Perspective on Risk - June 5, 2022 (Pt.1)

Liquidity-driven Markets; You’ve never been through QT;

You know, I said there’s storm clouds but I’m going to change it … it’s a hurricane. (Jamie Dimon)

You don’t need to be a weatherman to know which way the wind blows. (Bob Dylan)

Liquidity-driven Markets

Let’s all be clear; the Fed has only begun to withdraw reserves from the financial system. Since the Fed announcement of QT, banks have been adjusting their balance sheets The Fed’s balance sheet would decline by $775bn (including maturing T-bills) in 2022, $1 trillion in 2023 and $840bn in 2024, reducing its balance sheet from 36% of GDP to about 22% of GDP. This would still be higher than its pre-pandemic size of 17%.

Read that again: it is expected to take 31 more months just to reach the pre-pandemic starting point (which some will argue was not in any way ‘normal’).

To put things in perspective, it took 24 months for the Fed to reduce its balance sheet by $800 billion between October 2017 and September 2019 (in the wake of a $3.5 trillion expansion). The Fed is looking to move twice as fast. This will have large effects on financial, firm and counterparty liquidity, duration, creditworthiness and FX.

They do not have a choice because there is so much liquidity in the system. They have to remove some of the liquidity to stop speculation, to reduce home prices and stuff like that.” (Jamie Dimon)

As Joseph Politano succinctly notes in his substack Financial Conditions Are Rapidly Tightening:

[F]inancial conditions were tightening even before the FOMC officially raised interest rates due to the credible signal of upcoming tighter monetary policy. Since then, conditions have only gotten tighter: real interest rates are rising, corporate credit spreads are up, and equity risk premiums are higher. The result has so far been close to what the Fed was intending—a drop in inflation expectations and early signs of a price slowdown. However, the full effects of tighter monetary policy have not yet worked their way through the economy—and it will be critical to watch for shifts in the financial sphere as we enter the next stage of the economic recovery.

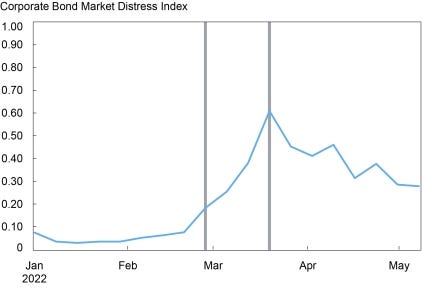

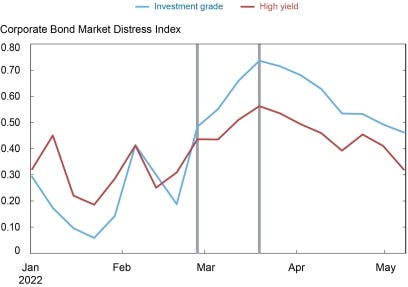

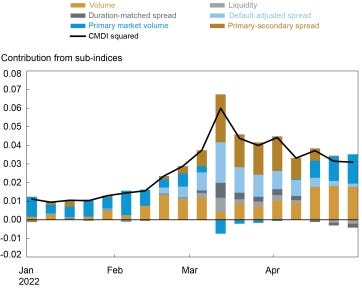

NY Fed posted a Liberty Street blog post How Is the Corporate Bond Market Responding to Financial Market Volatility? that provides some interesting information. They examine the evolution of the U.S. Corporate Bond Market Distress Index (CMDI)1, and index they created that “quantifies joint dislocations in the primary and secondary corporate bond markets and can thus serve as an early warning signal to detect financial market dysfunction.”

They note a material deterioration since the start of the year due to both the Ukraine invasion and the March FOMC meeting. They point out that the Ukraine invasion had a more material effect on financial conditions, likely due to increased uncertainty.

They further note that conditions for investment grade bonds deteriorated more than for junk.

What drove changes in the index?

[A] slowdown in issuance was the most noticeable contributor to the level of the CMDI at the beginning of 2022, the deterioration following the February 24 invasion of Ukraine can be initially attributed to trading conditions in the secondary market, with a decline in average trade size and the buy-sell ratio and an increase in turnover. The peak in the week ending on March 19 coincided with a deterioration in the default-adjusted spread sub-index, suggesting greater risk compensation for bearing default risk, and a deterioration in the spread between primary and secondary market pricing, suggesting a reduced willingness by market participants to intermediate in the primary market for U.S. corporate debt.

Joseph Wang explores how QT will be funded by the financial sector, and, by reviewing how MMF are likely to refinance their holdings, suggests that:

the financial system as currently configured will accommodate QT by draining bank deposits and reserves.

A $500b increase in the RRP and $400b in expected QT would drain the pool of bank deposits by ~$1t by year end. As the pool of bank deposits declines or stagnates, investors may need to continue to lower their selling prices to compete for the cash they want.

Twitter Dave provides a counter-argument, pointing out that the effects will be determined by how Treasury decides how to refinance maturing issuance. If, as he expects, Treasury chooses to fund primarily through bills (and bill issuance recently has been light so there is some evidence for his thesis), it will have a less immediate effect. And he argues this will be a superior was to minimize the ‘cliff effect’ of adding duration to the market.

Again, if interested, read the thread.

I think it’s important to read the entire Jamie Dimon quote, and not just linger on the hurricane analogy. Here is some of what he said, reordered by me:

The new part isn’t the raising of rates, it’s the QT.

You’ve never been through QT.

If you go back to 2010 and say who were the major buyers of treasuries all that time, it was the central banks, foreign exchange managers, banks who were topping up their liquidity profiles because we had to for the regulations.

All three won’t happen this go-around. Banks are topped up. Foreign exchange managers are topped up. The central bank will be selling, not buying, and governments have much more fiscal deficit to finance.

That’s a huge change in the flow of funds around the world.

This Will Be Painful

Cleveland Fed President Mester gave a speech titled An Update on the Economy and Monetary Policy, which had a concluding section:

Commitment and Follow-Through

As this period of recalibration of monetary policy continues, the FOMC will need to be resolute and intentional in removing policy accommodation to tighten financial conditions at the pace needed to get inflation under control. This will take fortitude. There will be bumps along the road. Financial markets could remain very volatile as financial conditions tighten further; growth could slow somewhat more than expected for a couple of quarters; and the unemployment rate could temporarily move above estimates of its longer-run level. This will be painful but so is high inflation. High inflation imposes a real burden on households and businesses, especially those that do not have the wherewithal to pay more for essential goods and services. I do not see the current situation as one involving a trade-off between our two monetary policy goals. If we fail to do what is necessary to get inflation down, we will not be able to sustain healthy labor markets over the medium and longer run, to the detriment of the public we serve. So in formulating my policy views, I will remain focused and committed to using our policy tools to achieve our monetary policy goals of price stability and maximum employment.

This conclusion is not an accident.

More to come in part 2; sorry for being verbose.

Boyarchenko, Crump, Kovner, and Shachar; Measuring the Forest through the Trees: The Corporate Bond Market Distress Index