Perspective on Risk - June 3, 2025 (Stablecoins, Part Deux)

Embedding A Narrow Bank; Walled Gardens & Open Worlds; Insolvency Provisions & Uninsured Deposits; Thoughts As A Regulator

The GENIUS Act may fundamentally reshape American banking by embedding narrow banks within traditional institutions—but the devil is in the details.

Some of you may have noticed that the May 28th Perspective on stablecoins was picked up by the FT Alphaville crew. That, of course, was a rather narrow piece focused on my long-standing obsession with Corrigan’s 1982 paper Are Banks Special?. Writing that piece sent me down a rabbit hole of thinking through the Genius Act and its implications. I did not welcome doing this. So, anyway, welcome to Stablecoins, Part Deux - Stablecoins, Narrow Banks & Financial Stability

What Is A Narrow Bank?

The Genius Act essentially allows the imbedding of a particular version of a narrow bank within the structure of a traditional bank.

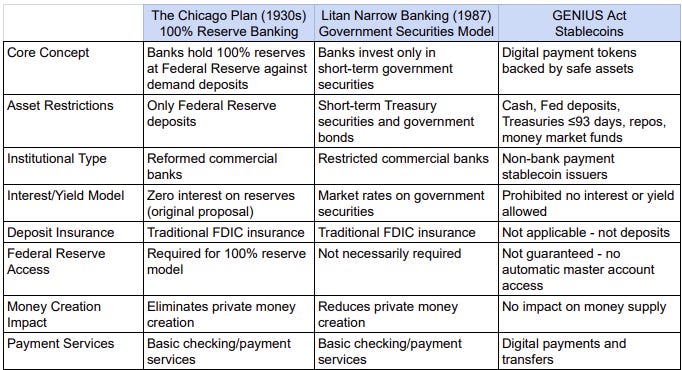

Narrow banking has a long history. It seems that in the 1930s there was a proposal for "100% Reserve Banking" called the Chicago Plan. The original Chicago Plan from the 1930s required banks to hold 100% reserves against deposits, with reserves held as deposits at the Federal Reserve. This plan aimed to separate money creation from credit creation, preventing banks from expanding the money supply through fractional reserve lending.

The idea of a “narrow bank” was raised again in the 1980s with the economist Robert Litan is a leading proponent.1 Littan’s proposal expanded the eligible assets to include short-term government securities. A bank, The Narrow Bank, was chartered in Connecticut, but ultimately denied a master account at the Federal Reserve. The Fed’s opposition to TNB was rooted in concerns that a full-reserve bank could destabilize the economy by challenging the Fed’s ability to regulate liquidity and interest rates.2

So, practically, we can say that narrow banks,

are limited to investing in a defined class of safe and liquid assets

separate deposit-taking/payment functions from lending and investment activities

seek to protection of deposits through full backing by high-quality assets

This is essentially what the Genius Act proposes. Stablecoin issuers may be within a bank, along-side a bank as an affiliate, or outside of the banking system altogether.

Going back to my Corrigan analysis, and the Fed’s concerns over The Narrow Bank, the Genius Act seems to overcome the concerns about interference with the monetary policy transition mechanism. By itself, the stablecoins will not force an unwanted expansion of Fed balance sheet. Stablecoin issuers will not automatically be granted Fed master account access. The Act allows a diverse reserve assets beyond Fed deposits, and prohibits interest payments that could create monetary policy complications.

Ring-Fencing The Stablecoin Issuer

The Genius Act calls for the ring-fencing of the stablecoin issuer. Ringfencing means to create a barrier to separate a specific portion of a company's assets or operations for a particular purpose. In bank supervision, we seek to ringfence the bank from the harmful effects of weak subsidiaries. Following the GFC, many countries now ring-fence foreign branches operating in their jurisdiction.

The Genius Act essentially creates a ring-fenced entity to issue stablecoins and hold the associated assets.

The EU's MiCA Regulatory Framework

The EU has already established a regulatory framework for stablecoins. The EU's Markets in Crypto-Assets (MiCA) regulation is broader than the Genius Act covering three classes of tokens: Asset-Referenced Tokens (ARTs), E-Money Tokens (EMTs), and "other tokens". Stablecoins would be EMTs.

One can’t fully compare Genius and MiCA until we see the OCC regulations. Both require 100% backing by eligible assets. Both require legal segregation of assets; there are differences in eligible assets, minimum liquidity requirements, asset maturity and, perhaps importantly, insolvency protection.

