Perspective on Risk - Mar. 17, 2022

Recession Probabilities; Risk Premiums; Changes to Risk Frontier; Enhanced Portfolio Optimization; Conditional Expected Returns; Counterparty Risk; Commodity Prices; Disclosure; More Existential Risks

Recession Probabilities

"In my view, the risk of a recession within the next year is not particularly elevated." — Jerome Powell yesterday

Risk Premiums

“Discount rates vary a lot more than we thought. Most of the puzzles and anomalies that we face amount to discount-rate variation we do not understand.” — John Cochrane

Sebastian Petric wrote a nice blog post at the CFA Institute that reminds us of John Cochrane’s seminal 2011 Presidential Address to the American Finance Association

Previously, we thought returns were unpredictable, with variation in price-dividend ratios due to variation in expected cashflows. Now it seems all price-dividend variation corresponds to discount-rate variation. We also thought that the cross-section of expected returns came from the CAPM. Now we have a zoo of new factors

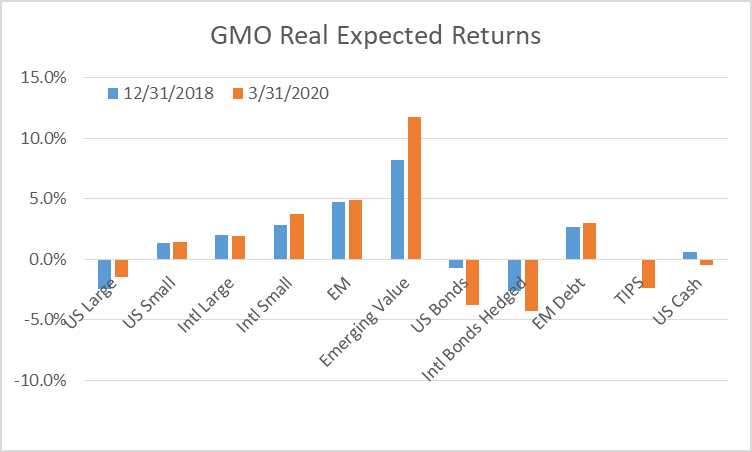

Two things I’ve liked to follow are the real forward return estimates from GMO (registration required) and the Efficient Risk Frontier (real) from Research Affiliates (more on this below). You can see the recent repricing of expected forward returns in their data (as prices decline expected future returns generally rise). I’ve been tracking this data for a few years.

First, let’s look at individual real asset-class expected returns, as estimated by GMO. As you can see, GMO was projecting negative real returns for US large cap equities and US Bonds prior to the covid disruptions.

Following the covid break, expected returns across all assets fell as asset prices were bid up due to QE (blue to orange). Asset-class returns have marginally improved as asset prices have fallen (and will look even better given the recent declines in the stock market). Still, by GMO’s estimates, asset prices still are extremely lofty suggesting negative of low forward returns.

For contrast, let’s look at their forward estimates from June 2010 to today: as you can see we have a long way to go to reach the forward expected returns that were estimated back then.

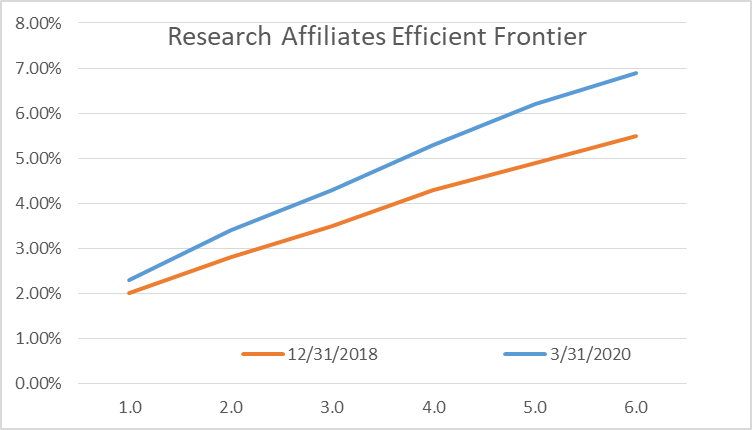

Now let’s turn to the risk efficient frontier. A little bit of apples and oranges as RA uses their own estimates and not GMOs, but the methodologies are more alike than different. Here are the RA real return frontiers; these show what they believe the efficient portfolio is at each of the stated variances. It may concentrate a bit in asset classes that it suggests has the best expected return (in this case both GMO and RA have for a while suggested overweight positions in EM value).

Goldman (pg 24; good read) is estimating that 2022 prospective nominal returns will be above their prospective 5 year returns

Another way to guage compensation for risk is to look at the implied Equity Risk Premium. Below is Goldman’s estimate (from the same above source) of the current level of the ERP. It suggests that the compensation for bearing risk remains at or above the long-run level given low and stable inflation.1

Changes to Risk Frontier

Earlier I mentioned the Efficient Risk Frontier (real) from Research Affiliates.

This first graph shows how forward returns tightened as markets rose prior to the Covid disruption.

In this second graph we can see how forward returns absolutely collapsed (blue line to red) as the Fed implemented QE, followed by improved forward real expected returns recently as the stock market has sold off (red to grey).

