Perspective on Risk - Feb. 27, 2024 (Commercial Real Estate - Part Deux)

Dudley/Ritholz on CRE; Shared National Credit Results; And so it begins… Cap Rates; Looking At The Banks; Bank Supervision & CRE; Head Office As NPL

Dudley/Ritholz on CRE

I wrote last week about the Dudley interview with Barry Ritholz. I thought I would highlight some of Dudley’s comments on CRE.

Ritholz: So, so Powell was asked… about the commercial real estate. … So this seems to be taking place in slow motion, but it seems like commercial real estate is a genuine risk factor certainly for some of the regional and community banks. How should we be contextualizing what’s been taking place with remote work and work from home and the slow return to office process that still has lots of vacancies in in urban centers?

Dudley: Yeah, I mean, I would define it more narrowly than commercial real estate. I would define it as office building space, because that’s really where you have very high vacancies rates, very underutilized resource and prices are coming down, especially for, you know, class B and class C buildings. Not the, the best stuff coming down quite significantly.

You know… this is sort of a slow burn rather than a fast burn because the problem typically arises not, you know, immediately it, arises when the mortgage has to be, or the commercial real estate loan has to be, refinanced. As long as the income on the property covers the interest on the loan, the borrower isn’t gonna default when the loan comes due though, the lender typically says, Hey, your building is worth, you know, 40% less than it was before. I’m sorry. We’re not gonna lend you as much money. You need to come up with more collateral. And at that point, the borrower might say, I don’t have the collateral, the building’s yours. And so then that, that crystallizes in a loss for the, for the commercial bank.

I think there are definitely commercial banks that are gonna have trouble due to their concentrated commercial office building portfolio. But I don’t view this as big enough or fast enough to really be, you know, systemic from a financial stability perspective.

Shared National Credit Results

Agencies issue 2023 Shared National Credit Program report

The Shared National Credit (SNC) program is where bank examiners review the largest syndicated loans in the banking system. This year’s results were recently published.

In CRE, the criticized rate increased, driven by office. But caution is warranted; these results are likely based on YE 2022 appraisals. I suspect we will see a material increase in both special mention and classified Office and All Other (which includes multifamily) in next years results.

And so it begins…

US Commercial Property Foreclosures Spike in January (Bloomberg)

There were 635 US commercial real estate foreclosures in January, up 17% from the previous month and roughly twice as many as in January 2023, according to a report from Attom.

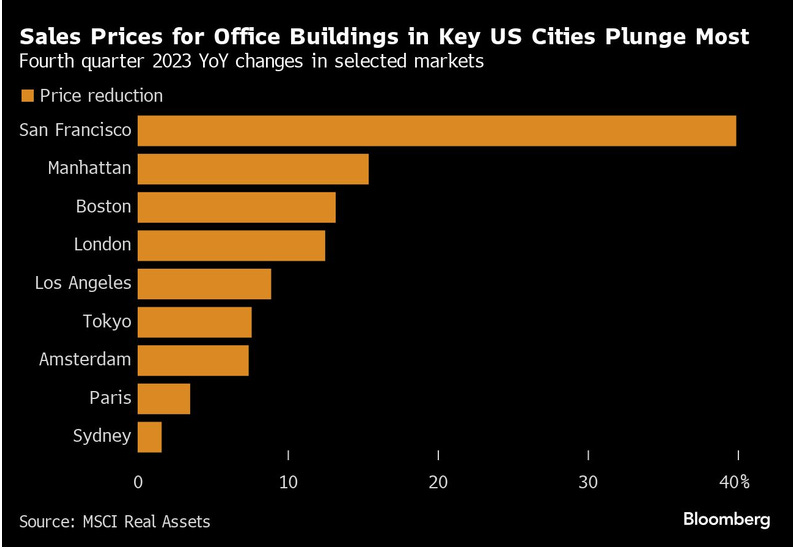

The Brutal Reality of Plunging Office Values Is Here (Bloomberg)

Across the country, deals are starting to pick up, revealing just how far real estate prices have fallen.

In Manhattan, brokers have started to market debt backed by a Blackstone Inc.-owned office building at a roughly 50% discount. A prime office tower in Los Angeles sold in December for about 45% less than its purchase price a decade ago. Around the same time, the Federal Deposit Insurance Corp. took a 40% discount on about $15 billion in loans it sold backed by New York City apartment buildings.

Sold for $1

360 Park Avenue (Park and 23rd Street)1

Fundamentals

Cap Rates Are Up; Office Is Ridiculously High

The 2024 U.S. Real Estate Outlook (Virtus RE Capital)

Office Vacancy Rates

National Office Vacancy Rate Climbed in 2023 to Record 19.7% (Trepp)

The national office vacancy rate increased last year by 200 basis points from 2022 to an all-time high of 19.7%, according to Cushman & Wakefield.

… the country's largest market, midtown Manhattan, which has 263.05 million square feet of space, had its vacancy rate increase to 22.3% from 21% in 2022. … Other large markets that had increases in vacancy included Los Angeles, whose rate climbed to 26.2% from 22.9%, and San Francisco, which carries the country's highest vacancy rate of 32.5%, an increase from 24.1% in 2022.

Debt Service Coverage Ratios (from Trepp)

Property Valuations

CRE Valuations Dropped 42 Percent on Average in 2023 (Commercial Observer)

CRED iQ analyzed 556 properties that were reappraised during 2023, since we were interested in the overall valuation impacts by quarter and property type.

In total, the average decline in value compared to the original valuation at issuance was 42 percent — remaining in the narrow range between 41 percent and 43 percent that prevailed throughout 2023.

