Perspective on Risk - Nov. 10, 2022 (FTX brief)

Quick note on FTX

I’ve been asked by a couple of folks for my thoughts here. I’m going to keep it as short as possible, as 1) events are still unfolding, 2) initial information is often incorrect, and 3) others (Matt Levine, Frances Coppula, Amy Castor) have written more insightfully. If you really want the details, read the links.

I wrote about crypto in three prior Perspectives:

Background & Jargon

FTX is a cryptocurrency derivatives exchange that offers futures, leveraged tokens and OTC trading.

FTX is backed by Alameda Research, a ~$100million AUM quantitative cryptocurrency trading firm. Within a year, Alameda Research became the largest liquidity provider and market maker in the space. Alameda trades $600 million to 1 billion a day, accounts for roughly 5% of global volume and is ranked 2nd on the BitMEX leaderboard.

FTT is the exchange token of FTX. … FTT is the backbone of the FTX ecosystem. We have carefully designed incentive schemes to increase network effects and demand for FTT, and to decrease its circulating supply.

FTT was launched on May 8, 2019

The Players

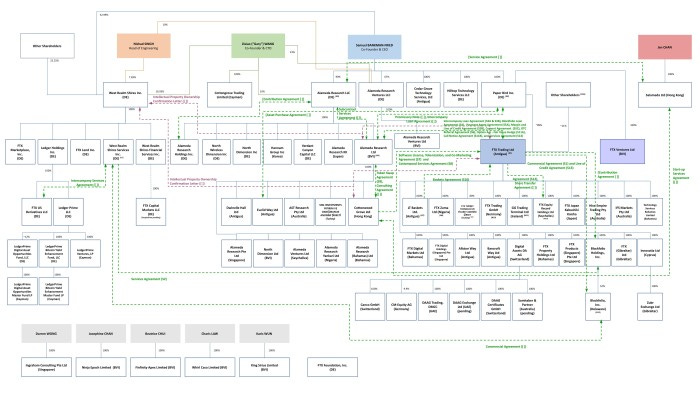

FTX, the exchange, and Alameda Research, the HF/liquidity provider, are both owned/controlled by Sam Bankman=Fried. Bloomberg has a nice description of the complex set of companies owned by SBF. Untangling the knotty empire of Bankman-Fried and FTX

Binance is a competitor exchange founded and owned/controlled by Changpeng “CZ” Zhao.

Binance is the largest exchange; FTX was second.

How did the Relationship Between FTX and Binance Begin?

From Reuters:

Six months after FTX’s launch, Zhao bought 20% of the exchange for about $100 million, a person with direct knowledge of the deal said.1

When FTX in May 2021 applied for a license in Gibraltar for a subsidiary, it had to submit information about its major shareholders, but Binance stonewalled FTX’s requests for help

By July of that year, Bankman-Fried had tired of waiting. He bought back Zhao’s stake in FTX for about $2 billion, the person with direct knowledge of the deal said. Two months later, with Binance no longer involved, Gibraltar’s regulator granted FTX a license.

That sum was paid to Binance, in part, in FTX’s own coin, FTT, Zhao said last Sunday

Alameda Suffers a Loss

This May and June, Bankman-Fried’s trading firm, Alameda Research, suffered a series of losses from deals, according to three people familiar with its operations. These included a $500-million loan agreement with failed crypto lender Voyager Digital, two of the people said. Voyager filed for bankruptcy protection the following month, with FTX's U.S. arm paying $1.4 billion for its assets in a September auction.

Seeking to prop up Alameda, which held almost $15 billion in assets, Bankman-Fried transferred at least $4 billion in FTX funds, secured by assets including FTT and shares in trading platform Robinhood Markets Inc, the people said.

Frances Coppula has a nice writeup The FTX-Alameda nexus. How did it all go bad so fast?

The short answer is - it didn't. The hole in FTX's balance sheet has existed for a long time. We don't know exactly how long, but the size of the estimates (ranging from $6-$10 billion) suggests several months if not years. Sam has been trading while insolvent. He's not the only crypto oligarch to do so: Celsius's Mashinsky also traded while insolvent for an extended period of time.