Walled Gardens Or Open Blockchain

So my understanding is that there are two (and maybe more) kinds of stablecoins in the world.

JPM Coin and Wells Fargo’s Digital Cash and Facebook’s (failed) Libra are exampled of “walled garden” stablecoins. They operate exclusively on closed, private blockchains and are used to facilitate B2B payments, treasury management, trade finance.

Then there are “open world” stablecoins; public stablecoins operating on open blockchain networks, freely tradeable across multiple platforms and accessible to broad user bases. These are the ones you may have heard of, like Tether and USD Coin.

It is unclear if banks will issue “open world” stablecoins. Presumably someone will try, and if so they may have a competitive advantage over non-bank stablecoins due to at least the implicit access to support from the regulated bank and indirect access to the safety net. Could regulators allow an “open-world” bank-issued stablecoin to fail?

Do regulatory requirements vary if a stablecoin is used exclusively in a “walled garden” as opposed to being issued in the “open world.”

Do we now live in the world of “free banking” where we will see a (further) proliferation of “open world” bank-affiliated and non-bank stablecoins? Will they all trade at par?

Genius Act Insolvency Provisions & Uninsured Deposits

The Genius Act

Prioritizes claims of holders of permitted payment stablecoins over all other creditors in the event a payment stablecoin issuer goes bankrupt.

Mandates expedited court review and distribution of reserves [segregated assets] to stablecoin holders.

What this means is that stablecoins holders come ahead of little old you and me.

If I were a corporation, at a minimum I would have my accounts at a banking institution that is a stablecoin issuer, and I would have a stablecoin account so that I could transfer my deposits into a stablecoin should distress occur. The fact that a stablecoin cannot pay interest means that I, as a corporate Treasurer, would probably keep most of my funds normally as deposits in order to earn interest. This would seem to be something of a subsidy to the stablecoin-issuing banks. As a bank, do I want to grow stablecoin custody as higher-priority liabilities are more valuable?

Conversely, could this increase the run-potential of the traditional banking franchise if my depositors can switch into protected stablecoins easily?

From the FDIC’s point of view, will this reduce recovery in bank failures due to stablecoin super-priority? Would this result in higher potential costs to Deposit Insurance Fund?

Thoughts As A Regulator

My first thoughts as a former Federal Reserve regulator and central banker interested mostly in financial stability went to Sections 23A/23B of the Federal Reserve Act. Sections 23A and 23B were designed to prevent banks from using federally insured deposits and access to the Federal Reserve's discount window to subsidize risky activities of their affiliates, thereby protecting the federal safety net and preventing conflicts of interest that could harm bank safety and soundness.

Affiliate Transactions

Section 23A imposes quantitative limits (10% of bank capital per affiliate, 20% total) and collateral requirements (100-130% depending on asset type) on "covered transactions" between banks and affiliates, while Section 23B requires all affiliate transactions to be conducted on market terms Federal Reserve Board - Section 23B. Restrictions on Transactions with Affiliates. However, the GENIUS Act appears to exempt stablecoin subsidiaries from these traditional restrictions, as

the holding company of a payment stablecoin issuer and 'sister' affiliates would not be restricted with respect to their business activities or relationships3

Traditional Bank Liquidity

This, then, would raise a few issues for me as a supervisor.

What is a reasonable share of bank deposits that come from stablecoin issuing activity? Can or should there be a limit?

What, if any, restrictions should be placed on a bank supporting its stablecoin issuer? Does it matter if it is within the bank or a separate affiliate? I still remember the liquidity puts that were a big factor in the GFC.

How do I think about the Supplemental Liquidity Ratio and the Net Stable Funding Ratio? Do I include or exclude stablecoin-related deposits?

The lack of explicit deposit size limits and broad liquidity support permissions suggest that the "narrow banking within banks" structure may not be as ring-fenced as traditional banking regulation would require for similar subsidiaries.

Next, how does the stablecoin business affect run risk? Can the stablecoin be run? Are traditional bank deposits of a stablecoin-issuing bank more vulnerable to running since they are subordinated to the stablecoin depositors interests? Can stablecoin activities cause a run on traditional deposits? Would weakness at the parent bank cause a run on the stablecoin? All things the regulators will need to think through.

Capital

The devil is in the yet-to-be-announced details. The Genius Act states:

may not exceed what is sufficient to ensure the permitted payment stablecoin issuer’s ongoing operations

subsection (a)(1)(A), section 171 of the Financial Stability Act of 2010 (12 U.S.C. 5371(a)(1)(A)) shall not apply.

