Perspectives on Risk - Apr. 28, 2022

Some Smart People Are Worrying About China; Roubini Chimes In On Our Themes; I Can’t Believe I Am Saying This; More Reading

I wanted to write a bit about China in the context of the broader discussion we have been having about the long-term incentive changes currently underway. Many of you know more about China that me, and I welcome your thoughts. If you need to catch up, here are the links:

Rethinking the Big Picture - Mar. 30, 2022

More Rethinking the Big Picture (pt. 1) - Apr. 12, 2022

More Rethinking the Big Picture (pt. 2) - Apr. 12, 2022

The principle observations are that:

There is an asymmetry between the financial system that remains spectacularly euro-dollar centered and the new multipolarity of power, trade and economic activity.

Covid supply chain disruptions, the ongoing frictions with China and the recent sanctions against Russia are causing policymakers and pundits to question the existing regime to address the asymmetry.

This is ultimately a geopolitical issue.

The world is already deglobalizing

Economic adjustments to the balance of consumption vs investment will need to occur both in the West and China. This will affect at the margin returns to labor and capital.

Some Smart People Are Worrying About China

Even before the current Covid lockdowns George Magnus was highlighting risks to China’s 5.5% growth target. He highlights the known causes, but importantly concludes that productivity growth has stalled and that China’s governance system is not good for the economy:

[China]’s not in great shape. There are a number of issues which weigh on its performance. One is the deadweight of excessive debt. Second is the glacial problem of a rapidly aging population and declining workforce, coupled with quite low levels of educational attainment. We have this image that everyone in China goes to Shanghai super schools and is top of the class in maths and science. That’s not really true. Only about 30% of Chinese workers have high school educational qualifications or better, and only about 15% have degrees. There are serious issues with the Chinese labor force to do with aging and education. And then productivity is a huge issue, not uniquely in China of course, but productivity growth has stalled. Add to that the harsh external environment plus China’s governance system, which is not good for the economy.

At its recent Twin Sessions, the government announced a 5.5% growth target for 2022. Is that realistic?

5.5% is the lowest in years, but it’s quite high relative to what China’s potential growth actually is. I think 5.5% can be achieved because for one, they can always manipulate it, and two, they will probably inject more stimulus into the economy in order to hit the target.

Adam Tooze (Chartbook 99: China under pressure) seeks to define the issues in the framework of Xi’s Risk Management approach:

Remember January 2019 when Xi was warning officials to beware “grey rhinos” - the threats that become so familiar that we actually end up ignoring them - as well as truly unexpected “black swans”? Risk management was the order of the day for cadres. Xi warned that they faced “changes not seen in a century”.

As summarized by CCP-thinker Chen Yixin in 2019, Xi articulated 10 guiding principles, six major effects, five tactics for preventing and diffusing risks, and five major campaigns to address the heightened global risk to China through a ‘risk management’ approach.

Tooze goes on to examine how China is handling the “classic grey rhinos1” (covid, real estate bubble, conflict with the US, economic slowdown) that Xi was concerned about, and finds China’s performance distinctly lacking:

Still, even with these issues, Tooze concludes that in the emerging bipolar world the major non-China Asian players (x-Japan) are currently stuck between the US and China, and will not choose a side unless forced:

[T]he fact remains that the US does not truly have a policy to offer in the Indo-Pacific strategy. It has published a blueprint. But is concerns are overwhelmingly domestic - fashioning a trade policy that is acceptable to America’s “middle class”. Whether that will suit any major partners in Asia is another matter altogether. The war in Ukraine is not going to persuade major Asian players that their future belongs in an anti-China camp masterminded by Washington. They do not want to have to choose.

Greg Ip has an interesting piece: How the West Can Win a Global Power Struggle (WSJ). What oil was to the global economy during the 20th century, he implicitly argues that semiconductors are to the current age. In the bipolar world, he cites the West’s advantages over the East.