Enhanced Portfolio Optimization

Lasse Heje Pedersen, Abhilash Babu, CFA, and Ari Levine published in the Second Quarter 2021 issue of the Financial Analysts Journal Enhanced Portfolio Optimization. This is a paper for the technicians in my audience.

In summarizing the article, Simon Constable writes:

For the global asset portfolios, the EPO time-series momentum portfolio performs far better than the market portfolio and the 1/N approach. It also does better than such sophisticated portfolio approaches as “volatility-scaled long-only and standard time-series momentum portfolios.” The approach provided a large and statistically significant increase in realized Sharpe ratios and alpha. “These sophisticated benchmarks already deliver high Sharpe ratios,” the authors state. “Yet EPO beat it.”

For lay readers, Black and Litterman (“Global Portfolio Optimization,” Financial Analysts Journal, 1992) is the seminal article on portfolio optimization. It’s somewhat hard to implement. The paper claims that “EPO accounts for the noise in investors’ estimates of risk–return2 and, as a result, increases risk-adjusted performance.”

Conditional Expected Returns

From our earlier discussion, Cochrane asserts:

“There is a strong common element and a strong business cycle association to all these forecasts. Low prices and high expected returns hold in ‘bad times,’ when consumption, output, and investment are low, unemployment is high, and businesses are failing, and vice versa.”

Larry Swedrow summarizes a few papers on factor timing in Factor Investing Premiums and the Economic Cycle.

Interesting post with three takeaways:

… all risk strategies go through extended periods of poor (and unforecastable) periods of poor performance.

… if you are going to try to time factors, the research shows that employing momentum strategies has provided the most effective solutions.

Returns to value strategies in individual equities, commodities, currencies, global government bonds and stock indexes are predictable by the value spread. … In all asset classes, a standard deviation increase in the value spread predicts an increase in expected value return in the same order of magnitude (or more) as the unconditional value premium.

Financial Conditions Are Tightening

Counterparty Risk(s)

The large, predominantly Swiss, commodity trading firms have risks associated with Russian gas, likely taking gas and selling it through to third parties. Are the large commodity trading shops in trouble? Bond prices seem to suggest they are.

Gunvor is the 6th largest oil & product trader; they reportedly won rights to lift 9Mt of crude & products for 2021 from Rosneft. Trafigura has reportedly been holding talks with private equity groups to secure additional financing as soaring prices trigger margin calls, and I’ve seen reports that their Letter of Credits cannot clear due to sanctions.

Certainly they are managing through margin calls, and working with their bankers to remain liquid. European banks (ING, Credit Agricole, Unicredit, etc.) have long been active in commodities. The Graham-Leach-Bliley Act enabled US banks to scale up their “complementary” commodity operations, and Goldman Sachs and, to a lesser extent, Morgan Stanley brought a significant commodity presence to US banks when they became a BHC during the GFC.

Glencore’s bonds have held up, but we are beginning to see signs of possible dealer hedging in the CDS market.

In the Nickel markets, the LME has reopened trading in the nickel contract. Tsingshan Reaches ‘Standstill’ Deal With Banks on Nickel. Each day, the contract has traded down its 5-8% limit, leading to the LME declaring a “disruption event” per 22/064. The market remains in backwardation.

To ensure the integrity of the Monthly Average Settlement Price (“MASP”) and Notional Average Price (“NAP”) calculation averaging periods during periods affected by a Disruption Event (defined below), each Business Day within the period of a Disruption Event shall continue to count as a Business Day for the purposes of each pricing calculation. However, the Official Price / Closing Price for each affected Business Day will instead be the next available Official Price / Closing Price (as applicable) in the relevant averaging calculation. In this way, the number of Business Days within the relevant averaging period will remain the same overall.

The MASP matters because it is the basis for settling Traded Average Price Options (TAPOs), which are exchange traded and cleared contracts which settle financially based on the average of the daily LME Official Settlement Prices for the relevant month. This, again, may introduce further differences between OTC contracts and the exchange traded hedges.

From the FT:

Typically, authorities will push for the private sector to solve these issues, with differing degrees of sovereign support (depending on country). Still, Sid may get what he’s looking for.

Russia and Commodity Prices

Russia isn’t only a large exporter of energy (oil, gas, uranium) and wheat, but is also a major exporter of fertilizer. As expected, with sanctions, these have gone vertical too.

Disclosure

Tracy Alloway in the FT reviews a prospectus for euro-denominated bonds sold by Russia back in November of 2020 and due in 2027 that presages current events.

Supervisory assessment of institutions’ climate-related and environmental risks disclosures

More Existential Risks

Ancient sarcophagus found under Notre Dame cathedral in Paris

Spring Forward at Your Own Risk: Daylight Saving Time and Fatal Vehicle Crashes

My results imply that from 2002-2011 the transition into DST caused over 30 deaths at a social cost of $275 million annually.

Rising Risk of a Nuclear Apocalypse

From BCA: "The risk of Armageddon has risen dramatically. Stay bullish on stocks over a 12-month horizon."

I have so much more, but Substack says I’m at the limit.

The Goldman piece has an interesting exploration of whether there is mean-reversion in equity returns. They, perhaps counter intuitively, find none. See page 16.

As seen in our earlier discussion of risk premium.