Perspective on Risk - Oct. 28, 2022

Things Are Breaking; P(recession); Credit; JGB/Yen Update; US Dollar Dominance; Large Bank Resolution; Discrimination; Fed, Get Your Act Together; Kocherlakota; Crypto; LDI; Phillies Suck

This post is perhaps the exact opposite of the r* torture post.

Things Are Breaking

Things That Have Broken:

Japanese Yen

British Gilt

JGBs

US/Europe CLO issuance

Let’s add: Eurozone repo

ICMA warns of eurozone repo “dysfunction” (FT Alphaville)

The International Capital Markets Association has today sent this open letter to the European Central Bank to express finance industry fears over “rising dysfunction” in the eurozone repo and money markets.

Basically, if we’ve got this right, the ECB’s QE programme created reserves to buy eurozone bonds, but banks are now swimming in reserves while the European financial system is struggling with a shortage of high-grade eurozone bonds to use as collateral.

Let’s add: #USDCNY

Offshore Yuan Rises Most on Record as China Banks Sell Dollars (Bloomberg)

The yuan gains due to suspected state bank intervention earlier further compounded the broad dollar softness since last night, said Stephen Chiu, chief Asia FX & Rates strategist at Bloomberg Intelligence. “It offers some near-term stabilization for the yuan after the rapid drop over the last few days.”

Of course, they waited until the end of the Party Congress

Recession Probabilities Are Rising

On Oct. 21 the Estrella/Mishkin metric predicted a 23% probability of recession. Today, however, the 3M/10Y curve has inverted (4.13% vs 3.96%) so the odds will rise further.

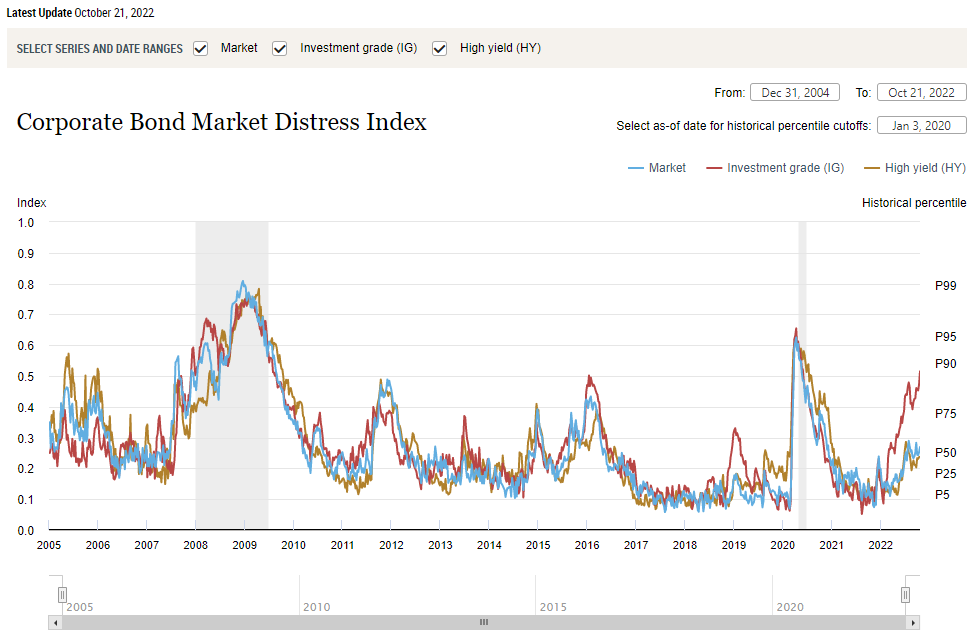

Corporate Bond Stress Rising, But Not Yet Near GFC/Covid Peaks

Corporate Bond Market Distress Index (NY Fed)

By the NY Fed’s gauge, IG bonds are at the 90th percentile but HY still holding up. Covid went noth of the 95th %tile, while the GFC went past the 99th

As expected, downgrades at the B- level exceeding upgrades.

Corporate defaults have yet to follow, but they will

Leveraged Loans Still Ugly

Leveraged loan financing for LBOs deteriorates as cost of debt rises (Pitchbook)

US companies raised just $10.6 billion of leveraged loans to fund buyouts over the past three months, the lowest such reading in almost seven years. The drop-off in activity is even more stark when compared to a year ago — LBO-related volume totaled $46.1 billion in 3Q21, the busiest quarter since the Global Financial Crisis.

[I]nvestor appetite for risk faded in the third quarter, forcing arrangers to offer LBO loans, which tend to be lower-rated, at uncharacteristically high discounts. The small sample of LBOs syndicated in the third quarter had an average price of 92.3 cents on the dollar and ranged from 90.5 to 94. In January, the average OID stood at 99.2, and the range varied from 98 to 99.8.

