Perspective on Risk - Sept. 21, 2022

The White Bear; Change in Expected Returns; When Do Things Break? Credit Markets; Commodity Traders & Liquidity; Operations Risk; Financial History; Podcasts; Other

This will be a bit more of a ‘normal’ post; no big thoughts on decoupling, technology, demographics, climate etc.

The White Bear

Unlike a Black Swan, which by definition is a surprise, perhaps the markets these days are best characterized as a white bear; rare, but we’ve all seen it coming, and its rapidly mauling financial markets.

Rare white black bear or ‘spirit bear’ caught on trail camera

Change in Expected Returns

Two public data series I like to follow show the degree of improvement in expected forward returns. Not sure if expected returns are yet back to ‘normal’ whatever that might be, but clearly a much better place to invest cash than a year ago. First, let’s look at the GMO 7-year real return forecast:

Next, let’s look at the Research Associates efficient frontier. You will see an increased expected return to the higher volatility portfolios. Interestingly, at the low end of the risk spectrum, the returns are expected to be the same; somewhat intuitive as these portfolios are dominated by bonds where the expected return is close to the purchase yield.

For those who like numbers for their Black Litterman models, here is Market perspectives: September 2022 fromVanguard.

When Do Things Break?

(When the levee breaks, got no place to go)

Restrictive monetary policy/rising rates breaks things; time and again. The question is not whether things will break, but when, and what will the response function be like (historically the world’s CBs have not been willing to tolerate the pain).

Fed Chair Powell has just made it clear that we will get to at least a 1% real Fed Funds rate.

Jurrien Timmer of Fidelity attempts to show estimates of the real fed funds rate against an estimate of the neutral rate, R-Star).

Let’s talk about each of those peaks;

1987 (the first peak) coincided with the peak in the commercial real estate market and, of course, Black Monday in the stock market.

1995-2001 coincided first with the Asian financial crisis, and culminated in the dotcom bubble.

2006/7 of course was the peak of the subprime mortgage boom and the start of the Global Financial Crisis.

The peaks hold whether you use equilibrium real fed funds or other measures such as 5y forward, 5y real yields.

We currently are close to historical lows in risk premia (as measured byt he ACM term risk premia). Here are three views (long-term and since 2000 and 2010) from the NY Fed website. Clearly as the Fed implements QT through the roll-off and/or sale of its mortgage portfolio, the pressure will be for premia to rise.

Another way to look at it is to think about alternative investments; I can get 4% on a 2y UST, or implicitly buy commercial real estate with a 4.5% cap rate; not much compensation for the risk. If 4% is the terminal rate target for the Fed, then a 4.5% cap rate looks low.

The problem (probably) won’t be at the banks; they are well capitalized and mostly intermediate the risk these days.

Credit Markets

I haven’t written much about credit markets this year; I don’t have the same sort of info I once had. Still, it’s been pretty ugly out there. There have been stalled syndications, bond prices down >20%, defaults just beginning to tick up, and new issue yields now closing in on 10%.

Global Bonds Tumble Into Their First Bear Market in a Generation (Bloomberg)

The Bloomberg Global Aggregate Total Return Index of government and investment-grade corporate bonds has fallen more than 20% from its 2021 peak on an unhedged basis, the biggest drawdown since its inception in 1990.

European bonds have been hit hardest this year … [t]he yield spread between sterling and dollar-denominated corporate bonds is the widest since 2014

One particular insurance company was bearish on CLOs a good 3-4 years ago; perhaps a bit early. CLOs are NOW holding a higher percentage of risky loans as we head towards a slowdown/recession. I have not heard about deteriorating rating agency standards (someone let me know if you’ve heard different), so individual deal structuring will become increasingly important.

How the Morrisons buyout turned into a nightmare for Goldman Sachs (FT)

“It’s the biggest fiasco since the Boots LBO,” said one loan fund manager, referring to the 2007 leveraged buyout of the British pharmacy chain that left banks holding billions of pounds of debt as credit markets turned.

The group of 16 underwriters have taken a more than £200mn gross loss on selling the debt this year, according to Financial Times calculations. Marking the remaining unsold debt to market leaves a further £400mn hole.

Worth noting that at the beginning of the GFC many bank CROs were as or more worried about the clogged balance sheets from failed syndications like Boots as they were about things like the failure of Bear Stearns High Grade fund; it’s not always clear at the moment what the big problem will be.

Credit Markets Brace for Big Post-Jackson Hole Test From Citrix Loan Sale (Bloomberg)

Bankers are poised to kick off the $15 billion leveraged buyout financing for Citrix Systems Inc. next week, testing investor demand for risky debt just days after the Federal Reserve pledged to keep raising interest rates.

