Perspective on Risk - Oct. 19, 2022

It's Liquidity, not Solvency; Central Banks Are Willing To Break Things; Things Are Breaking; Foreign Currency Reserves Are Falling; IMF Meeting Readout; LDI & Derivatives Clearing; & Custody; <more>

The Fed is looking to take out the excess liquidity it has pumped into the system going back to the GFC (or even earlier). And it has just begun.

We are worried about a loss of adequate liquidity in the market

That quote is from Janet Yellen on 10/12/2022.

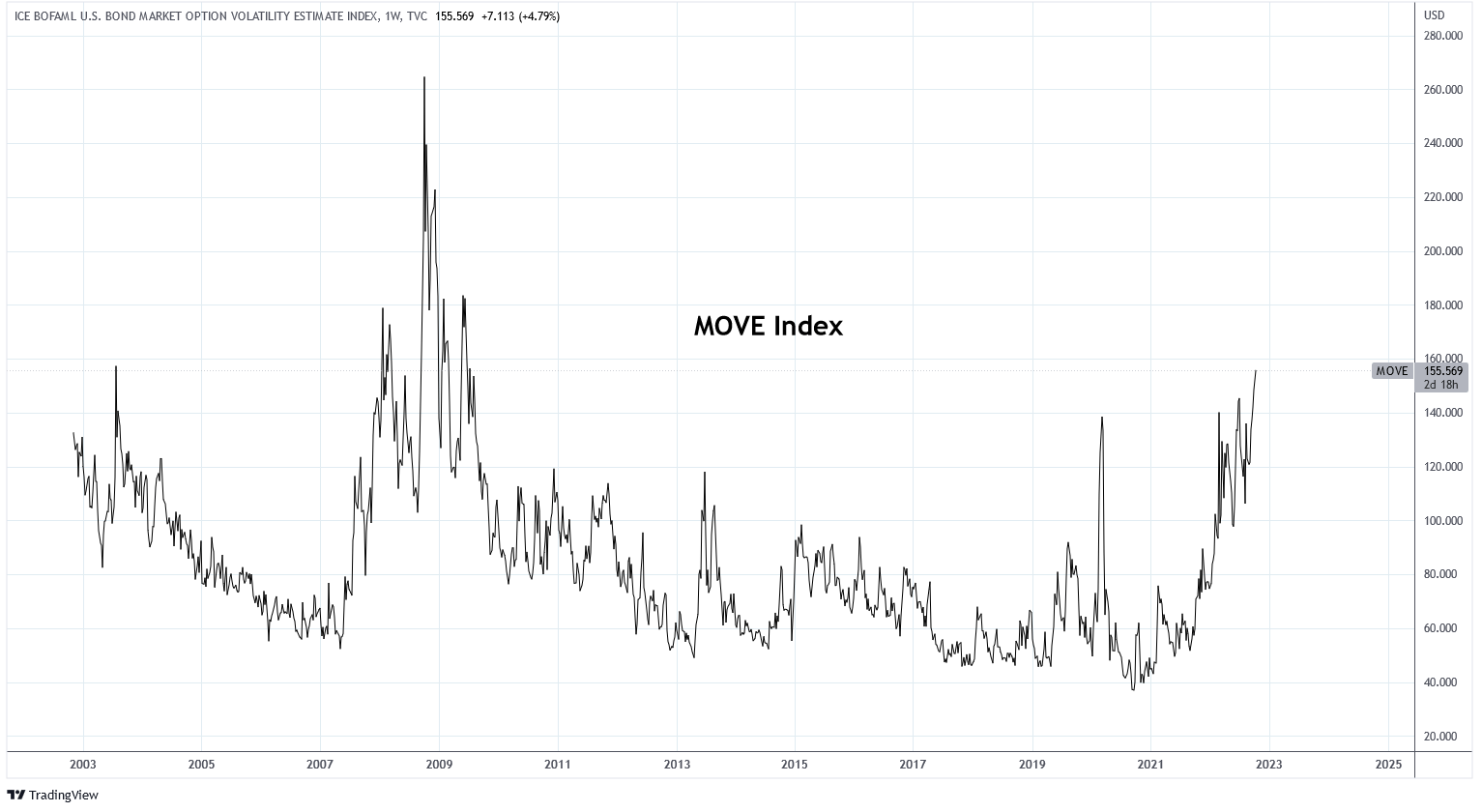

The MOVE index, which calculates the future volatility in U.S. Treasury yields implied by current prices of options on Treasuries of various maturities, is at levels not seen since the 2008/9 Global Financial Crisis (and above Covid highs).