Coindesk Leaks Alameda’s Balance Sheet

Here is the Coindesk report: Divisions in Sam Bankman-Fried’s Crypto Empire Blur on His Trading Titan Alameda’s Balance Sheet

That (Alemeda’s) balance sheet is full of FTX – specifically, the FTT token issued by the exchange that grants holders a discount on trading fees on its marketplace. While there is nothing per se untoward or wrong about that, it shows Bankman-Fried’s trading giant Alameda rests on a foundation largely made up of a coin that a sister company invented, not an independent asset like a fiat currency or another crypto. The situation adds to evidence that the ties between FTX and Alameda are unusually close.

There are more FTX tokens among its $8 billion of liabilities: $292 million of “locked FTT.” (The liabilities are dominated by $7.4 billion of loans.)

Amy Castor notes that the size of the Alameda’s position relative to the market is huge:

$5.8 billion is actually 180% of the circulating supply of FTT!

The Death Spiral

Matt Levine does a great job of explaining what is going on here: FTX Had a Death Spiral. So does Frances Coppula: The FTX-Alameda nexus. He explains how this all WOULD work if the exchange were a traditional bank or broker-dealer.

FTX issues a token called FTT. The attributes of this token are, like, it entitles you to some discounts and stuff, but the main attribute is that FTX periodically uses a portion of its profits to buy back FTT tokens. This makes FTT kind of like stock in FTX: The higher FTX’s profits are, the higher the price of FTT will be. 8 It is not actually stock in FTX — in fact FTX is a company and has stock and venture capitalists bought it, etc. — but it is a lot like stock in FTX. FTT is a bet on FTX’s future profits.

But it is also a crypto token, which means that a customer can come to you and post $100 worth of FTT as collateral and borrow $50 worth of Bitcoin, or dollars, or whatever, against that collateral, just as they would with any other token.

If you think of the token as “more or less stock,” and you think of a crypto exchange as a securities broker-dealer, this is completely insane. If you go to an investment bank and say “lend me $1 billion, and I will post $2 billion of your stock as collateral,” you are messing with very dark magic and they will say no. 9 The problem with this is that it is wrong-way risk. (It is also, at least sometimes, illegal.) If people start to worry about the investment bank’s financial health, its stock will go down, which means that its collateral will be less valuable, which means that its financial health will get worse, which means that its stock will go down, etc. It is a death spiral. In general it should not be possible to bankrupt an investment bank by shorting its stock. If one of the bank’s main assets is its own stock — is a leveraged bet on its own stock — then it is easy to bankrupt it by shorting its stock.

Binance Starts a Run

The Alameda FTT are Actually FTX Customer Deposits

Now the BIG problem is that it’s asserted that the FTT on Alameda’s balance sheet is actually FTX’s customer funds that were reportedly under custody.

Frances Coppula explains a possible motivation:

The exchange has lots of customer assets that aren't earning anything. If he puts those customer assets to work, he can earn far more from his exchange customers. And he's got an obvious vehicle through which to put them to work. The hedge fund. If he transfers customer assets on the exchange to the hedge fund, it can lend or pledge them at risk to earn megabucks.

One problem is

the exchange promises that customers can have their assets back on demand, which could be a trifle problematic if they are locked up in leveraged positions held by the hedge fund. But this is crypto. There's an easy solution. The exchange can issue its own token to replace the customer assets transferred to the hedge fund. The exchange will report customer balances in terms of the assets they have deposited, but what it will actually hold will be its own token. If customers request to withdraw their balances, the exchange will sell its own tokens to obtain the necessary assets - after all, crypto assets, like dollars, are fungible.

For this to work, however, the token must reliably hold its value. So the exchange creates more of the tokens than are needed to replace customer balances, and the hedge fund actively buys and sells them on the exchange, thus creating a market in the things and pumping the price. The price rockets, inflating the balance sheets of both the hedge fund and the exchange, and making $billions in unrealised profits for Joe and his investors - of whom there are suddenly a whole lot more, including some exceedingly respectable institutional investors.

