Perspective on Risk - April 5, 2024 (Bank To Banking)

Evolution of the Financial System; Moral Hazzard; Synthetic Risk Transfe; Bagehot vs Kindleberger; Resolution; Failure Due To IRR; View From Inside Treasury; Fed Haircuts; Kahneman; Variable Kitties

Evolution of the Financial System

Further evidence that the NY Fed is paying attention to the changing funding liquidity patterns presented by the increase in private non-bank lending. Buch and Goldberg have been looking at this for a few years now.

Liquidity Interlinkages and Complementarity

Global liquidity flows are largely channeled through banks and nonbank financial institutions. The common drivers of global liquidity flows include monetary policy in advanced economies and risk conditions. At the same time, the sensitivities of liquidity flows to changes in these drivers differ across institutions and have been evolving over time. Microprudential regulation of banks plays a role, influencing leverage and capitalization, changing sensitivities to shocks, and also driving risk migration from banks to nonbank financial institutions. Risk sensitivities and flightiness of global liquidity are now strongest in more leveraged nonbank financial institutions, raising challenges in stress episodes. Current policy initiatives target linkages across different types of financial institutions and associated risks. Meanwhile, significant gaps remain. This paper concludes by discussing policy options for addressing systemic risk in banks and nonbanks.

Unfortunately, they do not provide estimates of these differing sensitivities.

An important and ley observation comes in section 4.1:

Although the international reform agenda largely treats banks and non-banks as being distinct, the two sectors are closely interlinked. They are interlinked not only via balance sheet linkages and similar portfolios, but also because of complementarities when it comes to the provision of credit to the real economy.

