10/10/2021

Tether is a MMMF; Do we care? Policy implications

OK, I’m writing way to many of these; I promise to slow down

Tether is a MMMF

I’m not particularly deep on crypto, but it does fascinate me. In particular, the development of so-called ‘stable coins’ and the possibility of a central bank digital currency (CBDC).

Tether, in particular, has attracted a lot of attention. In its FAQs, Tether states:

Tether tokens hold their value at 1:1 to the underlying assets.

and

All Tether tokens are pegged at 1-to-1 with a matching fiat currency (e.g., 1 USD₮ = 1 USD) and are backed 100% by Tether’s reserves.

Cute, huh.

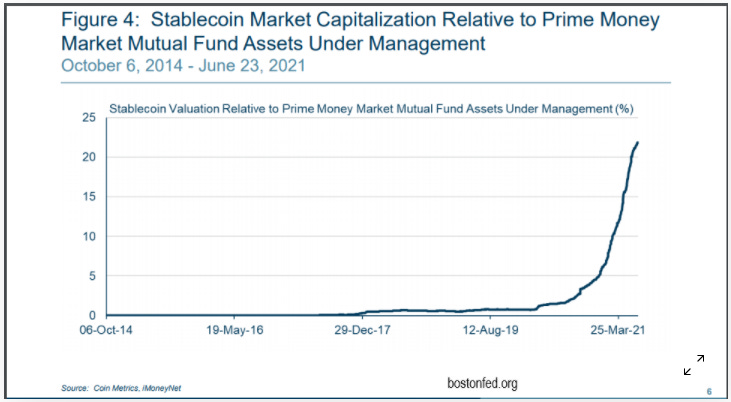

Tether has total assets of $68 billion. For reference, if they were a bank it would put them around #40-50. For another point of reference, the size of the Prime money-fund industry is $469 billion. As a third point of interest, at $68 billion Tether represents about 2/3rds of the total $100 billion stable coin market.

Tether has repeatedly made claims about the size and nature of its reserves; initially they were incredibly opaque, now just regular, old opaque. The nature of the reserves is important, because as with MMMF, they claim they will honor all obligations at par on demand. Tether publishes an Independent Accountants Report that provides some details on its holdings.

In the latest bit of disclosure, in response to a Bloomberg article ($), Tether stated that they do not hold the commercial paper of Evergrande, the struggling, likely insolvent, Chinese property developer.

“Tether does not hold any commercial paper or other debt or securities issued by Evergrande and has never done so. As we have indicated in our published statements and our most recent assurance attestation with a reporting date of June 30, 2021, the vast majority of the commercial paper held by Tether is in A-2 and above rated issuers.”

According to Tether, about 50% of its reserves - some $20 billion - were in commercial paper at the end of March, 12% in secured loans and 10 percent in corporate bonds, funds and precious metals. Only 2.9% was in dollar cash. Of the CP, only $14.7 billion was rated A1 or better. In addition, $13.7 billion has a 181-365 day maturity.

The average duration of items in this category is 150 days and the average rating is A-2.

Importantly:

Management’s accounting policy is to value assets and liabilities at historic cost plus any accrued interest and less any expected credit losses, or otherwise the redemption value where applicable. The realisable value of these assets and liabilities could be materially different if any key custodian or counterparty incurs credit losses or substantial illiquidity.

One issue is that the traditional CP dealers have stated that they do not recognize Tether as a buyer in that size. This leads to informed speculation that much of the CP owned by Tether is from Chinese companies.

Many crypto firms have established custody relationships with banks, and several have off-shore licenses (frequently Bermuda)

OK, so now that I’ve given you the background, so what?

Do we care? And if so why?

The first, most immediate question is whether Tether represents a transmission channel for systemic risk. Institutional MMMF have had a bad habit of facing preemptive withdrawals (runs) when risk increases as institutions want to insure their cash is safe. Recognizing this, the US Government has introduced rules governing the MMMF industry that provides clarity for investors. But as the covid-related events of 2020 show, there is still incentive for investors to run. These rules do not apply to Tether. Neither does Tether have direct access to the Federal Reserve’s discount window nor are its accounts covered by FDIC deposit insurance.

So the direct risk from Tether to the financial systems seems low. The issue becomes whether there are indirect linkages. 2008 surprised us by the size of the ‘liquidity puts’ that the banking sector had provided to the SIVs and ABCP conduits; this brought the risk onto the bank balance sheets. I have no reason to believe that US banks have engaged in this activity, but would be less confident that there isn’t some bank out there doing something stupid.

A second risk would be if corporations were keeping their cash deposits in crypto rather than the traditional financial system. There have been a number of firms that have made significant crypto investments, but it appears that they are not using crypto to manage their working capital, and a strong argument can be made for caveat emptor as long as there is disclosure and transparency.

Policy Implications

So crypto is becoming an asset class (whether some of us find little to no socially-redeeming value). Square, Paypal and others are creating digital wallets and allowing their customers to transact and transfer crypto. Our kids, and maybe some of you, are already transacting.

