Perspective on Risk - Sept. 5, 2023

Daryll Duffie; Kohn’s On Jackson Hole; Hyun Song Shin On The Evolution Of Financial Sector Risk; Reluctance To Use Resolution Powers; Results In Windfalls; Sheila Is Disingenuous; Basis Trade; Nickel

Daryll Duffie at Jackson Hole

…the current intermediation capacity of the US Treasury market impairs its resilience.

As promised in the last Perspective, I will try and discuss perhaps the most prominent paper presented this year at Jackson Hole, Darryll Duffie’s Resilience redux in the US Treasury market. Duffie is a favorite among Fed policymakers, and Treasury market function is one of the Fed’s highest responsibilities.

Prof. Duffie succinctly describes the goal of the paper in the abstract:

Since 2007, the total size of primary dealer balance sheets per dollar of Treasuries outstanding has shrunk by a factor of nearly four. This trend continues because of large US fiscal deficits and regulatory capital constraints, which are necessary for financial stability but reduce the flexibility of dealer balance sheets. I review approaches for increasing the intermediation capacity of the market and for back stopping Treasury market liquidity with official-sector market-function purchase programs.

The conclusion right off the bat is pretty headline grabbing:

In this paper, I describe new empirical evidence, with supporting theory, that the current intermediation capacity of the US Treasury market impairs its resilience. The risks include losses of market efficiency, higher costs for financing US deficits, potential losses of financial stability, and reduced safe haven services to investors.

The paper frequently references a NY Fed staff report authored by Duffie and others: Dealer Capacity and U.S. Treasury Market Functionality

On typical trading days, [the aforementioned staff report] show that illiquidity in the US Treasur ymarket is well and simply explained by yield volatility.

Volatility alone explains about 80% of the variation in Treasury market illiquidity

Although yield volatility explains most of the variation in Treasury market illiquidity, [the aforementioned staff report] also show that dealer balance-sheet loading plays an important role, but only when balance sheets are heavily loaded – a highly nonlinear effect.

Figure4 shows that during March 2020 Treasury market illiquidity was at times over three standard deviations worse than predicted by volatility. Figure5 shows that a significant fraction of this excess illiquidity can be explained by much heavier-than-normal loading of dealer balance sheets.

Duffie then goes to to describe the theory that supports the findings, as other potential reforms to improve market efficiency and stability, including central clearing, and all-to-all trading. The paper also provides support for the Fed’s existing standing repo facility.

The Oddlots team subsequently interviewed Duffie for Darrell Duffie on Illiquidity and Volatility in the US Treasury Market. In this, in case you missed it before, he highlights the non-linearity:

It's a highly non-linear effect. When dealer balance sheets are normally loaded, they don't contribute to illiquidity, but when they're reaching their extremes where dealers are handling more Treasury trades and more agency MBS trades than they've handled in the past, then you see illiquidity go up well beyond the level predicted by volatility.

In this commentary, he does take a stand against the Supplementary Liquidity Ratio (SLR)

There is one capital regulation that I think is not necessary, and that's the one you mentioned, Tracy, the supplementary leverage ratio. That rule penalizes the provision of liquidity even for very safe assets.

Jeremy Stein, another Fed favorite, provided commentary of Duffie’s remarks

before we go from [Duffie’s analysis] to a set of policy recommendations, we need to ask a series of questions. To do so, let us stipulate that: (i) we have an interest in preserving market liquidity; and (ii) central-bank asset purchase can help, particularly when capacity constraints are binding or near-binding.

Does it follow that such purchases are the best or only way to go?

Or are there other approaches that might want to be the first line of defense?

And if we are going to in some cases use asset purchases for market function purposes, how do we communicate about them, both ex ante and ex post?

If Darrell’s diagnosis is correct and dealer capacity constraints are indeed at the root of the problem, a natural question to ask is: why take these as exogenously given? Can we relieve these constraints in some way? And while Darrell’s empirical measure is agnostic as to the root of the constraints—they could come in part from dealers’ internal risk management considerations, for example—one suspects that the risk-insensitive leverage ratio is at least part of what is going on.

Now I have historically been in favor of the SLR in a risk-based regime where bank internal estimates were being used. My simple thinking was that banks needed to be capitalized primarily on a risk-based basis, but that an SLR was a control for banks misestimating the risk on the highest quality securities and thereby over-leveraging (here think about the risk of underestimating the losses on super-senior CLO tranches). But Prof. Duffie is correct in that there is a tradeoff and it does reduce the liquidity in the Treasury market. This would be a reason to exclude Treasuries from the SLR calculation, but then you face the slippery slope of other highly-rated securities.