From Levine:

The reason for a run on FTX is if you think that FTX loaned Alameda a bunch of customer assets and got back FTT in exchange. If that’s the case, then a crash in the price of FTT will destabilize FTX. If you’re worried about that, you should take your money out of FTX before the crash. If everyone is worried about that, they will all take their money out of FTX. But FTX doesn’t have their money; it has FTT, and a loan to Alameda. If they all take their money out, that’s a bank run.

And all of this is self-fulfilling

One way Alameda can respond is by issuing more FTT tokens to back the FTX customer assets. This creates the price death spiral. From Coppula:

When the value of the token crashes, a gaping hole opens up in the exchange's balance sheet. On the liabilities side are its customers' assets, whose value has not changed (well, not as much as the value of the token, anyway). But the asset side consists mainly of the devalued token. It's not difficult to see that the further the token's price falls, the bigger the gap between the exchange's assets and liabilities.

Furthermore, because the token's price is falling, the exchange has to create more tokens in order to honour customers' withdrawal requests, pushing the price down even more. And the crashing token price frightens customers, who flock to withdraw their deposits, forcing the exchange to create more and more tokens. The run stops when the token price falls so much that the exchange is unable to buy assets and is forced to suspend withdrawals. But by this time the exchange is deeply, deeply insolvent. For a big exchange, the gap between assets and liabilities can easily amount to billions of dollars.

This is the same "death spiral" as the one that killed off the Luna and UST tokens back in May. There is no way of recovering from it. Injections of funds will merely delay the inevitable. It is a crisis of solvency, not liquidity.

FTX is an exchange, and Alameda a hedge fund. But together, they were doing shadow banking - unregulated, risky deposit-taking and lending. And because they are owned by the same person, and are closely connected in other ways too, they really should be considered as one organisation. FTX-Alameda, Celsius and Voyager are brothers under the skin, and their fate - and that of their owner-managers - will be the same.

Or as Levine puts it:

One other point here is that if this is the story, then it is not a liquidity crisis but a solvency one. That is, the problem is not a timing mismatch, in which FTX’s customers asked for their cash back but FTX did not have enough ready cash because it had long-term but money-good loans out. The problem is that FTX took its customers’ money and traded it for a pile of magic beans, and now the beans are worthless and there’s a huge hole in the balance sheet.

FTX Investors

Reports indicate that the following firms invested in either the B or C rounds by FTX: Sequoia, BlackRock, Tiger Global, Insight Partners, Paradigm and The Ontario Teachers’ Pension Plan Board. The latest round had an indicated value of $32 billion.

Sequoia has written its position to zero, and its letter to investors has leaked: Sequoia Note

Spillover and Margin Calls

JPMorgan Team Says Crypto Markets Face ‘Cascade’ of Margin Calls

A “cascade of margin calls” is likely underway given the interplay between the exchange, its sister trading house Alameda Research and the rest of the crypto ecosystem, a team led by Nikolaos Panigirtzoglou wrote in a note.

As is usual at this time, you sell what is most liquid first.

SBF Tweets “I’m Sorry”

There Will, Unfortunately, Be Calls For Regulation

IMO, better to leave this as caveat emptor for the moment. I don’t know how many laws were broken, but certainly very risky dealings.

The entire crypto industry seems to have elements of a pyramid scheme, a Ponzi scheme (with a thin legal veneer), and a pump-and-dump scheme (coin issuance).

Tether

One thing that I haven’t yet seen discussed is that Alameda was important to the stablecoin Tether: SCOOP: Tether minted most USDT to just 2 firms — Alameda and Cumberland

Over two-thirds of all Tether minted across multiple years went to just two crypto companies — Alameda Research and Cumberland Global, owned by Chicago-based trading firm DRW — sources familiar with the matter exclusively told Protos.

Berwick, Wilson, EXCLUSIVE Behind FTX's fall, battling billionaires and a failed bid to save crypto, Reuters