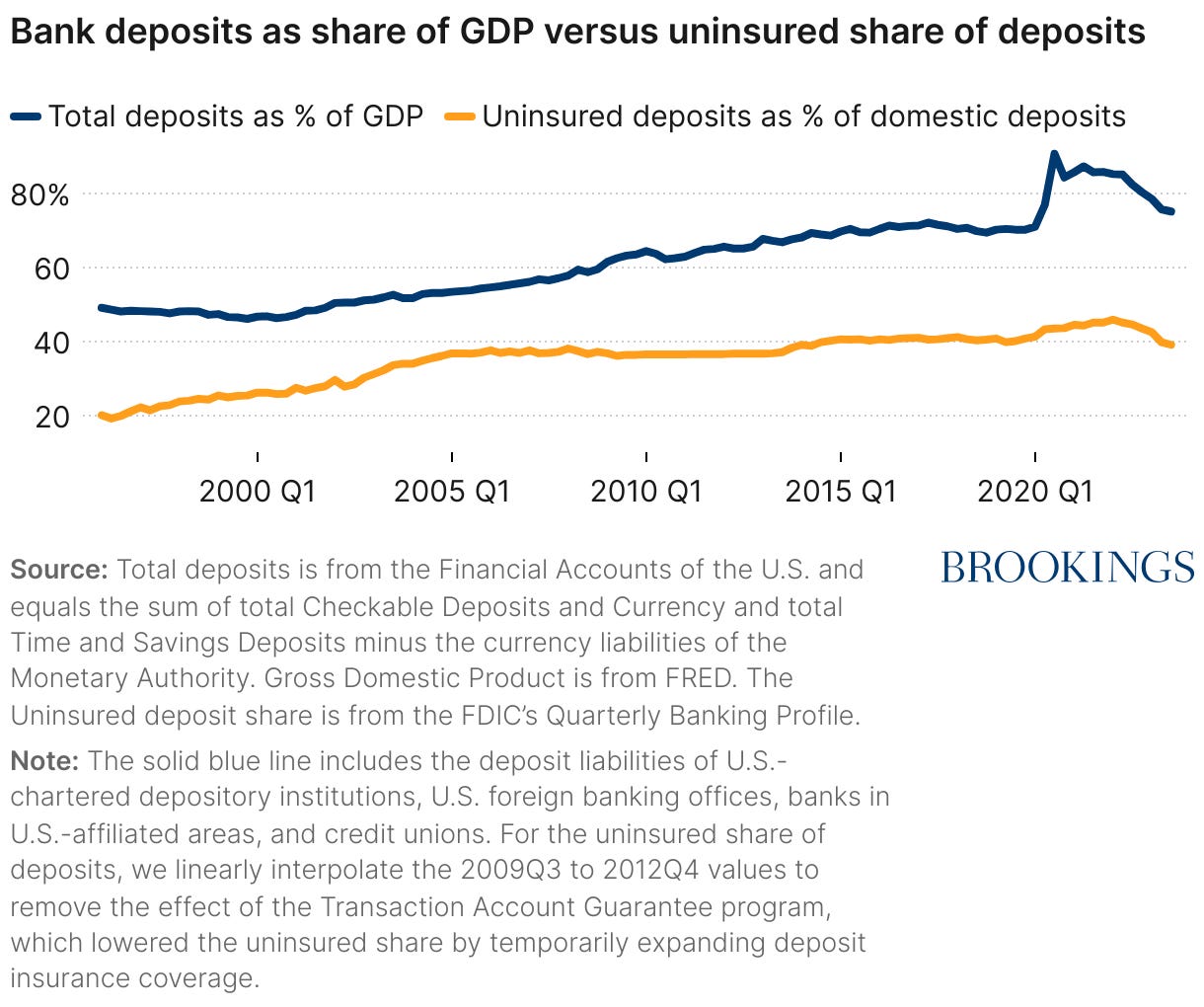

Banks Are Holding More (Uninsured) Deposits, But Have Lost Lending Share To Bonds and Private Non-Bank Lenders

A Brookings Conference The Evolution of Banking in the 21st Century: Evidence and Regulatory Implications discussed a similarly named paper by Hansen et. al. Sm Hansen has written some of my favorite papers over the last few decades, and he’s joined here by a number of heavy hitters.

One of the most striking developments that we document … is a dramatic growth in the economy-wide ratio of bank deposits to GDP [gross domestic product], with much of this growth coming from large uninsured deposits,” write Samuel G. Hanson, Victoria Ivashina, Laura Nicolae, Jeremy C. Stein, Adi Sunderam, and Daniel K. Tarullo, all from Harvard University.

Meanwhile, banks with the most rapid growth in deposits have seen the biggest declines in business lending, which has migrated toward non-bank entities such as securitization vehicles, mutual funds, insurance companies, and, in recent years, private-credit funds and business development companies.

PE sponsor engagement substitutes for bank monitoring

Banks are increasingly relying on sponsor strength, reputation and monitoring.

How Private Equity Fuels Non-Bank Lending (Fed Board)

We show how private equity (PE) buyouts fuel loan sales and non-bank participation in the U.S. syndicated loan market. Combining loan-level data from the Shared National Credit register with buyout deals from Pitchbook, we find that PE-backed loans feature lower bank monitoring, lower loan shares retained by the lead bank, and more loan sales to non-bank financial intermediaries. For PE-backed loans, the sponsor’s reputation and the strength of its relationship with the lead bank further reduce the lead bank’s retained share and monitoring. Our results suggest that PE sponsor engagement substitutes for bank monitoring, allowing banks to retain less skin-in-the game in the loans they originate and to sell greater loan shares to non-banks.

Scott Sumner on Moral Hazzard

In which he skewers Matt Levine and others.

The wrong way to think about moral hazard (Econlib)

You can’t judge moral hazard just by the outcomes

Things didn’t pan out for SVB. But that doesn’t mean their executives made an unwise gamble. It’s very possible that SVB’s strategy had a very high expected payoff, and they were simply hit by bad luck (rising interest rates.) Of course from a social perspective their decisions may have been bad, but not necessarily from a private perspective. “Heads I win, tails part of my losses are borne by taxpayers”. Of course I’d take more risk with those odds.

The fact that things didn’t work out for the executives doesn’t have any bearing on the question of whether moral hazard distorted decision-making at SVB.

The second misconception above [that moral hazard isn’t an issue because average people don’t think about the safety of a bank when making deposits] also illustrates a basic lack of understanding of moral hazard. Yes, people don’t tend to pay attention to bank balance sheets when making decisions on where to put their money. But that’s exactly what you’d expect to happen if moral hazard were a major problem. People would stop caring about bank risk, and highly risky banks would understand that they could attract deposits every bit as easily as conservative, well-run banks. Clueless depositors are not evidence of a lack of moral hazard; they are evidence that moral hazard exists.

Evidently Synthetic Risk Transfer Is Back

and the Bloomberg Editorial Board is not happy.

Banks’ New Trick Won’t Make Their Risks Disappear (Bloomberg)

One big reason the global financial system nearly collapsed in 2008 was that banks had shifted risks into the shadows, relying on insurance-like instruments that proved incapable of absorbing losses.

They’re at it again. It’s a trend that officials should discourage, not endorse.

By one estimate, the deals covered more than €43 billion in potential losses as of 2022. That’s mostly in Europe, though US banks have been ramping up their own risk-transfer deals.

