Perspective on Risk - Nov. 13, 2022

Paul Singer is Still Bearish; The ‘New’ Housing Market; Markets to Firms; Pos. Blockchain; Future Risk Report; Risk Management Is Too Boring; Crypto; OpRisk; Bet You Didn't Know; Research (on rats)

Welcome to my new subscribers. Saver you $8 for my charity drive.

Paul Singer is Still Bearish

A new letter from Elliott’s Paul Singer is purportedly making the rounds. I first wrote about Paul Singer’s bearishness in the Dec. 8, 2021 Perspectives, based on an article from the FT. He was pretty spot on; I highlighted this quote at the time

With all this in mind, it is puzzling that a growing number of otherwise sober money managers are in the process of boosting their allocations to riskier assets, rather than trying to figure out ways to make some kind of rate of return without giving back years of capital accretion in the next crash or crisis. Investors who have upgraded their risk levels, relying on policymakers to protect the prices of their holdings, may suffer significant and perhaps long-lasting damage when the government-orchestrated music finally stops.

You should read the whole (or at least the first half) Elliott letter; its is long and does get a bit whacky. Here are some extracts I thought worth highlighting (the bolding is my doing):

As for the prospects for monetary policy going forward, our overall judgment is that the central bankers will cause a recession in the global economy, during which (despite their current hawkish messaging) they will declare victory over inflation at the earliest possible moment (at whatever inflation rate coincides with that recession), and then gun the hell out of the global economy to restart it, hoping that it resumes growing without as much inflation as we have seen during this current cycle. It would be perfectly appropriate to call this “hope” a “big stretch.”

The Fed and its peers are trapped, and their actions are wholly reactive and experimental. Central banking is not a science; policymakers do not operate according to any precise knowledge, method or practical evidence (history, etc.). The stage, we think, has been set for a truly historic dénouement.

[A]n extraordinary confluence of extremes and problems have made possible a set of outcomes that would be at or beyond the boundaries of the entire post-WWII period. Investors should not assume that they have “seen everything” on account of experiencing the 1973 to 1974 bear market and oil embargo, the 1987 crash, the dot-com crash, or the 2007 to 2008 GFC.

To recap, we have: threats of nuclear war by a country that has more nuclear weapons than any other; a deliberate suppression of the supply of the world’s most important resources; the developed world drowning in ever-growing indebtedness and unrepayable entitlement obligations; the world’s greatest real estate and stock- market booms; the developed world’s greatest fall in bond prices; and a likely permanent negative inflection point in globalization.

The ‘New’ Housing Market

One of the first popular posts I wrote was on Zillow. You can read it here:

Zillow had transitioned from a firm that estimated the value of your house and made its money on advertising and referrals, to one that became a ‘market-maker’ buying and selling houses, in large part based on their algorithms. There are a couple of other firms that sought to get into this market, particularly Opendoor and Redfin.

I find this industry fascinating. In theory, this is a good market if you have the capital, liquidity (especially) and technology to pull it off. The bid/offer spread is pretty wide and the market is not particularly efficient. But can they get the capital, liquidity and risk management practices in place to intermediate effectively, do they understand that they are in a ‘moving’ and not a ‘storage’ business, and even more interestingly, will this result in a more efficient housing market with prices reaching new equilibrium clearing levels more quickly?

Now its Redfin’s turn to pull out of this business after experiencing losses.

Redfin to cut 13% of workforce and shut down home-flipping business RedfinNow (Geekwire)

Redfin will wind down its home-flipping program RedfinNow and lay off employees for the second time this year as it cuts expenses in response to a slowing housing market.

Redfin is one of a handful of real estate companies that invested heavily in iBuying to make real estate transactions more seamless. But it’s proving to be a difficult business, particularly with the broader market slowdown.

“We’ve tied up hundreds of millions of dollars in houses that you yourself wouldn’t want to own right now,” Kelman wrote. “Even before its overhead expenses, the RedfinNow properties segment will likely lose $22 – $26 million dollars in 2022.”

Redfin cited “the rising cost of capital” in their 8-K as the reason for shutting down the business. In other words, with Zillow’s issues investors have demanded higher risk-adjusted returns for firms in this business, and RedFin couldn’t make the economics work.

They have taken an $18 million writedown on inventory and offers to purchase totaling $357 million. This is only slightly more than 5%, so that seems to be pretty small relative to how much the price of houses must have moved.

In their ‘all-hands’ script, which is included in the 8-K, they cite two issues:

[T]he share gains we could attribute to iBuying have become less certain as we rolled it out more broadly, especially now that our offers are so low.

[T]he second problem is that iBuying is a staggering amount of money and risk for a now-uncertain benefit. We’ve tied up hundreds of

millions of dollars in houses that you yourself wouldn’t want to own right now. Even before its overhead expenses, the RedfinNow

properties segment will likely lose $22 - $26 million dollars in 2022. However small our iBuying loss may be compared to others, that loss

is still larger than we could afford to bear again.