Russia may be an energy superpower but Taiwan is a semiconductor superpower, and semiconductors are harder to replace than oil. Therein lies a critical insight about the emerging Cold War between Russia and China on one side and the West—the U.S. and its democratic allies—on the other. This Cold War will be much more of an economic contest than the first, and the balance of economic power favors the U.S. and its allies. And it’s not even close.

By itself, China accounted for 18% of global gross domestic product at current exchange rates last year, based on International Monetary Fund data. Adding Russia and their assorted allies brings the total to just 20%. The U.S., meanwhile, accounted for 24%, and adding its allies vaults the total to 59%.

While sanctions on Russia demonstrate the West’s control of the global financial system, long-run economic advantage will come from technology and knowledge. In pure science—such as space travel and atomic energy—Russia and China certainly hold their own. But in commercially useful technology, Western companies lead in almost every field, from commercial aviation and biotechnology to semiconductors and software.

As an aside, I might add that we should think through battery technology in the same way, Here I think China may be more of a competitor with the West.

Rita Rudnick, in Supply Chain Diversification in Asia: Quitting China Is Hard, has a nice discussion showing that the move out of China is less than meets the eye. She shows that it is the lowest part of the value chain, final assembly, that has moved from China to other Asian countries. Looking at Apple’s supply chain, she notes:

Delving further into these suppliers, many of the sites Apple removed from China were specializing in labor-intensive work such as packaging and metal production. At the same time, Apple added 14 new Chinese suppliers to its roster in 2021, many of which were higher value, knowledge-intensive manufacturers of intermediate goods like optical components, sensors, and connectors.

[T]he composition of Apple’s supply chain remains basically the same as before the trade war and pandemic. That is, R&D and most knowledge-intensive parts of the value chain are done in more advanced economies; end assembly and production of the simplest components are being gradually relocated from China to lower-cost countries such as Vietnam. But China is still home to the bulk of Apple’s supply chain.

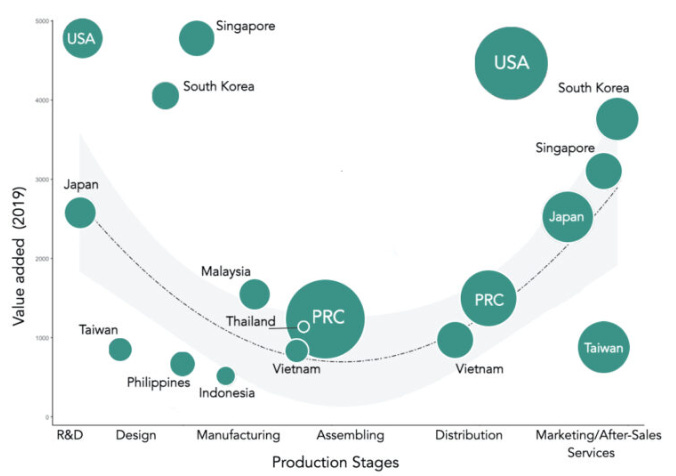

Ms. Rudnick goes on to helpfully articulate the “Smile Curve” developed by Acer’s Stan Shih to represent the value added in each segment of the value chain (see Figure 9).

Source: Adapted from Shih, S. (1992). Empowering technology—making your life easier. Acer’s Report, New Taipei.

Using trade and labor cost data, countries in this analysis can be plotted along the “Smile Curve” (see Figure 10). The results show that their positions along the curve have been largely stationary over the past two decades. Advanced economies like the United States, Japan, and South Korea occupy the higher ends, while China and Southeast Asian countries have continued to hover around the bottom.

If anything, countries like China and Vietnam are expanding in their existing positions along the curve rather than meaningfully shifting towards either of the higher ends. Despite growing larger in size, Southeast Asian countries still pale in comparison to China. Advanced economies continue to dominate the ends of the curve that are the most profitable parts of the global value chain.

The challenge for the West is to replace China at the low end of the value chain, while the challenge for China is to simultaneously move up both sides of the curve.

