Perspective on Risk - Dec. 15, 2022

Blackrock’s 2023 Outlook; The Largest Private Pension Bailout; Wirecard; Commercial Real Estate; Leveraged Loans; More Housing; Regulators; Productivity; More Technology; More

Blackrock’s 2023 Outlook

Worth a read.

The Great Moderation, the four-decade period of largely stable activity and inflation, is behind us. The new regime of greater macro and market volatility is playing out. A recession is foretold; central banks are on course to overtighten policy as they seek to tame inflation. This keeps us tactically underweight developed market (DM) equities. We expect to turn more positive on risk assets at some point in 2023 – but we are not there yet. And when we get there, we don’t see the sustained bull marketsof the past. That’s why a new investment playbook is needed.

A key feature of the new regime, we believe, is that we are in a world shaped by supply that involves brutal trade-offs. (BP: echoes of Zoltan’s commodity =driver thesis)

The Largest Private Pension Bailout in History

Amazing how little attention this received.

Central States Teamsters Pension Fund Becomes the Largest SFA Rescue (Plan Sponsor)

The multiemployer plan will receive $35.8 billion in assistance, making it the largest bailout under the Special Financial Assistance program administered by the PBGC.

The Central States Plan is a multiemployer plan with 357,056 participants, mostly for Teamsters union employees and retirees, in various industries such as transportation, construction, and food processing.

From the Chicago Tribune:

Before Thursday, the program had awarded aid to 36 troubled pension plans, but none of those had received more than about $1.2 billion.

Without the federal assistance, Teamsters members could have seen their benefits reduced by an average of 60% starting within a couple of years.

The retirement plan has participants in almost every state, with the largest concentration in the Midwest. There are about 40,000 participants in both Michigan and Ohio, nearly 28,000 in Missouri, 25,000 in Illinois and about 22,000 each in Texas and Wisconsin

If you go to the Central States Pension Fund website you are told that the plan was formed in 1955 and since that date, it has paid $80 billion in benefits.

How did we get here?

A 2017 Report, MULTIEMPLOYER PENSION PLANS: CURRENT STATUS AND FUTURE TRENDS, by the Center for Retirement Research at Boston College. gives us some background.

Deregulation of trucking in the 1980s and the economic and financial crises since 2001 forced many major trucking companies out of business. Of the 50 largest contributing employers that participated in 1980, almost all are out of business and only 3 contribute today.

Large negative cash flow rates are a serious problem for two well-known plans facing insolvency: the Central States Teamsters and the United Mine Workers (see Table 7). In each case, cash flow is at or below -13 percent. That means they are digging into assets each year to pay benefits and are projected to exhaust their assets within the next 10 years.

The Central States Teamsters plan provides a good example of the fragility of some major contributors. Three companies in the plan that contribute more than 5 percent – ABF Freight System Inc., Jack Cooper Transport Company Inc., and YRC Inc. – have very low profit margins, and their debt is classified either as junk or slightly above (see Table 12). These employers may not be in a position to pay higher PBGC premiums.

In short, any increase in employer PBGC premiums – without offsetting steps to alleviate financial pressures – would have to be carefully tailored to avoid accelerating the death spiral of “critical and declining” plans …

More Pensions

Wirecard

If you’re an American like me, you likely have heard the name Wirecard, and you may even remember that they failed, but it probably doesn’t register with you as a huge fraud like it would if you were German or in London.

Netflix has an excellent documentary detailing the fraud. I HIGHLY recommend watching it.

Wirecard was a German financial services company that provided payment processing and other services. The company was founded in 1999 and quickly grew to become one of the leading providers of digital payment solutions in Europe. However, in June 2020, the company filed for insolvency after it was revealed that around 1.9 billion euros ($2.1 billion) in cash was missing from its balance sheets. The scandal, which has been described as one of the biggest accounting frauds in history, led to the resignation of Wirecard's CEO, Markus Braun, and several other executives.

But the story is much wilder. We’re talking shell corporations, Libyan and Russian agents, money laundering, regulators defending Wirecard against the FT, Wirecard trying to buy Deutsche Bank, etc. Some totally outrageous stuff here too: the BaFin defending Wirecard against the allegations by the FT; the Bundestag stamping secret a report by E&Y's on Wirecard.

A private investigator, Zatarra, working for the shorts, first accused Wirecard of laundering money through a shell corporation. You can read the Zatarra report here. Dan McCrum, along with Stefania Palma, Olaf Storbeck and John Reed, of the FT began reporting on Wirecard in 2015. Here is a link to many of their stories.

Watch Skandal - Bringing Down Wirecard on Netflix.

Wirecard is now on trial in Germany.