12 U.S.C.5371(a)(1)(A), which is often referred to as the Collins Amendment to the Dodd-Frank Act, references the "generally applicable leverage capital requirements.” So here is the first nail in the Supplemental Leverage Ratio.

So the OCC can set bespoke, low-level capital requirements for the stablecoin-issuing bank-subsidiary. The unanswered question is whether they will require deduction of this capital from the capital calculations of the consolidated bank.

One can argue that the capital requirements should be zero. After all, how different is a stablecoin from a Treasury-only MMMF.

Operational risk

Stablecoins raise a number of operational issues. Given the prevalence of attacks in the “open world,” there will need to be higher cybersecurity standards for digital asset operations than traditional banking. I imagine there will need to be tailored Third-Party Risk Management of blockchain infrastructure providers, and specialized incident response procedures for blockchain-related operational failures. A Board-level committee with appropriate digital asset expertise will be mandated.

Compliance

The Genius Act includes Know Your Customer (KYC) requirements. The legislation mandates that permitted stablecoin issuers comply with the Bank Secrecy Act (BSA), which encompasses KYC, anti-money laundering (AML), and sanctions compliance obligations. This means issuers must implement identity verification, transaction monitoring, and reporting of suspicious activities.

As discussed before, “open world” stablecoins will represent a challenge.

There is a regulatory incompatibility between the principles of open, censorship-resistant finance and current KYC obligations. An “open world” stablecoin issued by a regulated bank can’t truly be open unless KYC and AML laws are redefined to accommodate that openness (e.g., shifting from strict identity controls to risk-based monitoring).

There are some possible solutions. Banks could allow transfers only between “whitelisted” accounts where KYC due diligence has been completed. Some “open world” tokens already operate with transfer restrictions. To maintain a degree of privacy, it might be possible to have an intermediary vouch for the KYC, though regulators will be REALLY loath to consider this. Transfer could be allowed, but there could be KYC restrictions on who could exchange stablecoins for dollars.

It strikes me that, if passed in current form and enforced, this will be a significant challenge to the existing “open world” crypto/stablecoin industry represented by USDC and Tether.

Current Bank Stablecoin Activity

A number of US banks have some degree of stablecoin activity already. JP Morgan Chase has JPM Coin, Wells Fargo has Digital Cash, Citigroup has Citi Token Services. JPM Coin is by far the largest. All are closed-loop “walled garden” stablecoins used primarily for internal cross-border payments and settlements within the bank's networks.

A Société Générale's subsidiary launched EUR CoinVertible (EURCV),a MiCA-compliant, fully collateralized, stablecoin. Unlike the US banks’ efforts, this is an “open world” stablecoin available on public blockchains.

JPM Coin

It is useful to examine JPM Coin.

JPM Coin is issued by JPMorgan Chase to facilitate instantaneous payments and account a digital representation of U.S. dollar institutional deposits held at the bank. A client deposits U.S. dollars into a designated JPMorgan Chase account, and an equivalent amount of JPM Coins is issued to the client on JPMorgan's proprietary blockchain. These JPM Coins can then be transferred to other eligible JPM Coin participants and holders can redeem JPM Coins for U.S. dollars at a 1:1 ratio from the bank.

The stablecoin is a liability of JPMorgan Chase N.A. It is not ring-fenced to the best of my research. No regulatory approvals were needed.

Concluding Thoughts

I really do think that the Genius Act is a step forward. It’s compliance requirements will challenge the existing industry competitively.

This is yet another defacto nail in the Supplemental Leverage Ratio; it might actually not require changing the law if banks can just gross-up their balance sheet through stablecoin funding to hold more short-dated bills.

Having banks issue stablecoins does, at least implicitly and in theory (I think), provide Federal Reserve access during times of stress. I worry a bit that there will be a subsidy effect for the biggest banks, and that FDIC insurance rates may not reflect the potential for larger losses should a stablecoin issuer fail.

As long as the stablecoins remain in the “walled gardens” the risks are probably easier to manage, but inevitably a US bank will issue an “open world” stablecoin and then things will get much more complicated.

Much will depend on the OCC’s timeliness and stringency in rulemaking and enforcement.

What Should Banks Do? (Brookings, 1987)

Squeezed: the Narrow Bank, the Federal Reserve, and the Future of Full-Reserve Banking (Southern California Law Review)

That image choice 🤝

Hot Shots! Part Deux is a fun movie.