JGB/Yen Update

We’ve mentioned numerous times before that liquidity conditions in sovereign bond markets, including the UST, has been stressed.

Joseph Wang points out that the issue with the JGB/Yen is due to a policy decision to engage in yield curve control. Japan has intervened already to slow the Yen’s depreciation, but the effect of the intervention was very short-lived. Japanese life insurers would seem to be particularly at risk.

Fed Staff Paper on US Dollar Dominance

Geopolitics and the U.S. Dollar's Future as a Reserve Currency

I survey the role of geopolitics and sanctions risk in shaping the U.S. dollar's status as the primary currency used for international reserves. Without changes in the economic incentives for holding FX reserves in U.S. dollar assets, an increased threat of sanctions is unlikely to drastically reduce the dollar share of FX reserves. Currently, around three-quarters of foreign government holdings of safe U.S. assets are by countries with some military tie to the U.S. Even a reduced reliance on the U.S. dollar for trade invoicing and debt denomination by a large bloc of countries less geopolitically aligned with the U.S. would be unlikely to end U.S. dollar dominance.

Large Bank Resolution

The FDIC and Fed issued an Advanced Notice of Proposed Rulemaking (ANPR) seeking input of the orderly resolution of large (principally non-GSIB) banks. Here’s a link to the ANPR.

The essential question they are asking is whether these firms should have a loss-absorbing long term debt requirement, and if so whether the current rules that apply to the GSIBs should be modified for this cohort of organizations.

Discrimination

How Much Does Racial Bias Affect Mortgage Lending? Evidence from Human and Algorithmic Credit Decisions1

Using newly available HMDA data for 2018-2019, we find that standard underwriting factors can explain most of racial and ethnic disparities in denial rates. Further evidence suggests that the remaining 1-2 percentage point differences in denial rates (what we refer to as “excess denials”) are at least partially due to differences in racial and ethnic distributions of unobservable underwriting factors. Overall, racially-biased credit decisions appear less common than has been suggested by previous research. Our results imply significant progress in fair lending for mortgages over the last 30 years.

Fed, Get Your Act Together

I really don’t like having to write this about my former employer, but the hubris or cluelessness is a bit much. Bullard and Bostic should both step down.

A Fed President Spoke at an Invite-Only, Off-the-Record Bank Client Event2

Atlanta Fed President Discloses Violations of Financial Transaction Policies3

Kocherlakota Throws Shade at Bank of England

Markets Didn’t Oust Truss. The Bank of England Did. (Bloomberg)

The Bank of England, as the entity responsible for overseeing the financial system, bears at least part of the blame for this catastrophe. As a result of its regulatory failure, it was forced into an emergency intervention, buying gilts to put a floor on prices. But it refused to extend its support beyond Oct. 14 — even though its purchases of long-term government bonds were fully indemnified by the Treasury. It’s hard to see how that decision aligned with the central bank’s financial-stability mandate, and easy to see how it contributed to the government’s demise.

Crypto Update

David Gerard provides an update4 on the Celcius, Three Arrows Capital, Terra-Luna, and Voyager bankruptcy/litigation, if anyone still cares.

LDI Update

In a tweet stream, Dan Mikulskis back-of-the-envelope estimates that the market move required rebalancing flows totaling £270 billion.

JPM doubts the margin-call doom loop could happen to US insurers5, mostly because "in the UK there was actually a shortage of high-duration, high-grade, long-maturity fixed income that LDI strategies need, which forced many into using interest rate swaps as a synthetic, leveraged alternative."

This is a really cool use of AI

For instance, I uploaded a copy of the r** paper from the last post to explainpaper.com, and it readily answered questions I posed, such as the sources of nonlinearities in the model, the current level of r** relative to historical averages, and whether this indicated heightened or lessened financial stability risk.

First Boston is Back

Credit Suisse unveils new strategy and transformation plan (Credit Suisse)

Matt Levine has a great summary Credit Suisse Gives First Boston a Second Chance (Bloomberg). Also, Who is Michael Klein, new CEO of CS First Boston? (eFinancialCareers)

Root Against the Phillies

Just another reason to root against Philadelphia

Bhutta, Hizmo, Ringo, How Much Does Racial Bias Affect Mortgage Lending? Evidence from Human and Algorithmic Credit Decisions, Board of Governors of the Federal Reserve System

Smialek, A Fed President Spoke at an Invite-Only, Off-the-Record Bank Client Event, NY Times

Timiraos, Atlanta Fed President Discloses Violations of Financial Transaction Policies, WSJ

Gerard, Crypto collapse: Celsius reveals its creditor list, 3AC NFTs, Terra-Luna, Voyager, Attack of the 50’ Blockchain

Wigglesworth, Could the LDIbacle happen in the US?, FT