Prof. Stein goes on to say:

… defanging the leverage ratio absolutely does not have to come at the cost of weakening overall capital in the banking system. It is straightforward to make a compensating adjustment to risk-based capital standards to ensure that overall capital does not decline, or indeed actually goes up, in light of a relaxation of the leverage ratio.

Now this is all incestuous as Duffie and Stein were the principal Project Advisors for the G30 report, which was chaired by ex-NY Fed President, ex-Treasury Secretary Geithner with ex-Fed Pat Parkinson as Project Director. The actual language of the G30 report states:

The G30 Report therefore recommends that banking regulators make (unspecified) changes to the SLR to ensure that the SLR continues to function as a backstop, rather than a binding constraint. The G30 Report notes, however, that any reforms in this regard should not reduce the overall capital in the banking system – this may mean that risk-based capital requirements need to increase.

Matthew Klein provides a nice summary of the Duffie approach to the March 2020 events in The NY Fed Trading Desk's Time to Shine? (The Overshoot) and goes a step further suggesting:

there is an alternative approach, which both Duffie and Stein hinted at, even though neither seemed particularly keen on it: the central bank could disintermediate the dealers and play a more active role in directly making markets and setting bond prices across the yield curve. The BOJ already provides an example of how this could work in practice.

Don Kohn’s Take On Jackson Hole

Don is one of my heroes. A true risk manager as a central banker. He was interviewed by David Wessel for Brookings: Don Kohn’s Reflections On Jackson Hole 2023. Paraphrasing Wessel:

[With] the near-term picture looking somewhat more comforting, there [was] more focus on the long-term structural issues that the world economy faces.

Don cited the Charles Jones presentation on innovation and productivity that I highlighted in the last Perspective. As an economist, he focused on the total factor productivity slide (where I focused on the aspects of innovation).

On globalization, he states:

I thought a very interesting finding was that the more open economies are, the more diversified trade is, the more resilient economies are.

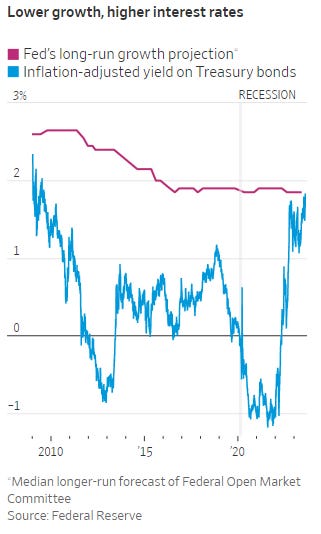

He expanded on the Eichengreen analysis of fiscal deficits noting:

A paper by Barry Eichengreen and Serkan Arslanalp was very discouraging with respect to the trajectory of the debt to GDP ratio in the U.S. and in many other countries as well. We’re running a primary deficit in the U.S. –that’s spending on everything besides debt service in excess of receipts – and the political system seems unwilling or unable to deal with this primary deficit, which is very large, especially considering we are at full employment with an inflation problem. And it’s going to get larger with the demographics of the population putting more pressure on Social Security, Medicare, and probably Medicaid as well. So that was discouraging.

The other point that Eichengreen and co-author made was that, in recovering from the huge debt load of World War II, there was quite a bit of what economists call financial repression … the view was that in current circumstances, with non-bank intermediaries growing in importance and many fewer restrictions on global capital flows – which was part of the financial repression of the1950s and 60s – that financial repression could not be counted on to solve the problem of r (the rate of interest) being high relative to g (growth rate of the economy).

Further:

The global savings glut … is no more.

Greg Ip wrote Why Fitch’s Downgrade Matters for the WSJ that has some relevence here. This sentence caught my attention:

One takeaway is that the global saving glut—the wall of money in search of safe assets that kept yields down a decade ago—is no more.

Sizing the change:

Independent economist Phil Suttle estimates private investors will be asked to absorb government debt worth 7.7% of developed economies’ GDP this year and 9.2% next, more than double the 4.3% of 2011. Private borrowers thus face competition from governments for capital, which in the long run hurts investment and growth.

And this image summarizes how r and g are related

Hyun Song Shin On The Evolution Of Financial Sector Risk

Hyun Song Shin Explains the New Financial Stability Risks (OddLots)

Along with the IMF, the BIS’s Hyun Song Shin usually has among the best broad perspective on risks to the global financial system. Here he chats with the OddLots folks.

It seems clear that everyone is aware of the significant shift to non-bank finance that is underway, and that will be further exacerbated by the pending increase in bank capital requirements. In the quest to “make the banks safer,” whatever that means, the risks will be pushed to the more opaque and unregulated sectors.