CMBS

In the last cycle, delinquencies on commercial mortgage-backed securities peaked at more than 10% in July 2012, nearly four years after Lehman Brothers Holdings Inc. filed for bankruptcy protection. The current delinquency rates on securitized loans is 4.7%, according to Trepp.2

Looking At The Banks

Bad property debt exceeds reserves at largest US banks (FT)

Bad commercial real estate loans have overtaken loss reserves at the biggest US banks after a sharp increase in late payments linked to offices, shopping centres and other properties.

The average reserves at JPMorgan Chase, Bank of America, Wells Fargo, Citigroup, Goldman Sachs and Morgan Stanley have fallen from $1.60 to 90 cents for every dollar of commercial real estate debt on which a borrower is at least 30 days late, according to filings to the Federal Deposit Insurance Corporation.

For the big banks it’s likely an earnings hit, but for regional and smaller banks it may be a capital hit.

Valley National’s Real Estate Loans Are in Strong Shape, CEO Says (Bloomberg)

“We have not had to restructure one loan of that whole $2.8 billion,” he said. Competitors, meanwhile, have had to rework debt because of higher interest rates or changes in behavior by borrowers, Robbins said.

Talking his book. We’ll see.

Johannes Borgen (@jeuasommenulle on Twitter) had an interesting graph that highlights how the problems will be in the smaller banks (and CMBS)

And it affects foreign banks;

In Germany and Scandinavia there are banks with a large exposure to commercial real estate, and if they take a 15-cent writedown for every dollar they lend “not only are these banks not investment grade, they’re insolvent.”

Deutsche Pfandbriefbank, a Bavarian lender specializing in commercial real estate finance with a large exposure to the US, saw its bonds collapse this week after Morgan Stanley held a call with clients recommending they sell PBB’s senior notes.3

Germany’s Deutsche PBB and Aareal Bank AG have seen their unsecured borrowing costs climb as investors scrutinize their books for bad US loans. South Korean banks and asset managers, among the largest investors in European and US commercial buildings in recent years, are also bracing for a wave of problematic debt.

The issues have also hit Canada. Sun Life Financial Inc. saw the value of its US office investments plunge, with particularly pain around one San Francisco building. Pension fund CPPIB recently sold a stake in a Manhattan office tower for just $1, on top of the assumption of mortgage debt and working capital, according to a person familiar with the matter.4

Why does foreign bank ownership matter? Because once burned by losses some firms will withdraw from financing the US market. This reduces the supply of funding available for refinancing the available debt stack.

Pfandbriefe

Ah, Pfandbriefe. Brings back memories of negotiating the Basel Capital Accord. Had to understand the differences in how German securitization works. Pfandbriefe5 are essentially covered bonds; on-balance-sheet securitizations subject to German law collateralized with long-term assets. The underlying asset pools can be ‘dynamic’ subject to limitations. The bonds are typically initially Aaa at origination.

If I am correct, the German banks have a preferential capital rule that risk-weights Aaa and Aa+ tranches at 10%. If the Pfandbrief ratings are lowered below this, the weight increases to 20%.

US Property Fears Send German Lender Bonds Plunging (Bloomberg)

PBB’s junior bonds suffered a record slump on Tuesday but recouped some losses after the bank said on Wednesday it raised risk provisions and reported preliminary pretax profit for the full year that met estimates.

It also brings back memories of the subprime crisis. There we had German banks buying subprime securitizations through SIVs and conduits that they set up in Ireland, all to monetize expiring German state guarantees. Some of the same players are showing up: I always liked the name Landesbank Baden-Wuerttemberg.

To the extent Pfandbrief ‘covereds’ are impaired, this will affect the capacity to refinance real estate debt in Europe. Economic contagion perhaps to Landesbanks and Spahrkassen.

US Banks CMBS Positions

Using data from the National Information Center, I decided to take a look at BHC holdings of CMBS (stale data, as of 3Q2023).

Looking at the BHCs > $100 billion, two stand out for their exposures.

Charles Schwab had >7% of total assets (and >90% of total equity) invested in CMBS. Since the majority of their CMBS book is designated HTM, they had an unrealized loss of $2 billion (or 5.6% of total equity)

Fifth Third also had sizeable holdings with >6% of assets and >80% of total equity in CMBS. They account for their CMBS as AFS, so they’ve already taken $2.5 billion through capital.

The rest of these banks had less than 4% of total assets in this class.

Below the $100 billion threshold, perhaps two more banks stood out:

Comerica with 4% of assets and 68% of total equity; all AFS

BOK Financial, 6% of assets, 66% of total equity, all AFS

Bank Supervision & CRE

Supervision with Speed, Force, and Agility (Barr)

Let me turn to supervision of a specific risk: commercial real estate (CRE). The reduced demand for office space and higher interest rates have put pressure on some CRE valuations, particularly in the office sector. Supervisors have been closely focused on banks' CRE lending in several ways: how banks are measuring their risk and monitoring the risk, what steps they have taken to mitigate the risk of losses on CRE loans, how they are reporting their risk to their directors and senior management, and whether they are provisioning appropriately and have sufficient capital to buffer against potential future CRE loan losses.

I suspect we are back to ‘old-school’ supervision where examiners are out reading loans. Examiners will ‘read’ loans and decide whether they warrant ‘criticism’ or ‘classification.’ The examiners 'rule-of-thumb for calculating the adequacy of the ACL applies weights to loans based on the degree of weakness (e.g. 20% for Substandard loans and 50% for 'Doubtful loans). For larger syndicated loans the rating will be derived on an inter-agency basis through the Shared National Credit (SNC) program. The SNC program is typically conducted in the spring, once year-end financial statements have been published. These results will only factor through into ACL builds during the 2nd and 3rd quarter.

When Your Own Head Office Is Your NPL

The Pfandbrief and its legal foundations provides a good overview if you’d like more detail.