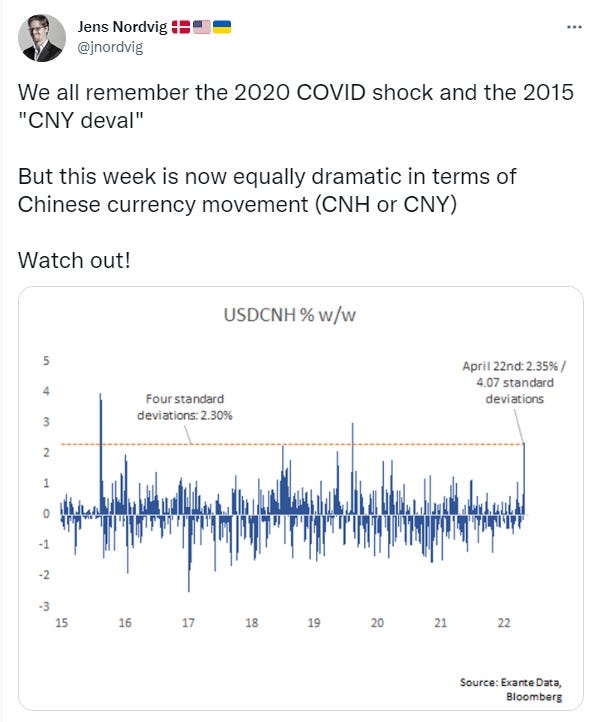

Meanwhile, it looks like the currency has turned:

Higher rates in the US will demand higher rates in China to staunch currency outflows.

Roubini Chimes In On Our Themes

Nouriel Roubini writes in The Gathering Stagflationary Storm (Project Syndicate):

[T]he global financial crisis, there has been a retreat from globalization and a return to various forms of protectionism. … Rising geopolitical tensions and the supply-chain trauma left by the pandemic are likely to lead to more reshoring of manufacturing from China and emerging markets to advanced economies – or at least near-shoring (or “friend-shoring”) to clusters of politically allied countries. Either way, production will be misallocated to higher-cost regions and countries.1

Moreover, demographic aging in advanced economies and some key emerging markets (such as China, Russia, and South Korea) will continue to reduce the supply of labor, causing wage inflation. …

The sustained political and economic backlash against immigration in advanced economies will likewise reduce labor supply and apply upward pressure on wages. …

Sino-American decoupling implies fragmentation of the global economy, balkanization of supply chains, and tighter restrictions on trade in technology, data, and information – key elements of future trade patterns. …

Finally, the weaponization of the US dollar – a central instrument in the enforcement of sanctions – is also stagflationary. Not only does it create severe friction in international trade in goods, services, commodities, and capital; it encourages US rivals to diversify their foreign-exchange reserves away from dollar-denominated assets.

Guess our thinking is now consensus. Don’t like it - need to rethink my priors!

I Can’t Believe I Am Saying This

But you should really read A Clash of Two Systems by Nassim Nicholas Taleb. A bunch of interesting and relevant observations. Here’s a tease:

A state that wants to base its legitimacy on cultural unity must be small; it is otherwise doomed to meet the hostility of others. A Francophone Swiss citizen, although culturally linked to his or her language, does not aspire to belong to France, and France does not try to invade French-speaking Switzerland under this pretext.

Some More Interesting Reading

Commodity traders seek to ride out liquidity squeeze (IFR)

Just How Many EVs Can Be Made? Far Fewer Than Expected

China’s Restructuring Firms Staff Up for Record Wave of Defaults (Bloomberg)

Can the EU wean itself off Russian gas? (FT)

The race to dominate the new battery economy (Axios)

Sam Bankman-Fried and Matt Levine on How to Make Money in Crypto (FT Odd Lots)

Equity Risk Premiums (ERP): Determinants, Estimation, and Implications – The 2022 Edition (Damodaran)

Xi defined ‘grey rhinos’ as the threats that become so familiar that we actually end up ignoring them