Bagehot versus Kindleberger

Only for serious central bank nerds

Money and Finance Idea Lab Seminar Series: The Political

Columbia’s Center for Political Economy held an interesting seminar Money and Finance Idea Lab Seminar Series: The Political of Liquidity. Youtube has five videos of the sessions. Overall, it was mostly academics talking to academics.

Students of Bagehot and Kindleberger will be interested in Perry Mehrling’s discussion of emergency lending.1 Valérie Schwarzer argues that there are bigger differences between the two theorists, and that Kindleberger is more relevant for today.2

Resolution

Bagehot and Kindleberger naturally lead into bank resolution.

Whenever we face a wave of failures, academics and policymakers like to discuss everything they should have done differently or better.

European Case Studies

Yale looks at 19 case studies in Survey of Resolution and Restructuring in Europe: Pre- and Post-Survey of Resolution and Restructuring in Europe: Pre- and Post-BRRD (Yale)

… The main themes that emerge are: (a) the need for resolution and restructuring to eliminate uncertainty about an institution’s solvency by closing it, recapitalizing it, or merging it with a healthier institution; (b) the importance of effective valuation in achieving this result; (c) the necessity of clarity in the treatment of creditors; and (d) the value of a credible bail-in tool to incentivize creditors to agree to solutions outside of resolution.

Petrou Takes US Policymakers To Task (Again)

Karen Petrou: How the FDIC Fails and Why It Matters So Much (Petrou)

There’s a bit of a dance going on, all related to the “least cost” test that says the FDIC must take, in resolving a bank, the offer that results in the smallest loss to the Resolution Fund. Ms. Petrou, who I would expect to support large bank mergers (I may be wrong here, but that is my prior), takes shots at the FDIC’s inability to resolve a large bank as a way to cast aspersions on the working of the Ordinary Liquidation Authority (OLA) resolution mechanism, and therefore to take shots at the proposed merger guidance.

She writes (I reformatted for easier reading):

The most basic tenet of U.S. financial policy established in 1932, 1970, and – with teeth – in 2008 is that no financial company shall be too big to fail.

If markets believed this, market discipline would be credible.

If regulators could adhere to it, then the thousands of pages of unaccountable and often-incoherent resolution plans big banks now file would be boiled down to ensure far less complexity, greater operational and liquidity resilience, and sure and certain investor and large-counterparty cost.

If the FDIC knew what it was supposed to do and then knew how to do it, size thresholds for when banks are “too big” would be set not by the FDIC’s own pain point due to operational incompetence, but instead by differentiation between banks that may be too dominant regardless of asset size and those cut down to size only because the FDIC has made all but the smallest banks too big to fail by its failure to do its job as both an IDI and systemic resolution authority.

If the FDIC did its job and the Fed redefined emergency liquidity facilities and used its source-of-strength authority, financial companies – bank and nonbank – would no longer profit from moral hazard.

That’s what Congress demands, the FDIC and Fed are chartered to do, and a few good rules and a modern-day merger policy backed by effective supervision and enforcement would go a long way to ensure.

So I agree with most of these statements. Perhaps we should agree that the FDIC’s OLA should be modified so that, at a minimum, no systemically important financial institution (SIFI) should be allowed to purchase from the FDIC. This would not prevent new firm’s from becoming a SIFI, but it would be an incremental start.3

IMF Points Out The Obvious (Size Matters)

More Work is Needed to Make Big Banks Resolvable (IMF)

This piece is a reflection on Credit Suisse and the US regional bank ‘crisis.’

Taxpayers were once again on the hook as extensive public support was used to protect more than just the insured depositors of failed banks. Amid a massive creditor run, the Credit Suisse acquisition was backed by a government guarantee and liquidity nearly equal to a quarter of Swiss economic output.

Nothing new here. Just makes the point that at some size and significance, banks are just extensions of the sovereign and will need support. The size of UBS and CS relative to the size of the Swiss economy was a well-known issue.

Bank of England Finalizes Rules For Non-Systemic Banks

PS5/24 – Solvent exit planning for non-systemic banks and building societies (Bank of England)

The Bank has finalized its guidance requiring smaller non-systemic banks to submit Resolution Plans by Oct. 2025. More work for consultants.

Failure Due To Interest Rate Risk

The Failure of the Bank of the Commonwealth: An Early Example of Interest Rate Risk (FRB-Cleveland)

Commonwealth was perhaps the first bank to fail because of interest rate risk. The Cleveland Fed does a nice job of providing the details of the failure, and they conclude by contrasting Commonwealth with the recent SVB failure.