After Zillow closed its ZillowOffers unit, RedFin CEO Kelman claimed they were more cautious in their offers1:

Kelman said Redfin uses software to help figure out RedfinNow offers, but it also uses “two layers of human governance.” It slows down the process of generating an offer but helps Redfin be more cautious.

The idea that a machine learning algorithm could get us into a pickle is one that all the iBuyers have worried about. We’ve tried to figure out the right balance between scale and caution, and Redfin is probably at the far end of caution

Might as well take a quick look over at OpenDoor. The company posted inventory valuation adjustments of $573 million ($431 million price adjustment + $142 million selling cost) on an inventory balance of 16,873 homes, representing $6.1 billion in value. So the total $573 million writedown equals about 9% of inventory not including unclosed purchases (so not apples-to-apples to the RedFin percentage).2 As an aside, read this footnote to see that OpenDoor recognizes the need to turn its inventory more quickly3.

Anyhow. let’s do some back-of-the-envelop math. This isn’t meant to be precise, just indicative.

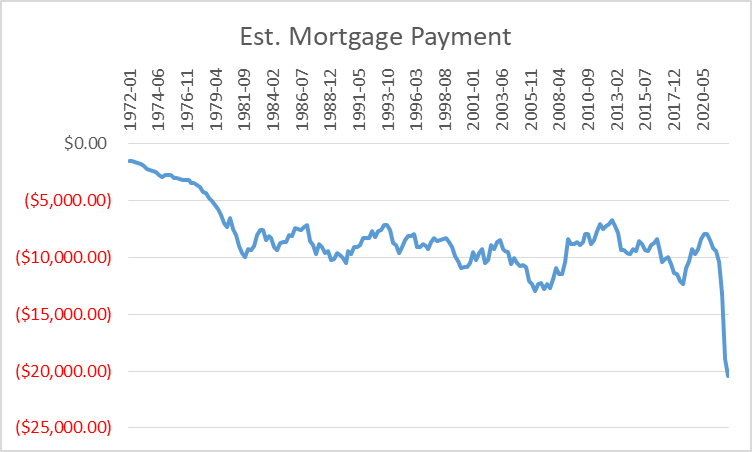

The rights way to think about housing is not to start with the home price, but instead with the mortgage payment amount. This is the constraining factor on most first-time purchases, and affects trade-up purchases as well. I pulled from FRED time series of 1) Median Sales Price of Houses Sold, and 2) 30-Year Fixed Rate Mortgage Average. I then calculated the mortgage payment assuming an 80% LTV ($454,900 median house price x 80% = 363,920) which is appropriate for the near-marginal buyer. You can see the large jump in payments that occurred with the 2nd quarter average when the 30 year rate reached 5.62%, up from, say, 2.87% one year earlier

Zooming lets zoom in. I’ve added a data point that reflects the current mortgage rate of 7.24% from bankrate.com.

Were rates to stay here (7.24%), to get mortgage payments back down to $10K would imply a mortgage of only $138,122, and a median house price at 80% LTV of only $172,652. That would mean house prices would need to fall by 62%! That implies prices equal to where they were in 1996. Again, this is nothing precise, just indicative. Lots of other factors involved.

So 10% writedowns are likely no where near what is necessary to clear the market.

Opendoor’s market capitalization has fallen to $1.3 billion, which is less than SHE of $2.2 billion), from about $14 billion one year prior. Clearly looks like it’s trading on its option value at this point.

Housing is dead for the foreseeable future. We need a combination of income inflation, housing price declines, mortgage rate declines, and time to overcome this issue. The actual reported market will take quite some time to reach a new equilibrium and press reports will lag.

From Markets to Firms

We’ve seen a lot of damage in the markets. But the realization of this damage, and the transition from ‘market’ risk to ‘institution’ risks usually has a lag, as most firms do not mark their positions to market on a daily basis, instead waiting for information from their investors. Similarly, certain aspects of liquidity take time to work through the system. Yes, margin calls may happen rapidly, but the extent of the changes on firm liquidity position is often not apparent until they issue published financial statements.

I suspect we will increasingly see discussion of the impact of the wealth destruction on firms , pension funds, etc. Perhaps this call is still a bit early, but nevertheless here it is.

Billions in Capital Calls Threaten to Wreak Havoc on Global Stocks, Bonds (Bloomberg)

As financial conditions tighten around the world, private-market funds are demanding that investors stump up more of the cash they pledged during the easy-money days of the pandemic.

Capital calls have accelerated this year, in particular for private credit funds, said one senior executive from an institutional investor overseeing more than $50 billion. Portfolios known as trigger funds, which request client capital once certain thresholds are met, have been among the most active in making capital calls

Positive Blockchain

All blockchain in finance is not cryptocurrencies.

First Industry Pilot for Digital Asset and Decentralised Finance Goes Live

The Monetary Authority of Singapore (MAS) announced today that the first industry pilot under MAS’ Project Guardian [1] that explores potential decentralised finance (DeFi) applications in wholesale funding markets has completed its first live trades.