Harley Bassman, the creator of the MOVE index, says when the MOVE is above 150, or 9.5bp per day, is unsustainable1.

Primary dealer delivery fails have spiked.

And the Treasury is asking the primary dealers whether they should buy back some off-the-run securities to improve liquidity23.

The Bank of America survey that asks about liquidity conditions is poor (but with room to go lower).

Remember when Jamie Dimon was voicing concerns about capital and other regulatory requirements constraining banks’ ability to support their customers? The US government is a pretty large customer, and the simplistic leverage ratio is a constraint on banks holding low risk UST and Agency securities. In fact, bank holdings of Treasury and Agency securities has actually declined.

Remember too our discussion of the Logan/Hausar paper on the central bank response function as liquidity is withdrawn; the central banks will support orderly markets, but will allow market prices to find their appropriate level. This is what the Bank of England has just done.

The Fed put has gone away, and consequently volatility has risen. That means the Fed will buy bonds or use a lending facility, but will not cut rates.

Higher volatility, all else equal, means one should be less levered so as to withstand mark-to-market shocks (regardless of the accounting my insurance industry friends).

Remember too Rudi Dornbusch’s maxim:

Central Banks Are Willing To Break Things (cont.)

Many took the Bank of England’s action to push down Gilt yields as a ‘central bank put.’ Andrew Bailey made it clear that they will provide temporary liquidity, but not a put.

“We’ve announced we will be out by the end of this week. My message to the [pension] funds is you’ve got three days left,” Bailey said.

Markets freaked. Homie don’t care.

Move fast, break things.

Things Are Breaking (cont.)

Things That Have Broken:

Japanese Yen

British Gilt

Let’s add: JGBs

Let’s add: US/Europe CLO issuance

And maybe we are close/at the point of adding UST (see above).

Foreign Currency Reserves Are Falling

World Currency Reserves Shrink by $1 Trillion in Record Drawdown (Bloomberg)

Reserves have declined by about $1 trillion, or 7.8%, this year to $12 trillion, the biggest drop since Bloomberg started to compile the data in 2003.

Part of the decline — more than half according to estimates from Steven Englander, Standard Chartered Plc’s global head of G-10 foreign-exchange research — was due to valuation changes. As the dollar jumped to two-decade highs against other reserve currencies, like the euro and yen, it reduced the dollar value of the holdings of these currencies. But the dwindling reserves also reflect the stress in the currency market that is forcing a growing number of central banks to dip into their war chests to fend off the depreciation.

IMF Meetings Readout

Robin Brooks of the IIF gave a nice readout4 on Twitter of his takeaways from the recent IMF meetings. Summarizing:

No consensus on monetary policy. Most policy makers want to keep hiking aggressively, most market participants want central banks to slow.

Debt-to-GDP ratios are back! Many G10 countries have gov't debt that's higher than the UK (GB). Market focus is now squarely on them.

Most think Ukraine will win and take back ALL its territory from Russia.

Russia's invasion of Ukraine is a total game changer for global capital flows. Front and center is China, where anecdotal evidence that new money is no longer being put to work by foreign investors lines up with our flows going flat. Saudi Arabia is also under scrutiny...

Lots of focus on deteriorating market liquidity. This is attributed to market makers at their risk limits due to volatile commodity prices.

German deindustrialization. Focus on Germany is intense. Worries of energy rationing are fading, given growing evidence that energy consumption is falling. Instead, there is growing focus on the medium-term, with manufacturing leaving Germany for locations with cheap energy...

