We are currently in an extended period of implicit financial repression. The term was first widely popularized in economic circles by Ronald McKinnon and Edward Shaw in 1973 when discussing the economic performance of South Korea, though it had been in practice for generations.

financial repression occurs when governments implement policies to channel to themselves funds that in a deregulated market environment would go elsewhere. Policies include directed lending to the government by captive domestic audiences (such as pension funds or domestic banks), explicit or implicit caps on interest rates, regulation of cross-border capital movements, and (generally) a tighter connection between government and banks, either explicitly through public ownership of some of the banks or through heavy “moral suasion.” Financial repression is also sometimes associated with relatively high reserve requirements (or liquidity requirements), securities transaction taxes, prohibition of gold purchases, or the placement of significant amounts of government debt that is nonmarketable. In the current policy discussion, financial repression issues come under the broad umbrella of “macroprudential regulation,” which refers to government efforts to ensure the health of an entire financial system.

Financial repression serves to keep nominal interest rates lower than they would be in more competitive markets in order to reduce government debt burdens.

In the US of recent, the Federal Reserve has vastly expanded its balance sheet as a “captive domestic audience” and maintaining nominal interest rates below the level of inflation.

Now, to be fair, the Fed has always run some degree of minor repression. Here we graph the 3-month Constant Maturity Treasury less the Fed’s preferred measure of inflation (the PCE deflator) from 10/1/1982 to 10/1/2021. But as you can see from below, a fairly rapid increase in real rates is probably warranted and inevitable.

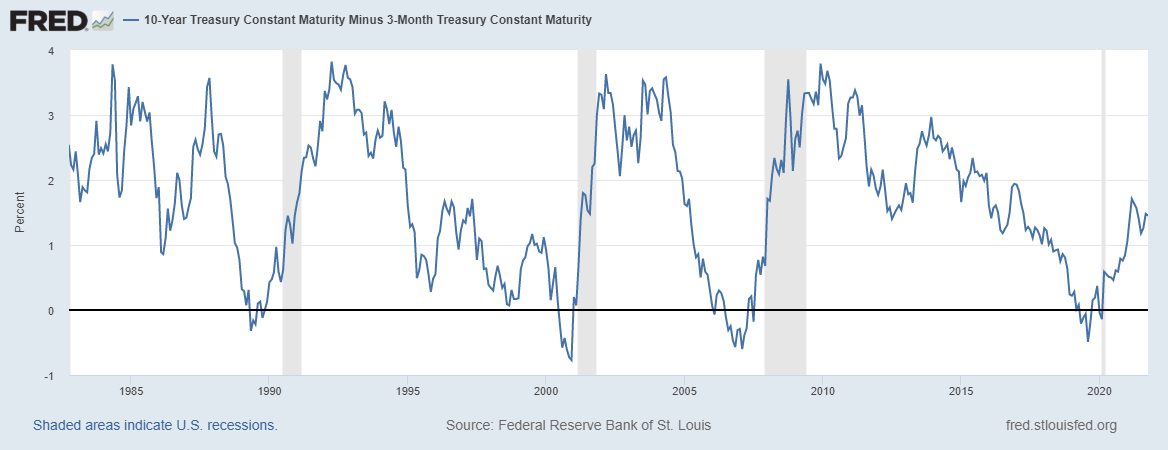

Next is a graph of the yield curve (10Y - 3M) for the same time period. You will see that recessions tend to occur when the 10Y/3M curve goes flat, and that the curve quickly steepens in response to a recession. Because of the zero lower-bound, the most recent steepening of the yield curve was truncated and replaced, in part, by the expanded program of quantitative easing. I think we can assume the Fed will raise the funds rate (perhaps quickly) to somewhere near the 10 year UST of ~2.3%, perhaps a little shy to keep the forwards upward sloping. 175 bp of tightening would be consistent with the discussed seven 25 bp hikes.

Let’s take a look at financial conditions. As measured by the Chicago Fed Financial Conditions Index, there has been a moderate tightening, but nothing yet consistent with a forthcoming recession.

I started out being more worried that the degree of YC steepening during significant negative real rates was unprecedented, but maybe walk away a bit more sanguine.

Update on Commodities

I’m probably obsessing on this more than my audience would find interesting, but I think there is a lot of interesting action going on here from both a risk management and a geopolitical perspective. Different issues in nickel, energy, wheat, and fertilizer; all have frictions that should increase costs.

The letter goes on to cite margin pressures at these firms from Clearing House requirements. In particular they not initial margin have increased by 6x within 6 months, and that variation margin moves by 10x on a daily basis. They also note, as discussed in previous notes, that firms do not have the option of reducing their positions as they are hedges for physical positions.

