10/16/2021

Where have we been? Where are we going? Risks

I like to step back every now and then and think about time scales longer than our daily concerns.

Where Have We Been

The long-term demographic and technology trends continue to play out.

Demographically, Japan and Europe age rapidly, the US ages a bit more slowly, China, which will age very rapidly, passes its optimal number of workers to dependents, and India1 and sub-Saharan Africa grow rapidly.

Technology-wise, Moore’s law has continued to hold, and other technologies, such as gene sequencing or the cost of solar power are progressing exponentially faster than Moore’s law for semiconductor circuits. The iPhone, Google Maps, Facebook, Bluetooth, CRISPR gene editing, electric cars, self-driving cars, and 3d printing didn’t exist 20 years ago. Neither did reusable rockets. China hadn’t yet been admitted to the WTO.

What we used to call the world of H3 (the third horizon) is almost upon us. All of these are dis- or de-flationary. However, they also contribute to ‘globalization’ which is in moderate retreat as the 20 year experiment of US-China economic integration comes apart. Ideally, the labor arbitrage would move to other rapidly growing countries like India, but we are clearly seeing frictions in any adjustment away from China.

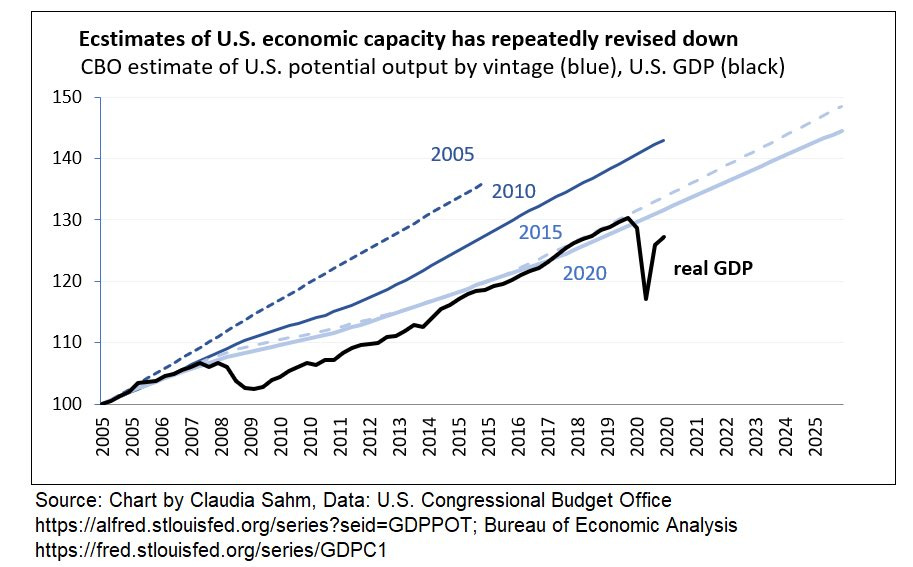

The developed world has faced a number of horrible shocks. Following the implosion of the dot-com boom in 2000, we had 9-11, the Global Financial Crisis, and the Covid downturn. This graph gives some idea of what’s been lost: $10-20 trillion of annualized output/GDP.

As Adam Toose notes:

Interest rates are at 5000-year lows. But the norm for long-term rates is closer to 3% than it is to 6%.

We are in pretty severe ‘financial repression.’

And as inflation expectations are rising faster than nominal yields, at least in the short term it is only poised to continue or get worse. As Doug Dachille put it, get used to a world of return-free risk

So Where Do We Go From Here?

With the long-term trends in mind, probably the defining medium-term development will be central banks beginning to pull away the extraordinary support they have given to economies. The Fed will soon consider, and is expected to approve, the unwind of quantitative easing. From the FOMC minutes (highlighting is mine):

Participants also expressed their views on how slowing in the pace of purchases might proceed. In particular, participants commented on an illustrative path, developed by the staff and reflecting participants' discussions at the Committee's July meeting, that gave the speed and composition associated with a tapering of asset purchases. The illustrative tapering path was designed to be simple to communicate and entailed a gradual reduction in the pace of net asset purchases that, if begun later this year, would lead the Federal Reserve to end purchases around the middle of next year. The path featured monthly reductions in the pace of asset purchases, by $10 billion in the case of Treasury securities and $5 billion in the case of agency mortgage-backed securities (MBS). Participants generally commented that the illustrative path provided a straightforward and appropriate template that policymakers might follow, and a couple of participants observed that giving advance notice to the general public of a plan along these lines may reduce the risk of an adverse market reaction to a moderation in asset purchases.

Anthony Sauders notes that the Bank of Japan’s balance sheet has stopped growing and its holdings of government bonds have started to decline. The ECB seems a bit further behind the curve, as they are considering continuing their quantitative easing ($) once its Pandemic Bond Buying Program ends.

If we think about things in terms of yield curve decomposition, the retreat of QE should result in higher risk/term premium. We also know that implied forward inflation has risen, and the Fed has indicated that it will not be raising the overnight rate any time soon (and the futures market seems to concur).

Now the pace of the unwind of QE looks relatively slow. The Fed will be selling less than 1% of the agency MBS market per month. The Fed owns about 25-30% of the agency market, so unless they pick up the pace we are looking at 2+ years of unwind.

Looking at a yield curve decomposition breaking out the effects of Rf, implied breakeven inflation and the term/risk premium, it’s illustrative to remember that the Fed kept the Fed Funds rate at virtually zero for a full 6 years following the global financial crisis. TIPs yields were negative for ~5 years. Risk premia narrowed only once financial repression ended. The Fed has been willing to be more repressive so far, and steepening the curve will only increase the amount of repression in the short term.

Interestingly, though, the market has begun to build in a more rapid rise in the Fed Funds rate:

So all else equal we are facing:

long-term deflationary effects of demographics and technology, and

medium-term pressures to steepen the yield curve (inflation expectations and risk premia). And as term rates rise we may see additional convexity hedging (not to mention that the Fed by curtailing MBS purchases will be adding negative convexity back to the market).

Risks

Again thinking through the medium-term prospects, what are the risks?

The first risk is that I have no idea what I am talking about (probability 75%).

Second, as with Japan at the peak of their bubble, the stock market values growth over value. Who needs firms that generate cashflow when cash is abundant and term discount rates are negligible. An increase in the term premia should at least put a little headwinds to growth stocks (I have no idea what level is needed to really change the economics). More broadly, BofA likens the S&P 500 to a 36-year zero ($).

Third, the US and developed market economies remain very vulnerable to an exogenous shock. With the covid-crisis, the Fed has already had to deploy many ‘weapons’ that it hadn’t used before - bought corporate bonds, bought new-issue municipal bonds, created additional facilities to handle institutional MMF (as the last set of policy changes haven’t yet solved the problems), and bought 1/3rd of the MBS market. What will they have to do if hit with an exogenous shock in the next 6 months?

Finally, who will be buying the assets that the Fed is selling? Unless the Fed changes its capital requirements (unlikely), the banking sector is capital constrained. It is possible that the securities could get pledged to the Fed’s standing repo facility. At higher yields, the securities may be interesting to foreign buyers. Finally, there’s the possible expansion of holdings by unregulated non-bank financial institutions; this seems likely if a steeper yield curve makes carry more attractive.

Errata

What I’m listening to: The Old North Woods (Bella Fleck)

And if anyone is looking for a wizard with experience, Ian is available, experienced and relatively cheap.