Silicon Valley Bank got into trouble for the same reason Bank of the Commonwealth did. It bought large quantities of long-duration, fixed-rate securities in a period of low interest rates and low inflation, and then both rates and inflation increased.

A second similarity was that both banks had unstable funding bases. For SVB, the unstable funding came from its uninsured deposits, which were 94 percent of its domestic deposits at the end of 2022.14

A third similarity was that SVB’s uninsured depositors ended up being protected by financial regulators, just like Commonwealth’s, albeit by different means. Since the Great Depression, uninsured depositors of a failing large bank have rarely lost their funds (Horvitz, 1986; Stern and Feldman, 2009), and despite the many changes to banking law since Commonwealth’s failure, the outcome for uninsured depositors at these two banks was the same.

One difference between the two banks was the degree and speed of the withdrawals and how that affected the failing bank’s resolution.

Historically, most banks have enough insured and stable deposits that a combination of discount window lending and other sources of lending can keep a bank operating until a solution is found. This was the case with Commonwealth and for the other too-big-to-fail bailouts of the 1970s and 1980s … As a result, Commonwealth’s run played out over time and gave regulators more time to resolve it.

In contrast, most of SVB’s deposits were uninsured and, as is well-documented, many were held by a small number of depositors who were highly connected to each other and could quickly initiate withdrawals (Board of Governors, 2023). As a result, the speed and size of the run on SVB was so fast and so large that there was not time to borrow from the discount window, let alone to find a buyer. Instead, regulators shut it down and used the systemic risk exception contained in the Federal Deposit Insurance Corporation Improvement Act of 1991 to protect uninsured depositors.

Instead, the resolution of Commonwealth looks more like that of First Republic, at least in the sense that there was more time to find an acquiring bank.

The Regional Bank Failures From Inside Treasury

Where you stand depends on where you sit.

Graham Steele, the former Assistant Secretary for Financial Institutions, penned Remember the Silicon Valley Bank Disaster? (Washington Monthly). It is largely a policy advocacy piece, but it’s always interesting to see how things were perceived.

One year ago, I was sitting in my office at the Treasury Department, where I served as a member of the department’s leadership overseeing our nation’s banking industry when we got word from our colleagues at the banking agencies that a large bank was facing imminent failure.

For two months last spring, we experienced the second, third, and fourth largest bank failures by assets in U.S. history. During this period, my Treasury colleagues and I received reports of long lines of depositors, steady withdrawals, and declining stock prices at banks nationwide. Panicked bankers and members of Congress were calling our offices, imploring us to put the full force of the federal government behind the nation’s banking system to ensure that we did not experience a widespread, Great Depression-style bank run that could push our economy into a recession.

Last February, I debated a former Trump administration regulator who argued that the failure of large regional banks like SVB, Signature, or First Republic posed little risk to financial stability. Less than a month later, this view was proven to be spectacularly misguided.

Not sure I agree with this. I’d note that the Fed still hasn’t responded to my FOIA request from last AUGUST.

Fed Charges Some Pretty Steep Haircuts

Obligatory Steven Kelly Reference

Danny Kahneman

The Nobel Prize-Winning Professor Who Liked to Collaborate With His Adversaries (Cass Sunstein in the NYT)

List of Danny Kahneman’s Papers on Google Scholar

High & Low Variance Kitty Cats

Mehrling’s main Point: Emergency liquidity provision is not fundamentally different from everyday liquidity provision. We do not need a special theory for the lender of last resort; the correct theory for "peacetime" also applies to crisis situations. This contrasts with the standard economic view, which often treats emergency liquidity provision as an exceptional event requiring a separate theoretical framework.

Schwarzer sees a deeper analytical difference between Bagehot and Kindleberger than Mehrling does. Bagehot emphasizes lending at a high rate of interest against good collateral to deter opportunistic behavior and protect the central bank's reserves. This reflects a belief in a finite and inelastic supply of liquidity. Kindleberger prioritizes providing maximum elasticity of liquidity supply to contain panics and prevent fire sales of assets. He recognizes the endogeneity of solvency and the limitations of relying on good collateral during a crisis.

Schwarzer cautions against relying solely on central banks for emergency liquidity management, as this can lead to "financial dominance" where central banks are forced to cater to the interests of financial markets. She argues that fiscal authorities should play a larger role due to their democratic legitimacy and ability to address the Bagehot dilemma by attaching strings to guarantees and levying fees for bailouts.

It might be time prohibitive to have the regulators make a determination that the new entity would be a SIFI.