We think of oil as a global, moderately fungible commodity. What this highlights is the real friction inherent in delivering oil/gas to specific delivery hubs (e.g. WTI is ‘landlocked’; Brent is ‘seaborne’).

The Dallas Fed has published a nice piece. A key point they highlight is that Russian production cannot just be imported by China due to constraints on pipeline capacity.

So we have issues both on PRICE and on AVAILABILITY.

Again, this is currently mostly a European problem. The EFET is essentially looking for the Europeans to set up the equivalent on a 13(3) facility that the Fed has used in “unusual and exigent” circumstances. Steven Kelly has a substack that does a nice job of describing the issues with the Fed establishing a 13(3) facility here. Good chance we see some weaker hands get merged into national champion firms, the usual European way of handling things.

This is a nice segue back into the world of nickel.

What is likely going on now, behind the scenes, is the management of counterparty risk. The brokers are working with Tsinghan to minimize the open risk position, and to term out the crystalized loss. Similarly, the LME is working with the brokers to insure variation margin payments can be made.

The market continued to trade down-limit until, surprise, it traded immediately up-limit 2 days ago. Disruption events art being declared on a daily basis. This led to the LME cancelling more trades, and imposing new rules on order submission (22/090). There are still players trying to take advantage of the situation.

As usual, Zoltan Poszar said it best:

Commodities are collateral … …and every crisis occurs at the intersection of funding and collateral markets. Urals spot trading at a discount to WTI is like subprime CDOs going from AAA to junk. Will all commodities sourced from Russia trade at a significant discount? Is it possible that the Western boycott of Russian commodities is turning AAA commodities to junk? Does going from AAA to junk trigger margin calls? You bet!

The LME has announced that it will double its Default Fund.

The default fund is expected to increase to $2.075 billion from $1.1 billion in April as a result of the exchange’s monthly stress-testing exercise, an LME spokesperson said on Friday.

There are, of course, standards that central counterparties are expected to meet (Principles for Financial Market Infrastructures (PFMI)). The standards, however, do not specify a specific solvency standard for the clearing institution. The best they have to say is:

3.20.5. FMIs in a link arrangement should effectively measure, monitor, and manage their financial risk, including custody risk, arising from the link arrangement. FMIs should ensure that they and their participants have adequate protection of assets in the event of the insolvency of a linked FMI or a participant default in a linked FMI. Specific guidance on mitigating and managing these risks in CSD-CSD links and CCP-CCP links is provided below.

Clearinghouses face competing demands on the level of capitalization. On the one hand, capital at the clearinghouse demands a competitive rate of return, increasing the cost of using the clearinghouse custody and settlement services. On the other hand, clearinghouses can be exposed to counterparty risk of its members (when they fail to make required margin payments). Clearinghouses must decide how defensively they want to be capitalized, realizing their is no 100% guarantee it will be enough.

[The LME] has equity equivalent to just 1.05% of its balance sheet. Its contribution to the default fund it administers is just $23.2 million out of $1.36 billion, based on data at the end of 2020.

One issue we can see is when there is high correlation among broker counterparty risk, as in this case, because they have the same underlying customer with similar positions. Common counterparties are frequently an issue in markets, witness the Achegos failure in US equity markets. In general, regulators leave it to the brokers to try and understand when their clients may have similar positions at other firms, and to size their risk positions accordingly.

The LME’s regulator, the UK Financial Conduct Authority, has been notably quiet as events have unfolded. They initially blessed the actions of the LME:

As a regulated investment exchange, the LME is responsible for the maintenance of fair and orderly markets, … This may include taking steps such as a temporary suspension of trading at times of extreme price volatility.2

And now they are dragging out the standard need to learn lessons:

The London Metal Exchange and the rest of the market need to learn lessons from episodes such as this, it’s important they do so.3

At this point, it appears that the risk of a blow-up from nickel is being mitigated, but there is further risk in energy. But the FRA-OIS spread, which historically is a good indicator on inter-bank funding risk, has peaked and may indicate the worst is past (for now).

Not to get too lost in the weeds, but, related to the LME and metals, there is another thing to keep in the back of your mind.

If we ban metals from our warehouses, we’re not just making a decision about our business, we’re making a decision on behalf of the whole market, … Right now Russian metal isn’t sanctioned and that’s why it’s allowed in.

While the impact on copper would be significant, banning Russian metal could have an even more seismic impact in the LME’s nickel and aluminum markets, where producers MMC Norilsk Nickel PJSC and United Co. Rusal International PJSC supply a large proportion of the tradable brands.

And remember that EV engines need a lot of copper for their engines. Increasing demand meet supply shock.

Now let’s turn to food

Fertilizer prices are spiking.

Prices began rising last December due to domestic issues, including

Fertilizer is quickly becoming another sector where turmoil in supply fundamentals—both geopolitical instability and extreme weather—provides an opportunity for dominant firms to sustain extraordinary prices.