Under the first industry pilot, DBS Bank, JP Morgan and SBI Digital Asset Holdings conducted foreign exchange and government bond transactions against liquidity pools comprising of tokenised Singapore Government Securities Bonds, Japanese Government Bonds, Japanese Yen (JPY) and Singapore Dollar (SGD).

A live cross-currency transaction [2] involving tokenised JPY and SGD deposits was successfully conducted. In addition, a simulated exercise was performed involving the buying and selling of tokenised government bonds.

This Tweet stream by @TyLobban has a number of the details

AXA Future Risk Report

For those of you that like these things, AXA does a pretty good job (good marketing).

The Key Lessons in the Executive Summary are interesting if not surprising:

Climate change, geopolitics and energy are forming a new nexus of risk

Economic risks are becoming more serious and fuelling social tensions

People feel more risk averse amid rising vulnerability and erosion of trust

Risk Management Is Too Boring

[00:01:00] Constance Wang: Hi guys. I'm Constance, I'm the CEO of FTX and the co-CEO of FTX Digital Markets. … I joined Credit Suisse, but was totally bored in banking industry and moved to crypto two years later and joined SIM to build out FTX since the beginning of 2019.4

Somehow, Constance Wang went from a risk/compliance role at CS to the COO of FTX.

Watch these short videos and tell me that anyone did any due diligence before investing:

Crypto Update

Crypto Confidence Soars After CEO Defrauds Customers Just Like Real Bank (The Onion)

Man Who Lost Everything In Crypto Just Wishes Several Thousand More People Had Warned Him (The Onion)

Hmm. This does not look like a normal market, does it. One of the repeated indications of fraud is the distribution of results centering on round numbers. 40K, 30K, 20K… This looks like a variant of Benford’s law applied to a supposedly free market.

Operational Risk

KFC apologizes after German Kristallnacht promotion (BBC)

KFC has apologised after sending a promotional message to customers in Germany, urging them to commemorate Kristallnacht with cheesy chicken.

The fast-food chain sent an app alert on Wednesday, saying: "It's memorial day for Kristallnacht! Treat yourself with more tender cheese on your crispy chicken. Now at KFCheese!"

The fast food chain said the "automated push notification" was "linked to calendars that include national observances".

Bet You Didn’t Know

Binance is an investor in the Twitter takeover

Gary Wang is/was the CTO of FTX. Only the back of his head is pictured on the FTX website (Terry, why didn’t we think of that when redoing the NY Fed’s site).

This picture does show up on golden.com.

Some Interesting (or Fun) Research

Bull, bear, or rat markets: Rat “stock market” task reveals human-like behavioral biases. (APA PsychNet)

[W]e developed an experimental “stock market”’ task in which cohorts of 4 rats drove asset prices up and down by selecting and subsequently buying, selling, or holding “stocks” to earn sweet liquid reward.

Rats also tended to respond suboptimally following a loss, which corresponded to an increase in risk-seeking behavior characterized by a bias against the optimal “hold” option in that context. Rats’ choice of the sell option demonstrated a robust tendency toward realizing gains more quickly than losses

Our results indicate that rats exhibit behavioral biases similar to human investors, emphasizing the suitability of the rat stock market model to future work into the behavioral neuroscience of suboptimal financial decision-making.

[bp: They did not determine if rats were better or worse traders than humans, though.]

We examine social media attention and sentiment from three major platforms: Twitter, StockTwits, and Seeking Alpha. We find that attention is highly correlated across platforms, but sentiment is not: its first principal component explains little more variation than purely idiosyncratic sentiment. We attribute differences across platforms to differences in users (e.g., professionals vs. novices) and differences in platform design (e.g., character limits in posts). We also find that sentiment and attention are both positively related to retail trading imbalance, but contain different return-relevant information. Sentiment-induced retail trading imbalance predicts positive next-day returns, in contrast to attention-induced retail trading imbalance, which predicts strongly negative next-day returns. These results highlight the importance of distinguishing between social media sentiment and attention, and suggest caution when studying the social signal through the lens of a single platform.

There’s one really interesting development, which is sort of backwards from the way markets normally develop. OpenDoor is moving at least in part from being a principal to all of their transactions to being a broker, whereby they match up buyers and sellers. This is their “new marketplace exclusives, which is our third-party product, where we connect a seller with one of our buyers and facilitate the transaction.”

[W]e are focused on improving the health of our inventory by accelerating the resell of homes we made offers on during Q2.

[W]e are executing on operational and platform changes that we expect will increase our resell velocity and reduce inventory hold times.

[W]e have accelerated our clearance rate versus the market to more than double that of a quarter ago and are on track to have sold or be in resell contract on approximately 65% of these homes by year-end.

Source: Opendoor Technologies Inc. (OPEN) Q3 2022 Earnings Call Transcript

Martinez, Breaking the Bias in Fintech, Trading and Crypto, Alpaca