The thing … to start with is just to take her a step back and have an overview of the way that the structure of intermediation has changed. … What that does point to is the shifting nature of risks, the different propagation mechanisms and you know, the different set of players out there.

We're going from banks to non-bank players -- in the jargon they're called NBFI, it's non-bank financial intermediaries. But it's not just the intermediaries. I mean, it's also the way that infrastructure, you know, CCPs, exchanges, they've also become very important as well.

We have fewer of these bank-based intermediaries … they've shrunk in size and heft, if you like, within the system. Instead, what we have are many non-leveraged players, asset managers of various stripes, life insurance companies, pension funds, but I think a very, very important class of players are the other hedge funds as well.

There are [also] non-regulated market intermediaries there. And a very important part of the infrastructure here would be the new central counterparties, other exchanges where, rather than having intermediation go through a dealer balance sheet, you have clearing, you have the central counterparties that actually act as creditors and debtors to a wide range of participants.

The discussion turns to the recent financial sector ‘events’ - the 2020 Gilt episode and the SVB bailout, and Hyun puts these events into a broader picture, and discusses the systemic nature of interest rate risk::

We've had a very long period of low for long interest rates and of course central bank asset purchases that has really compressed the yield curve. And what that's meant is that borrowers have taken advantage of that and they've turned out, their borrowing …we see it in the corporate sector …we see it in the household sector as well.

But I think especially important would be the government bond market. There's been an increased duration of the bonds outstanding, not surprising really, because government debt managers would also be taking advantage of the low long-term rate.

If you look at the duration in aggregate of advanced economic government bonds, it was around seven years at the end of 2010, that's now nine plus years. So we've had a tremendous lengthening of duration.

The effect of this, he explains, is that we are seeing LESS credit problems from consumers and corporations, but MORE mark-to-market issues. He then asks, rhetorically:

How is it possible that a safe asset can still be at the center of a stress event?

He answers with a twist on the traditional firesale arguments:

When the price falls, you expect people to come in and pick up the cheap assets. But in these stress episodes, what you typically find is that a price decline actually generates more sales. And that actually of course leads to further price decline. And you can have this loop.

Leverage is one way that you can have that.

[Another way is when] the embedded option in the mortgage market [causes[ the duration increases actually because people stop refinancing.

Or it can be structural mismatches:

Something similar can happen even in very boring sectors like, you know, pension funds or life insurance. If you are trying to match duration and you have liabilities to your policy holders, which are let's say 30 years, but you have assets that are 10 years, liabilities are much longer duration than your assets. When rates rise, the duration comes in both on your assets and your liabilities, but because your liabilities a much longer duration than your assets, liability duration comes in much faster. So what ends up happening is that you find that you've got too much duration on the asset side. And so you have to sell.

Returning to market structure:

The reason why these financial stability channels of propagation can be so corrosive is because sometimes one part of the market just becomes too big. They grew without our knowing it, without our really noticing it. And then when something happens, this is when all these dynamics take hold.

He returns to referencing the Logan/Hausar paper that we have spoken about previously (for background I originally wrote about the Logan/Hauser paper in Perspective on Risk - Sept. 29, 2022 (The Pain Has Only Begun) :

To cut a long story short, the story there is we have to strike a balance. In the end, the central bank has to be a backstop. So if no one else is there to really pick up the pieces, the central bank has to be there to cushion that shock, because otherwise, the consequences of not doing so would be very, very large.

But it should not be a first resort to the extent possible. So whenever possible, it should be a market-determined outcome. The central bank shouldn't wade in at the drop of a hat. And if you like, influence market outcomes that way.

The other important point is that there's a very important issue here of incentives. If it becomes generally known that the central bank's threshold for pain is here and therefore they will enter, what that could do is to shift, if you like, the incentives in the portfolio decision of the private sector market participants. What you're doing by doing that, by having a kind of, you know, a rule to enter the market would be to lop off the left tail of the outcome distribution. [It] means that it becomes less risky to one layer of leverage.

How will the Fed know when a part of the market has become too big? In a world of transparency, does the Fed have the political will to add the ‘fog of war’ to its pain threshold (SVB would argue that they don’t).

Duration addendum:

Joseph Wang was reading through the Fed’s regional bank LT Debt proposal and noted:

The Reluctance To Use Resolution Powers

Patrick Honohan has authored The apparent reluctance to use resolution powers for big banks that discusses “an international standard approach to resolution policy for banks of systemic importance” from the perspective of a UK market participant. In it, he quotes Dave Ramsden, Bank of England’s Deputy Governor for Markets and Banking, as stating:

today a major UK bank could enter resolution safely: remaining open and continuing to provide vital banking services to the economy.

