Perspective on Risk - Dec. 2, 2024 (US Dollar)

Trump & the Dollar; The Death of the International Monetary Non-System; Further Triangulation; Bernanke Predicted This;

My mind went in a very interesting direction this weekend; totally unexpected. Sorry for another lengthy thoughtful post so quickly following Global Trends; I’m really trying to ration these things to weekly posts. This is for Terry C and the folks interested in the International Monetary Regime. In some ways it harkens all the way back to our discussion of Zoltan Poszar’s work.

Trump and the Dollar

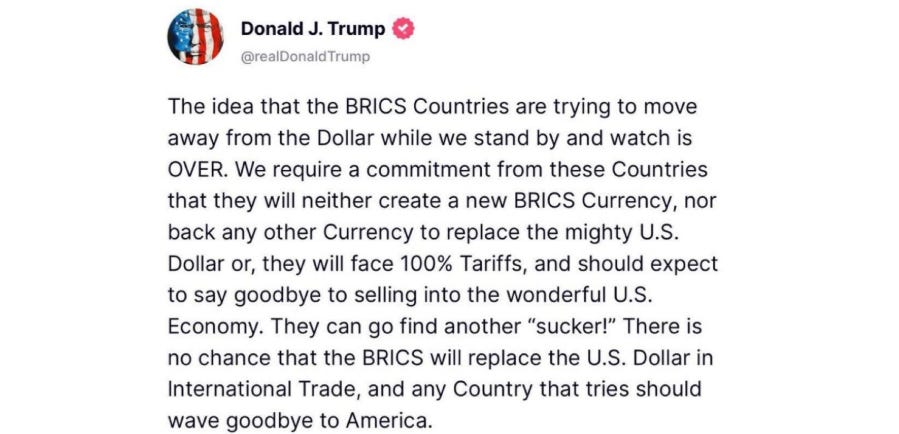

First, we have this post by our incoming President. It has caused a lot of chatter among the US economist community.

Krugman, Magnus, and Pettis all explain the fallacies in his understanding.

Krugman's analysis is particularly strong in explaining the network effects of dollar dominance through his English language analogy. Just as you can't force people to stop using English as a business lingua franca through threats, you can't maintain currency dominance through coercion. His breakdown of the dollar's three roles (medium of exchange, store of value, unit of account) and explanation of vehicle currency dynamics is textbook international finance theory.

Magnus makes a point that it is the "exorbitant privilege" of dollar dominance actually creates the trade deficits Trump ostensibly wants to eliminate. This is a crucial contradiction - you can't simultaneously maintain complete dollar dominance and eliminate trade deficits, as they're two sides of the same coin.

Pettis drives this point home most forcefully by highlighting the fundamental incompatibility between two stated goals: 1) Maintaining dollar supremacy, and 2) Reducing trade deficits and reviving domestic manufacturing

This is because, as Pettis notes, foreign accumulation of dollar assets (which underlies dollar dominance) necessarily requires U.S. trade deficits. You simply cannot have both.

The collective analysis reveals a deeper issue: the original post reflects not just misunderstanding of international finance, but internally contradictory policy goals. The proposed policy would be both ineffective (you can't threaten your way to currency dominance) and counterproductive (it would accelerate the very de-dollarization it aims to prevent).

This unrelated article Argentina Seeks Its First Wheat Shipments to China in Decades can be used to further illustrate the above points.

Just as Brazil benefited from the first trade war by increasing agricultural exports to China, Argentina is now positioning itself to capitalize on potential U.S.-China trade tensions. This demonstrates how protectionist policies often don't "protect" domestic industries but rather redirect trade flows to other countries

China's authorization of Argentine wheat and corn imports shows how markets adapt to trade barriers by developing new relationships. This suggests that unilateral tariffs often accelerate the very diversification of trade relationships they aim to prevent.

Argentina's potential entrance into China's wheat market shows how protectionist policies can actually reduce U.S. agricultural market share.

There's an interesting parallel between U.S. and Argentine trade policy challenges

While the U.S. threatens higher tariffs on imports, Argentina needs to reduce its export tariffs (12-33%) to become more competitive. Both cases show how tariffs can harm domestic competitiveness.

But In Defense of Trump

The world is changing rapidly.

As I’ve said before, China is “short water” - that is they do not have enough water to produce feedstocks to fully feed their population. As such they must import agricultural goods. In the now distant past, they imported a lot from the US (as a way to spend the dollars their manufacturing accumulated), but with the first Trump tariffs, they moved a substantial portion of their imports to Brazil, and now Argentina.

This could significantly change the currency dynamics over time. If China becomes the major trading partner for these countries, they will have a strong incentive to shift at least a portion of their reserves to Renminbi (RMB) or a BRICs currency if one developed. I’m in no way saying this is a sufficient condition to dethrone King Dollar, but it is a development in that direction.

Let’s do some prospective longer-term napkin math.

China's domestic consumption is approximately 55-56% of GDP, far below the 70-80% typical in developed economies. With China's GDP around $18 trillion, this puts domestic consumption at roughly $10 trillion. Import content of final consumption in China is estimated at around 10-15%, so approximately $1-1.5 trillion of consumption is imported goods.

If China moved to consumption levels similar to developed economies (say 70-75% of GDP). This would imply domestic consumption of $12.6-13.5 trillion at current GDP levels. With higher consumption shares, you'd expect import content to rise to perhaps 20-25%. This would suggest potential imports for consumption of $2.5-3.4 trillion.

Pettis has long been focused on this gap/transition. In some ways, it would be natural for some countries to diversify their reserve holdings (if it only weren’t for those pesky things like legal certainty of Chinese investments).