The loan portion of the deal, an expected $4.05 billion offering, will get under way on Tuesday after being reconfigured several times to help banks offload debt that they committed to provide in January, when credit markets were in much better shape. Loans then were trading at around 99 cents on the dollar, and have since fallen to about 94.6 cents on average, according to the Morningstar LSTA US Leveraged Loan Price Index.

The size of the financing is so large that banks have decided to hold onto part of the Citrix debt rather than overload the market with too much supply.

The underwriters plan to hold onto $3.5 billion of a leveraged loan, though they may reduce that amount if there is enough demand for the $4.05 billion broadly syndicated portion, of which about $1 billion has already been placed with private credit firms, Bloomberg reported.

Citrix offers deep discount to wrap $4.55B bellwether leveraged loan backing LBO (PitchBook)

Citrix Systems on Sept. 20 priced [at] an original-issue discount of 91 cents on the dollar

This leveraged buyout loan for Elliott got done at a discount and tighter terms; all-in dollar yield was almost 10%

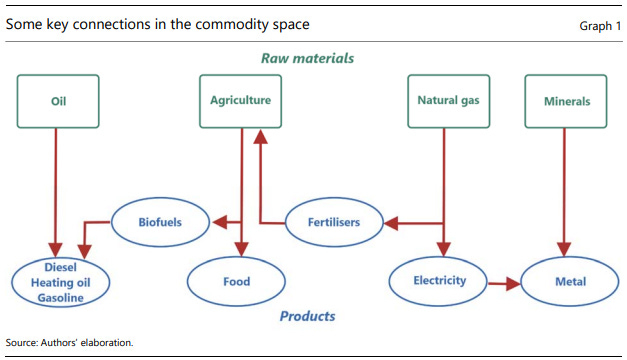

Commodity Traders & Liquidity

As we’ve discussed before, the current ‘systemic’ risks are not in the financial sector, but in the adjacent energy and commodity sectors.

The BIS has published a timely analysis, Commodity markets: shocks and spillovers1.

We argue that a substitution of Russian oil exports would be difficult, implying that restrictions on these exports may result in large and persistent price increases for oil-related products. Surging oil prices may be partly moderated by an increased use of biofuels, but this in turn could push up the prices of the staple crops that are biofuel feedstocks. In addition, persistently high prices for natural gas, key for electricity generation, could extend the recent electricity price hikes for final users – a strong headwind for all economic activity, especially industrial production.

Something I learned: the reliance of Europe on Russian gas is relatively recent, and is linked to the winddown of a gas field in the Netherlands.

For decades, a third or more of that supply used to come from domestic sources, underpinned by the massive Groningen gas field in the Netherlands. As late as 2013 its output, at 53 billion of cubic meters per year (bcm/year), represented 40% of the total EU natural gas production.

A footnote explains why:

From early on, gas extraction from the field led to minor earthquakes, which became more frequent and intense from the mid-2000s. In 2014 the production of the field was capped for the first time, and a programme of gradual cuts that stretched out to 2030 was introduced. In October 2019, the government decided to accelerate the shutdown of Groningen to September 2022.

Their analysis

has also pointed to two salient spillover mechanisms, from oil via biofuels to crops, and from natural gas via electricity to manufacturing. Some of these effects may still have not unfolded in full, due to structural delays in production chains, or may pick up steam if there are reversals in the recently subdued demand in key sectors (eg Chinese construction).

In addition, there is a nice exposition on the financial implications of volatile commodity markets.

A worthwhile read.

You may remember the shenanigans that occurred in the nickel contracts at the LME. The LME rewrote its rules to allow Xiang Guangda, nicknamed Mr. Big Shot, of Tsingshan Holdings to gradually liquidate its positions rather than fail at a margin call.

Looks like copper may be next. Copper (which is often anthropomorphized as Dr. Copper) is extremely sensitive to economic activity. Yasou Hamanaka of Sumitomo, nicknamed Mr. Five Percent, caused a lot of pain in 1996 when his manipulation of the copper market unfolded. This was back when Japan was the world-beating competitor.

Now its China, and Bloomberg has an article, Tycoon Running a Quarter of China’s Copper Trade Is on the Ropes, on He Jinbi of Maike Metals International Ltd. Maike is the largest player in the copper market and according to Bloomberg is reponsible for one-quarter of China’s copper imports.

In recent weeks, Maike began experiencing difficulties paying for its copper purchases, and several international companies — including BHP Group and Chile’s Codelco — paused sales to Maike and diverted cargoes.