He then discusses how the Bank handled Silicon Valley Bank’s UK subsidiary, noting:

The powers helped expedite the bail-in of capital instrument and the sale of the rest of the bank to HSBC. But interestingly this was not the Bank’s first intention. Indeed, it announced on the Friday that resolution would not be needed and instead SVBUK would simply be put into insolvency—a solution which could have left 95 percent of the depositors waiting months for whatever they could recover from the insolvency.

He continues:

[Globally,] only a few banks have been resolved using the new tools, and most of these have been relatively simple cases, such as the Spanish bank Popular, … or the Croatian and Slovenian subsidiaries of Russia’s Sberbank. Some banks that should have been resolved using the new tools have been dealt with in a more old-fashioned manner.

He describes the Swiss position that the bail-in did involve elements of the resolution plan, but goes on to quote the Swiss authorities that

In a context of global market stress it was doubtful that this option would have restored the necessary confidence.

He asks the important question:

What use, one wonders, is a resolution plan that is ready to implement but will not resolve matters?

Not Using Resolution Authority Resulted In Windfalls For The Acquirers

The cost ion the US is absolutely outrageous. The cost of resolving Credit Suisse may be warranted as it was a systemic risk.

The $44bn bank bailout bonanza (FT)

With the books closed on that combination, we now have the official figures from quarterly reports and securities filings on all four of the major bank M&A rescues since the early spring crisis:

In each of these instances, the buyers took over the targets for an effective purchase price far less than the target’s book equity value, also called net asset value (the fair value of their assets less the fair value of their liabilities).

Those four … bargain purchases prices/negative goodwill add up to $44bn in collective gain.

Exploiting the desperation of regulators meant mostly easy money for the buyers. The tough losses then have been imposed on previous shareholders of these moribund banks, their non-deposit creditors as well as the deposit insurance schemes that are funded broadly by the banking industry. These failed banks had viable assets as these acquirers have demonstrated. Why the returns from those assets must be only captured by opportunistic parties remains a public policy question.

Glad I Get To Disagree With Sheila Again

In The truth about proposed bank capital rules (FT), former FDIC Chair Sheila Bair writes so many, many things I feel are wrong. Let’s discuss just a few:

Banks can fund a loan with equity capital as easily as with leverage.

I mean, wow. Has she read any Modigliani/Miller? Does she understand anything [….]. And I guess she means to do away with deposit taking entirely - that’s debt intermediation and leverage after all.

She claims that

banks … internal models … failed spectacularly during the financial crisis [because] large banks had every incentive to adopt models that understated their risks, as this would allow them to lower their capital requirements to boost equity returns.

Does she really believe this? Does she believe banks solely had models to game regulatory capital? Even though these models were in use before Basel and the US regulators considered using them for regulatory capital?

I assume she was aware that the Advanced Internal Ratings-Based (A-IRB) only became effective on April 1, 2008, which if I recall correctly was AFTER Bear Stearns had failed. Not quite sure how many quarterly earnings meeting the banks were able to exhibit those boosted equity returns.

She also states

Regulators have estimated that most banks already have enough excess capital to comply with the rules

But as we have discussed many times, there are two parts to thinking about regulatory capital; the minimum requirement, and the buffer above the minimum to avoid breaching the minimum requirement. Raising the requirement without changing the overall level of capital diminishes the buffer and increases the probability the minimum requirement is breached.

Incredibly disingenuous.

Is The Basis Trade Back?

Interesting paper by the DC Fed. Recent Developments in Hedge Funds’ Treasury Futures and Repo Positions: is the Basis Trade “Back"?

In short, the answer is "probably", at least to some degree.

This note provides evidence that hedge fund futures and repo positions are consistent with increased trading in the cash-futures basis. … Should these positions represent basis trades, sustained large exposures by hedge funds present a financial stability vulnerability.

Glad to see the Fed has some folks doing the analysis, but I certainly hope they have some FRBNY Markets staff actually talking to the HFs,

More Nickel Shenanigans

I’m way more obsessed with the nickel fraud than I have any right to be:

Another Metals Trader Says It Has Been Hit by a Nickel Fraud (Bloomberg)

US trader Kataman says it found containers full of steel waste

The revelation that the problem of non-existent nickel is more widespread will be another blow to confidence in the scandal-prone metals trading industry.

In the new case, US trading house Kataman Metals LLC alleges it paid $3.3 million for nickel from New Alloys Trading Pte. only to discover when it opened the containers that there was no nickel inside.

The trade appears to be part of a broader set of transactions involving several companies linked to [Prateek] Gupta