The Death of the International Monetary Non-System

So recently Russell Napier published a very interesting paper, America, China, and the Death of the International Monetary Non-System (American Affairs).

In keeping with our discussion last week of Global Trends, Napier's argues that in 1994, China made a decision that quietly changed the entire global economy. By keeping its currency artificially cheap and managing its exchange rate, China created an unofficial but powerful system that reshaped how money flows around the world. This system had huge effects: it kept interest rates unusually low in developed countries, encouraged companies to move manufacturing to China, and led U.S. companies to focus on financial engineering rather than building new factories at home. It also led to China accumulating massive amounts of U.S. government debt.

Now, Napier argues, this system is breaking down. China has taken on too much debt and needs to focus on its domestic economy rather than maintaining its currency policy. When this system finally breaks, it will force major changes in how the global economy works. We're likely to see a split into two separate financial systems - one led by the U.S. and its allies, another by China. Countries will probably restrict how money can move across borders, and governments will take a much more active role in directing where investment goes. This will be a huge shift from the past few decades of free-flowing global capital and relatively hands-off government policy.

Trump's tweet demonstrates exactly what Napier identifies as a critical misunderstanding - treating currency relationships as primarily about trade rather than understanding the deep structural interdependencies of the "non-system." The threat of "100% tariffs" shows a failure to grasp that the dollar's role isn't maintained through force but through structural relationships Napier describes.

Napier's paper explains WHY Trump’s goals are contradictory - the very system that maintains dollar dominance created the conditions that moved manufacturing to China and generated persistent U.S. trade deficits.

While not explicitly stated, Napier suggests that the system is ALREADY breaking down due to internal contradictions due to conditions in China, not the US (China's debt problems, the need for domestic reflation) and that this is fundamentally incompatibility with continued exchange rate management. The real challenge isn't preventing BRICS from "moving away from the dollar" but in managing the transition as China's domestic needs force a restructuring of the global monetary system.

Further Triangulation

The United States’ Fiscal Policy in a Global Context (IMF Econofact)

The United States is heading for a serious fiscal problem that could shake the entire global financial system. While U.S. government debt has long been considered extremely safe due to America's unique position in global finance, this same privileged position has allowed the U.S. to run much larger deficits than other countries. Now, according to IMF analysis, U.S. government debt is on track to reach dangerously high levels - projected to exceed 135% of GDP by 2029, far above other advanced economies. This isn't just an American problem; when U.S. government borrowing costs rise, it drives up borrowing costs worldwide and can create significant financial market turbulence globally.

What makes this particularly challenging is that the U.S. seems unwilling to make the difficult political choices needed to address the problem. The IMF points out that while there are clear solutions - like raising taxes, cutting spending, or reforming entitlement programs - there's little political appetite for any of these changes. This creates a growing risk that what has long been considered the world's safest asset - U.S. government debt - could become a source of global financial instability.

So let’s look at this piece through the lens of the Trump tweet and Napier.

This article creates a fascinating triangulation that gets at the heart of the current global monetary-fiscal dilemma.

The IMF piece highlights what Napier identified as a key breaking point - the U.S. is simultaneously trying to:

Maintain dollar dominance (Trump's focus)

Run persistent large fiscal deficits (IMF's concern)

Reduce trade deficits (Trump's stated goal)

As both Napier and the IMF note, these goals are fundamentally incompatible. The "exorbitant privilege" that allows high U.S. deficits depends on the very global monetary system that Trump's trade policies would undermine.

The IMF projects U.S. debt reaching 135% of GDP by decade's end, while noting this isn't necessarily catastrophic due to dollar dominance. However, Napier's analysis suggests this "non-system" enabling such debt levels is itself breaking down. Trump's aggressive trade policies could accelerate this breakdown.

So we have a new trilemma: an impossible trinity:

High fiscal deficits

Dollar dominance

Trade protectionism

You can maintain any two, but not all three. Trump's tweet suggests wanting all three, while Napier argues the system enabling any two is breaking down, and the IMF warns about the fiscal trajectory's sustainability.

This suggests several possible outcomes:

Forced fiscal adjustment (IMF's preference)

Breakdown of dollar dominance (Napier's prediction)

Abandonment of protectionist policies (unlikely politically)

Bernanke Pretty Much Predicted This in 2016

Ben Bernanke wrote an article for Brookings back in 2016: China’s trilemma—and a possible solution.

Bernanke identified China's impossible trinity:

Fixed exchange rate

Independent monetary policy

Free capital flows

This exactly predicts the situation Napier describes as breaking down in 2024. China tried to maintain all three but, as Bernanke warned, couldn't sustain this balance indefinitely.

Bernanke noted in 2016 that Chinese savers were "spurning yuan-denominated investments and looking abroad for higher returns." This is precisely what Napier identifies as a key breaking point - the capital outflows that forced China to burn through $700 billion in reserves.

Bernanke outlined three potential solutions: a) Large one-time devaluation (rejected as too disruptive) b) Capital controls (noted as potentially ineffective) c) Targeted fiscal policy to support transition. What's fascinating is that China attempted parts of all three.

The article helps explain why China's current predicament was somewhat inevitable - they never fully committed to any of Bernanke's proposed solutions, instead trying to maintain all elements of the trilemma until, as Napier describes, the contradictions became too great.

Unfortunately, one of Bernanke's suggested solution - using fiscal policy to build a social safety net to reduce precautionary saving - is particularly interesting in light of Napier's analysis of why the current system is breaking down. It could have provided a way to reduce the saving-investment imbalances that Napier identifies as core to the problem.