The future is uncertain. He met a group of Chinese banks in late August at a crunch meeting organized by the local Shaanxi government. Maike later said that the banks had agreed to support it, including by offering extensions on existing loans.

But its trading activity has largely ground to a halt as other traders grow increasingly nervous about dealing with the company. And, in the wake of Maike's troubles, some of the biggest banks in the sector are pulling back from financing metals in China more generally.

“For many years, traders like Maike have been quite important in the importation of copper into China — they’ve bought very consistently to keep the flow of financing going,” said Simon Collins, the former head of metals trading at Trafigura Group and the CEO of digital trading platform TradeCloud. “With the property market like it is, I think the music could be stopping.”

No word yet on He Jinbi’s nickname.

Operations Risk

Chaos Researchers Can Now Predict Perilous Points of No Return

Barclays Is Buying Back $7.7 Billion of Securities After Mistake (Bloomberg)

Barclays Plc is close to concluding a buyback of securities after the bank accidentally issued billions of dollars more structured and exchange-traded notes than it had registered with the Securities and Exchange Commission.

The British lender said in a filing Thursday that $7.7 billion of securities have been submitted for the so-called rescission offer through a tender process, out of a total of $9.5 billion eligible.

Citi entitled to return of erroneous Revlon loan repayment, appellate court says (Pitchbook)

An appellate court on Sept. 8 ruled that Citibank is entitled to repayment of $500 million it erroneously sent to lenders of Revlon in August 2020.

At the time, the bank intended to make an interest payment on the company's outstanding leveraged loan in the amount of $7.8 million, but due to an error wired about $900 million to lenders in repayment of all principal and interest owed under the company's 2016 term loan due 2023.

Financial History

Two seminal days in the market.

Investigating the 1987 Stock Market Crash (stories.finance)

It Was 30 Years Ago Today, George Soros Taught the Bank to Play (Bloomberg)

Podcasts

Money and Empire: A Conversation on Charles Kindleberger and the Dollar System (Youtube)

Other

Market Share - Understanding Competitive Advantage Through Market Power (Morgan Stanley)

Mauboussin pieces are always worth reading

UBS and Wealthfront mutually agree to terminate merger agreement (Business Wire)

As we discussed earlier this year, this deal didn’t make much sense.

How Accurate are [Actuarial] Capital Market Assumptions, and How Should We Use Them?

Note I added the word ‘actuarial’ to the above title, as that is the focus of the paper. These are NOT the assumptions published by either the sell-side Wall Street firms or, like Vanguard above, the buy-side firms.

The annual Horizon Actuarial Survey of Capital Market Assumptions has become the pre-eminent source of aggregated information on the industry’s CMAs. Past surveys are published online going back ten years (2012 through 2021, with the 2022 edition likely out shortly), giving us an opportunity to begin assessing the industry’s performance in estimating long-term future returns.

CMAs tend to describe a return environment that is more stable than what occurs in reality

Were Those Great Returns the Result of Skill — or Just Luck? (Institutional Investor)

In a new research paper to be released on Thursday, Essentia used the new benchmark to evaluate 76 anonymized active, long-only equity portfolio managers over a 36-month period ending on March 30, 2022.

The Behavioral Alpha Benchmark incorporates Essentia’s seven key decision types: stock picking, entry timing, sizing, scaling in, size adjusting, scaling out, and exit timing.

[T]he research and analytics firm also found that 58 percent of portfolio managers added value through their stock-picking decisions. But a majority of managers destroyed potential returns by making poor decisions when sizing a position. Only 38 percent of the 76 managers added value when determining how big a position should be. … Managers are also weak sellers (“you end up wasting alpha in the way you get out”)

The Courage of Misguided Convictions: The Trading Behavior of Individual Investors

Modern financial economics assumes that we behave with extreme rationality; but, we do not. Furthermore, our deviations from rationality are often systematic. Behavioral finance relaxes the traditional assumptions of financial economics by incorporating these observable, systematic, and very human departures from rationality into standard models of financial markets.

This paper highlights two common mistakes investors make; they tend to disproportionately hold onto their losing investments while selling their winners and they trade excessively.

We present evidence that the average individual investor pays an extremely large performance penalty for trading. Those investors who trade most actively earn, on average, the lowest returns.

And the stocks individual investors purchase do not outperform those they sell by enough to even cover the costs of trading. In fact, the stocks individual investors purchase, on average, subsequently underperform those they sell. This is the case even when trading is not apparently motivated by liquidity demands, tax-loss selling, portfolio rebalancing, or a move to lower-risk stocks.

Avalos & Huang, Commodity markets: shocks and spillovers, BIS