The $127 Billion globalchemical fertilizer market revolves around three macronutrients: nitrogen, phosphate, and potassium (or potash). … Deposits of potash and phosphates happen to occur wherever God or nature wanted to place them. … Mosaic, a top supplier of potash and phosphate, now enjoys around 90 percent of U.S. market share, according to two analysts of the sector, granting it enviable pricing power. … [F]our firms—Koch, CF Industries, Nutrien, and Yara-USA—represented three-quarters of total domestic nitrogen fertilizer production.

Russia and Belarus accounted for more than 40% of global exports of potash last year. Additionally, Russia accounted for about 22% of global exports of ammonia, 14% of the world’s urea exports and about 14% of monoammonium phosphate (MAP) - all key kinds of fertilizers. A larger portion of these exports went to the developing world, Brazil being a major food exporter.

Nitrogen fertilizer is based on natural gas, and in the US encouragement of biofuels led to growth in nitrogen fertilizer use for corn production. In Europe, as you might imagine, with the Russian sanctions, producers are either in the East, or gas is being prioritized for other uses.

Yara — which is the big fertilizer producers in Norway — is curtailing its production of fertilizer because of the natural gas price surge.4

Making matters worse, in February the Commerce Department imposed countervailing duties on some nitrogen imports finding that:

Russia, Trinidad and Tobago have been “dumping” urea ammonium nitrate (UAN) in the U.S. at below-market prices.5

Farmers will respond to these market forces by switching to crops that require fewer nutrients, cultivating less acreage, or simply use less fertilizer, a strategy that will reduce yields. Just what we need: incentives to grow less when the world’s largest exporters of wheat are off-line.

The government could do two things immediately: repeal these duties, and remove the requirements and incentives that promote the use of corn for biofuels.

Which Brings Us To Wheat

Wheat, at this point, is more of a geopolitical issue than an immediate financial market concerns. Reportedly, Russia and Ukraine export up to 14% of the calories consumed in the world.

Econometric evidence from this work indicates that after 2008 the relationship between fertilizers and corn prices increased.6

Joe Weisenthal and Tracy Alloway have an excellent Odd Lots interview (transcript) with Scott Irwin, an agriculture economist at the University of Illinois, about what he calls the biggest disruption he’s seen in his career. I doubt I can do justice to the details of the interview, and encourage you to listen to it if interested in details.

Question: So how big a deal is Russia invading Ukraine from a grains or agricultural perspective?

Ukraine in recent years has planted about 59 million acres of their top six crops: wheat, sunflower, soybeans, corn barley, and what they call rapeseed. So how big is that? And that's what's under threat of potentially not being planted at all. This spring due to the war, that's almost exactly equal to the total planted area of Illinois and Iowa.

Then they have on the other side, Russia, they're not going to probably have, you know, any problems growing their crops this year. The question is how much of it will be available to the world markets? Russia is the world's largest exporter of wheat. And again, the way I try to put that into perspective, well, you know, with U.S. production, what, would it take for U.S. wheat production to replace what's lost potentially for Russia? Well, Kansas is our biggest winter wheat producer here in the United States and it would take 4 million Kansases to replace what was lost.

Question: When we think about wheat, where does it go?

[T]he vast majority of wheat is actually used for human consumption — bread, pasta, crackers, things like that. This is potentially a huge problem for lower to middle income countries in North Africa and throughout the Middle East that have relied very heavily on the imports of wheat from this area.

Question: How does existing supply get allocated? Could we see a return or even more sort of food supply nationalism, and the idea that people are going to be keeping more of their own crops closer to home?

This is the great danger in global grain markets right now … when you get these huge, scary price spikes, particularly for food commodity, like wheat, that there's a tendency for a bit of panic to set in and countries begin shutting off exports to basically protect domestic supplies and protect domestic consumers. And that really leaves — importers particularly importers in the not rich countries — out in the cold. And we're already seeing that kind of thing beginning to happen.

Question: Is there something for the USDA or the White House to think about doing during such a time of high prices and tight supplies?

In the United States we have something that's called the Conservation Reserve Program that currently contains 22 million acres of previously cropped land that has been taken out of production, presumably because it's environmentally sensitive in terms of wind and water erosion or it has biodiversity, really a lot of it's for pheasant hunting. So there's that acreage that could be considered for maybe a special one time exemption from the current long term contracts that are required to place acreage into that reserve.

Will be watching this space.

I Love This NWS Map (Pray for Texas)

From March 21: Flood, tornado, red flag (dangerous wildfires), high wind and blizzard warnings in various parts of the state. Also coastal flood and high surf advisories.

Other Things We Should Be Talking About (But I’ve Run Out of Space)