Commercial Real Estate

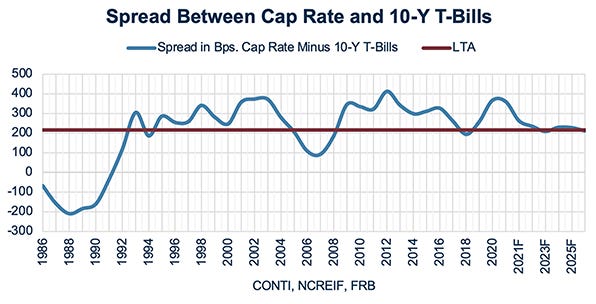

In discussing the current downturn, I have frequently said that I expect to see a commercial real estate downturn like we saw in the late 80s and early 90s. I’m not sure if there are the concentrations that there were back then, but the environment, particularly tough for old class A and class B CBD office properties. Cap rates of4.5-5.0% are too low in an environment with 2 year UST at 4.33% and 10 year Treasuries at 3.5-4.0%. The long-term cap rate spread to 10 year UST is generally thought to be north of 2%.1

Risk-free rates are not the only factors that drive cap rates, but many of the other factors, such as GDP, unemployment, Baa corporate spreads and rent growth all have their own challenges.

Back on Nov. 13th I wrote that we are in the early stages of risk moving from markets to firms. In CRE we’ve started to see some of these developments at the REITs:

BREITing bad (FT Alphaville)

Blackstone’s giant property vehicle BREIT limited withdrawals

It seems that mainly Asian investors in BREIT have been yanking money out so aggressively that they hit the withdrawal limit (the vehicle is structured so that withdrawals happen in the form of BREIT buying back shares from exiting investors).

The $14.6bn Starwood Real Estate Income Trust has already announced similar investor withdrawal limits.

Per the amazing @Chvolk

"During 2021 the private REIT reportedly raised about 70% of all the equity capital raised by private REIT companies. Since its 2017 inception, the company has raised a staggering $59.9 billion, repurchasing approximately $7.3 billion of this amount through its stockholder liquidity program. As of June 30, the NAV was reported to be $68.3 billion... if BREIT were a public company, its reported value would have the company ranked fifth amongst all equity REITs in terms of equity market capitalization."

@philbak1

And since the appraisal schedule is typically annual, when there is an economic turn, the appraisal based NAVs are going to be slow to catch up to the new environment.

SL Green Cuts Its Dividend as the Manhattan Office Market Suffers From Long COVID (Motley Fool)

S.L. Green recently announced a 12.9% decrease in its dividend to $0.2708 per month. This works out to an annual dividend of $3.25 per share. It did this in order to meet its projections for 2023 funds available for distribution. This move will allow S.L. Green to repay $2.4 billion in debt next year and increase its liquidity to just shy of $1.6 billion.

Leveraged Loans

Pretty simply put, the banks are on the hook for quite a few deals that are eating up balance sheet.

From Bloomberg2:

With just three weeks left in 2022, leveraged finance bankers are scrambling to unload a $40 billion albatross: the risky buyout financings that they committed to when credit markets were booming but that their usual investors will no longer touch.

Funds including Elliott scooped up €1.5 billion ($1.58 billion) of debt that underpins the buyout of Unilever Plc’s tea business at 82 cents on the euro. Apollo and Franklin got their hands on $750 million of Citrix buyout debt for 87 cents on the dollar. The banks financing gaming company 888’s takeover of William Hill International stuffed £347 million of debt through every channel they could, also at steep discounts.

IFR reports that banks are offering leverage to investors willing to take on the debt. The Independent reports that Morgan Stanley has already proposed replacing the high-rate unsecured Twitter debt with margin loans backed by Musk’s Tesla stake.

{T]he Blackstone Private Credit Fund (BCRED) has reportedly told FT Alphaville that “it anticipates 5 per cent of its shares being redeemed” during the next quarterly tender window.

What about Blackstone’s $50bn credit fund? (FT Alphaville)

More Housing

Demand still > supply

Forecasting Real Estate Trends for 2023 with Rick Palacios Jr. (Top of Mind podcast)

[S]o when we roll it all up, we think, again, our view is and this is now a 7% mortgage rates and core assumption in here is that mortgage rates stay relatively, relatively close to about 6% through next year. So that’s a foundational assumption, we think that home prices nationally, will correct to late 2020 levels, by the time we get to 2024.

What Happens If Housing Prices Fall 20%? (A Wealth of Common Sense)

From April 2020 through June 2022, housing prices in the United States rose more than 41%. That was basically a decade’s worth of price gains in a little over two years. You simply cannot have that happen for the most important financial asset for the majority of U.S. households.

Homebuilders … typically make up something like 10-15% of the housing supply. Today it’s more like 30%. If it gets as high as 40-50%, those homebuilders are going to be the marginal seller making a market and setting prices.

