Parliamentary Investigation Committee)

Report: Conduct of federal authorities in the context of the Credit Suisse crisis

Responses

There are a few new revelations in the Report.

The End Began With a Tweet

Before we had the SVB run, we had a CS run.

In early October 2022, a tweet from an Australian journalist about the collapse of a global systemically important bank triggered speculation about the state of CS, resulting in huge capital outflows from CS. Markets reacted cautiously to the presentation of the new strategy at the end of the month and the situation remained volatile.

Following the tweet mentioned earlier, CS's share price fell by 11% on 3 October 2022. Shortly afterwards, customers withdrew over CHF 100 billion in deposits, marking the beginning of massive liquidity outflows.

CS had seen outflows of around CHF 130 billion in deposits since October 2022.

“Regulatory Filter”

In 2017, FINMA granted a “regulatory filter” to account for a ruling amending the treatment of parent company’s holdings (an accounting rule). The regulatory filter made it possible to neutralise the then impending change to the Swiss Code of Obligations with regard to the accounting requirements for holdings. The Report is unclear on the specifics of the accounting change. Nevertheless:

When the regulatory filter was designed in 2017, its effect was estimated by FINMA to be around CHF 8 billion. When it was first applied at the end of 2019, CS reported the filter’s effect to be CHF 15.3 billion, nearly twice as high as the original estimate. The amount of the regulatory filter remained approximately the same during the period 2019 to 2022. However, the reported equity of CS AG, calculated without the filter, fell significantly from the third quarter of 2021 due to poor business performance. Without applying the filter, the capital ratio would have fallen from 10% at the end of 2019 to 5% in the third quarter of 2022, well below the regulatory minimum.

The regulatory filter obscured the true situation of CS AG. As a result, CS was not forced to strengthen its equity situation at a time when it might have been easier to do so.

This process of granting “regulatory relief” is essentially deviating from GAAP (or IFRS). Banks will frequently argue that the accounting is “uneconomic” and that allowances need to be granted. The problem usually occurs after several years when no one remembers why the relief was granted in the first place. I remember this distinctly happening in the US with one foreign banking organization being granted “temporary” US holding company capital relief for an acquisition that somehow became evergreen.

Effectiveness of FINMA Supervision

The PInC specifically questioned "the effectiveness of FINMA's interventions."

Despite "ample use" of supervisory tools including annual assessment letters, on-site inspections and stress tests, FINMA's interventions were largely ineffective. FINMA repeatedly raised the same issues year after year but "CS made little progress." FINMA rarely issued formal rulings, instead relying on written expectations in assessment letters that often had to be repeated over several years

Probably to be expected. Overall, while CS was allowed to live longer than it probably should, it was resolved without disrupting the markets.

Maybe The Rules Have Gotten Too Complex

Quantum internal models for Solvency II and quantitative risk management

This paper extends previous research on using quantum computers for risk management to a substantial, real-world challenge: constructing a quantum internal model for a medium-sized insurance company. … we closely examine the practical bottlenecks in developing and maintaining quantum internal models. Our work seeks to determine whether a quadratic speedup, through quantum amplitude estimation can be realised for problems at an industrial scale. It also builds on previous work that explores the application of quantum computing to the problem of asset liability management in an actuarial context. Finally, we identify both the obstacles and the potential opportunities that emerge from applying quantum computing to the field of insurance risk management.

This will take model validation to a whole new level.

Top Risks 2025, Eurasia Group

PCB Central has an interesting post that touches on this: The partisan and institutional politics of Michael Barr