Growing dismay over de facto Euro zone spread control. Wide-spread consternation that the volatility of Italy's spread was near all-time lows into the Sep. 25 election. Spread control is seen as unsustainable in a global rising rate environment. Lots of skepticism of ECB TPI.

LDI & Derivatives Clearing

It’s been posited that the clearing of Gilt interest rate swaps on central clearinghouses was part of the problem in the UK. Derivatives clearing exacerbated LDI cash crunch

A steep rise in Gilt yields after the UK government’s “mini-budget” on September 23 forced LDI managers to post huge amounts of margin to their swap counterparties as the value of their positions declined.

The argument seems to be that clearing requirements somehow changed the margin posting dynamic adversely.

Clearinghouses require variation margin, which covers mark-to-market changes to positions, to be posted in cash to minimise their own risks. That contrasts with transacting swaps bilaterally with bank trading desks, industry insiders say, which can afford greater flexibility to clients by allowing them to post Gilts or other bonds as margin.

I don’t buy it. Yes, it is possible that a bilateral counterparty MIGHT give a firm an extra day or so to post variation collateral, but they also might not. And the requirement to post cash, rather than other bonds, is weak; those bonds could always be lent/repo’d for cash, which would then be posted.

The final argument is that the pension firms

"A lot of pension funds don’t necessarily have the systems or experience to deal with that – it’s not a risk that’s been on their radar. Clearing has pushed that liquidity risk onto a part of the financial system where they have much less ability to understand and manage it, and don’t naturally run with large allocations to cash," he added.

I have no time for this argument.

LDI & Custody

It does appear that there was some operational issues that occurred, and perhaps exacerbated, the risk around the UK Gilt market during the recent LDI events. The FT reports Processing hold-ups at US custody bank exacerbated UK pension sell-off5.

The bank in question is Northern Trust.

Northern Trust, a large US custody bank, was overwhelmed by a slew of margin calls during the UK government bond market turmoil, hampering the ability of pension funds to raise cash, according to several people involved in the trades.

Processing hold-ups forced Northern Trust to redeploy staff from its US headquarters to help with the workload, according to two people with knowledge of the bank’s operations. Northern Trust acts as a depository for two of the biggest liability-driven investment managers caught up by the gilt sell-off, Legal & General Investment Management and Insight Investment.

Aside from the liquidity risk issue, there was a huge human resources processing component,” said a senior banker involved in the trades, adding that Northern Trust’s manual processing was a key blockage in the system.

An executive at a rival custody bank said Northern Trust used more manual processing than other players in the market, which predominantly use automated processing.

Another competitor said Northern Trust’s role as depository for two of the largest LDI managers created a concentration of stress on its operations.

And people say that operational risk is uncorrelated with market developments!

Nobel Prize in Economics

It’s fashionable in the Twittersphere to denigrate the Nobel Prizes for Diamond, Dyvbig and Bernanke. But if you worked at the NY Fed, and cared about systemic risk, this work was foundational in understanding the risk and crafting remedies, along with luminaries like Kindelberger, Fisher, Minsky and Galbreith.

Anil Kashyap has a nice piece summarizing the research Explaining the Rationale for the 2022 Nobel Prize in Economics. OIf course, Charles Kindleberger had a different take (worth reading!)

Tyler Cowen has a very nice writeup on Bernanke’s contributions in The economic contributions of Ben Bernanke

Frances Coppula has perhaps the best critique of awarding them the prise that I have read.

Education

A Stylized History of Quantitative Finance (Youtube)

This is a presentation by Emanuel Derman. Derman is at least a demi-god in the risk management world. Must watch for any serious student of quantitative risk management.

What I’m Listening to Today

49 years ago today, Bob Marley’s classic Burnin was released. The Downward Trends lives.

Farley, The Bond Market Is Already Broken - Stocks & Housing Are Next (Spotify: Forward Guidance)

Brettell & Barbuscia, UPDATE 2-U.S. Treasury asks major banks if it should buy back bonds, Reuters

Harris, Momentum Builds for Creating a Treasury Bond Buyback Program, Bloomberg

Brooks, Twitter stream

Walker, Processing hold-ups at US custody bank exacerbated UK pension sell-off, Financial Times