Even if we do get a 20% woosh lower in housing prices, it’s not likely going to have the same impact as the housing crash in 2008. The credit profile of borrowers is far better now than it was back then

Regulators

PCAOB reports higher deficiency rates in public-company audits (Jim Hamilton’s World of Securities Regulation)

“Higher deficiency rates in 2021, coupled with the fact that the PCAOB is also seeing an increase in comment forms for 2022, are a warning signal that the audit profession needs to sharpen its focus on improving audit quality and protecting investors,” PCAOB Chair Erica Williams said in a release. The report, “Staff Update and Preview of 2021 Inspection Observations,” stated many identified auditing deficiencies have been recurring for years. However, a significant portion of the rise was driven by deficiencies related to critical audit matters (CAMs), particularly those with fewer than 100 public company audit clients.

OCC names unrealized losses as key risk for US banks, gives stress test guidance

In its Fall 2022 Semiannual Risk Perspective report, the agency named investment portfolio depreciation as a key risk for U.S. banks.

U.S. banks posted AOCI losses of $347.83 billion in the third quarter, bringing the total for the first nine months of the year to $771.39 billion, according to a recent analysis by S&P Global Market Intelligence.

I mean………

Productivity

Prime working age men have been leaving the workforce for 40 years; this paper explores why.

Wage Inequality and the Rise in Labor Force Exit: The Case of US Prime-Age Men (FRB-Boston)

Data indicate that more frequent labor force exit among men without a four-year college degree has been driving the decline in the US prime-age (25 to 54) men’s labor force participation rate over the last 40 years. At the same time, non-college men’s earnings measured as a share of the average earnings of all prime-age workers have fallen by more than 30 percent since 1980. In light of these parallel trends, this paper investigates whether prime-age noncollege men are more inclined to leave the labor force when their expected earnings fall relative to the earnings of other workers in their labor market.

More Technology

Fusion Energy

Laser fusion experiment extracts net energy from fuel (Nature)

Huge, if true, but we’ve been here before.

[A] team of researchers say they have, for the first time, extracted more energy from controlled nuclear fusion than was absorbed by the fuel to trigger it. … The latest feat … is still a way off from the much harder and long-sought goal of 'ignition', the break-even point beyond which a fusion reactor can generate more energy than is put in. Many other steps in the current experiments dissipate energy before it even reaches the nuclear fuel.

Here is the formal paper, Fuel gain exceeding unity in an inertially confined fusion implosion, which requires a subscription that I do not have.

Computer-Generated Computer Code

Competition-Level Code Generation with AlphaCode (arxiv)

AlphaCode performs roughly at the level of the median competitor" in coding contests by using a purely data-driven approach.

Algorithms, Correcting Biases (Cass Sunstein)

A good paper if, like me, you believe that the use of explicit algorithms (rather than ML-based LLMs), can be good practice and address behavioral biases.

[A]lgorithms can overcome the harmful effects of cognitive biases, which can have a strong hold on people whose job it is to avoid them and whose training and experience might be expected to allow them to do so.

[A]lgorithms can be designed so as to avoid racial (or other) discrimination

in its unlawful forms—and also raise hard questions about how to balance competing social values (Kleinberg et al. 2019).

More

AIG Financial Product is No More

AIG subsidiary files for Chapter 11 bankruptcy (Reuters)

If You’re Gonna Crime, Don’t Be So Damn Stupid

FTX’s inner circle had a secret chat group called ‘Wirefraud’ (Australian Financial Review)

Members of the inner circle of power at collapsed cryptocurrency exchange FTX formed a chat group called “Wirefraud” and were using it to send secret information about operations in the lead up to the company’s spectacular failure.

…FTX founders Sam Bankman-Fried and Zixiao “Gary” Wang, along with FTX engineer Nishad Singh and former Alameda Research chief executive Caroline Ellison, used a chat group on Signal in the hope that the information would remain hidden.

The ‘Kevin Bacon’ Rule Is Out Of Date.

Degrees of Separation in Social Networks (Proceedings of the International Symposium on Combinatorial Search)

This paper addresses the search problem of identifying the degree of separation between two users. Our optimal algorithm finds an average degree of separation of 3.43 between two random Twitter users, requiring an average of only 67 requests for information over the Internet to Twitter. A near-optimal solution of length 3.88 can be found by making an average of 13.3 requests.

ML & Asset Pricing

Empirical Asset Pricing via Machine Learning

We perform a comparative analysis of machine learning methods for the canonical problem of empirical asset pricing: measuring asset risk premiums. We demonstrate large economic gains to investors using machine learning forecasts, in some cases doubling the performance of leading regression-based strategies from the literature. We identify the best-performing methods (trees and neural networks) and trace their predictive gains to allowing nonlinear predictor interactions missed by other methods. All methods agree on the same set of dominant predictive signals, a set that includes variations on momentum, liquidity, and volatility.

Wisdom Doesn’t Come With Age

FTX

The CFTC Complaint (link downloads a pdf) is an absolute hoot.

“[t]he fact that we didn’t hedge as much as we should have alone cost more in EV [expected value] than all the money Alameda has ever made or ever will make”

https://carlosvaz.com/en/blog/cap-rates-and-10-year-treasury-bills/

Shedding the LBO Albatross (Bloomberg)