Perspective on Risk - May 13, 2022

YTD Returns; Pension Returns; This Can’t Be Good For The Mortgage Warehouses; Real World Inflation; 'Core' PCE-measured Inflation; Inflation and Market Returns

So…where are we?

The working hypothesis is that we have liquidity-inflated markets in a world where the marginal effect if deglobalization. Inflation is running high due to both ‘transient’ factors and core wage-price spiral dynamics.

In this environment the Fed is going to be reducing liquidity by raising rates quite rapidly, and by reducing its portfolio holdings. Markets have anticipated (and reacted) to this pace and brought forward the rate increases, and repriced financial assets.

Real asset prices (housing, autos, oil, commodities) are rising; financial asset prices are receding. Climate change and the Ukraine war are exacerbating these trends.

YTD Returns

Pension Returns

Pensions’ Bad Year Poised to Get Worse (WSJ)

Losses across both stock and bond markets delivered a double blow to the funds that manage more than $4.5 trillion in retirement savings for America’s teachers, firefighters and other public workers. These retirement plans returned a median minus 4.01% in the first quarter, according to data from the Wilshire Trust Universe Comparison Service expected to be released Tuesday.

However, if discount rates used are dynamic, much of the loss may be offset by rising discount rates on the liabilities [bp]

Also, just wait for HF and PE marks to come through in the 2nd and 3rd quarters [bp]

Larger loss than LTCM, but not nearly as leveraged.

This Can’t Be Good For The Mortgage Warehouses

I doubt we’ll have the same problems we did in 2008, but clearly there are some losses to be born in the RMBS space.

Real-world Inflation

The Fed’s (and therefore the market’s) favorite inflation gauge, the ‘core’ PCE deflator excludes things that most of us care about: food and energy.

We have a problem with both oil and foodstuffs. On energy, there is a diesel shortage occurring, primarily in Europe, but potentially here in the US as well. Diesel, of course, is used in both truck and rail shipping, which could raise supply chain costs.

Natural gas is also the critical input to ammonia fertilizer production.

The US is also facing a drought. This is affecting foodstuffs.12

Conditions have split across the Great Plains, with western parts deteriorating and eastern parts often drought-free (see western vs. eastern Oklahoma). The Southwest continues to be dry and windy—and now heat is moving in. As of May 10, 2022, 44.38% of the U.S. and 53.02% of the lower 48 states are in drought. (drought.gov)

‘Core’ PCE-measured Inflation

So there is some good (not great) news here. The market seems to be pricing in declining inflation over the next two years. Over a 5 year horizon, the market prices in a return to the Fed’s target level.

Housing represents about 1/3rd of the PCE deflator. Motor vehicles (new and used cars) account for another 6%. These two sectors are the principle sectors affected quickly by Fed rate policy.

Remember, this tightening cycle won’t be over until the Fed crushes the RMBS market and housing prices stabilize.

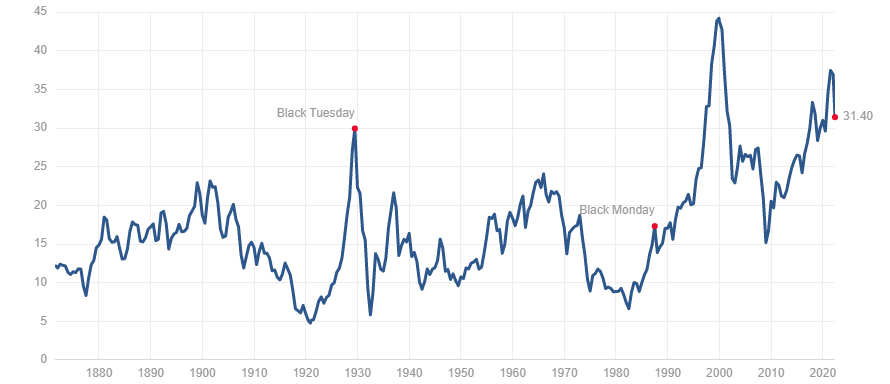

Inflation and Market Returns

CAPE has fallen from its high of nearly 40 to a current level of ~30. Still a long way to go to return to ‘normal.’

A CAPE of 30 predicts a 10 year forward return of ~4% (+/-2%), up from 0% at 40. Meb Faber notes that the highest CAPE on record when inflation was >5% is 23 (so 24% lower from here)

Moving the US5y5y real yield from -50bp to +50bp could take 12 month fwd. earnings yield from 5% to 6% (or PE from 20 to 16.7), or another 15-20% down.

I have a follow-up piece on liquidity-driven markets that I will also be sending out soon. Sorry to inundate you - I must be bored or something.

Full disclosure: long $WEAT and $GCC

After I wrote this, it was announced that India will be prohibiting wheat exports. This will in the short term raise wheat prices, though it should be offset by lower wheat prices in the future.