Should stablecoins have access to the financial system, and if so how? The Federal Deposit Insurance Corp. (FDIC) is studying whether certain stablecoins might be eligible for its coverage. Circle, another stablecoin issuer, disclosed they are under SEC investigation. The Fed is said to be studying whether the US needs to issue a CBDC.

My favorite paper for thinking through these issues is an old paper written by Gerry Corrigan when he was the President of the Minneapolis Fed titled “Are Banks Special?” way back in 1982.1

Amidst this process of rapid change, with market innovation and new sources of competition, there is a perception that banks' competitive position—and presumably their market share—has slipped. Casual observation of 2 the growth of the commercial paper market, the thrift industry money market mutual funds (MMMFs), and the de facto trend toward ownership of banks by securities firms and commercial enterprises, tends to support that perception. Indeed, there are numerous instances in which nonbanks have been able to provide "bank-like" services at a lower cost (or a higher rate of return) to the individual or corporate customer, thereby drawing business away from banking institutions.

In reviewing the development of MMMF he concludes:

A case can be made that nonbank financial institutions incur liabilities that appear to have some or all of the characteristics of a transaction account issued by a bank. However on close inspection it appears that such instruments whether—MMMFs, retail repurchase (RPs) agreements, customer credit balances with brokers, sweep accounts, etc.—do not, at least in a technical sense, in fact possess the characteristics associated with the bank issued transaction account

In a prescient statement applicable to stablecoins (highlighting is mine):

In all of these cases, including money market mutual funds, instruments which appear to have bank transaction account characteristics take on those characteristics in part because the acquisition or disposition of such assets involves, at some point, the use of a transaction account at a bank. However, technology makes it possible to manage these financial assets in a way in which their ultimate dependence on a bank account is not apparent to the individual holder of the asset.

So crypto right now is not the equivalent of a bank demand-deposit account because ultimately, behind the technology, there is a separate dependence on a bank DDA.

The problem for Tether (and other stablecoin issuers) is how to get a linkage from crypto → stablecoin → demand deposits.

Tether could invest its assets in a Government MMMF, but that would be uneconomical. Also, settlement is not instantaneous.

Tether could invest in a Prime MMF, but then they could not guarantee the 1-to-1 conversion into dollars. Also, settlement is not instantaneous.

Tether could become a bank. This would provide access to the Fed’s discount window and could have stablecoins treated as DDA. This however would come with higher capital requirements (both risk-based and leverage), explicit reserve requirements, and supervisory oversight. At current capital requirements, I have no idea whether the economics work.

There is one additional alternative, but one that the Fed appears to have rejected (for now) in 2019. That is the concept of a ‘narrow bank.’ A narrow bank would have a narrowly focused business model that involve taking deposits from institutional investors and investing all or substantially all of the proceeds in balances at Reserve Banks. These narrowly focused depository institutions would not be subject to federal prudential regulation and would not be subject to the same set of capital and other prudential requirements as other federally regulated banks. In effect, these narrow banks would pass through the interest obtained at the IOER rate from a Reserve Bank to their depositors, less a small spread.

John Cochrane summarized it well:

If anyone should worry about narrow banks it is money market funds, especially those that hold only treasuries.

Treasures -> Fed -> reserves -> narrow bank -> consumer

is better than

Treasuries -> money market fund -> consumer.

Add stablecoin before ‘consumer.’

So back to Corrigan - how do stablecoins fit into his analysis? He concludes that three factors make banks special:

Banks offer transaction accounts.

Banks are the backup source of liquidity for all other institutions.

Banks are the transmission belt for monetary policy.

Tether and the other stablecoin issuers are claiming to issue transaction accounts. But lacking access to the ‘inside money’ of the banking system, Tether does not meet criteria #2 and #3. By attempting to solve the convertibility issue they are on path to solving #2. If crypto gets widely adopted for transactions, the Fed will be forced to address #3 as it could eventually, sometime, maybe become the defacto method of transacting.

I’ll close with another quote from the conclusion of the prescient paper:

A strong case can be made that banks continue to be special. And because they are special, we, as regulators, will continue to apply high standards to companies seeking a bank charter. We must also continue to examine and supervise banks for safety and soundness. Likewise, it appears that Congress will take a cautious approach when determining what types of companies may own and affiliate with banks.

But banks must also compete in the marketplace. Consequently, we can expect over time to see adjustments in both the direct activities of banks and in the line separating banking and commerce. History is, in some sense, about the drawing, re-evaluation, and re-drawing of lines. As a matter of public policy, changes will trail rather than lead the marketplace, and any changes must be informed by a careful study of both the role we want banks to play in our economy and the needs of the marketplace.

And hey, if anyone is in contact with Jamie McAndrews, throw this his way, I’d love to hear his arguments.

What I’m listening to: Arooj Aftab - Full Performance (Live on KEXP)

What I’m reading: Red Roulette

The money-market mutual fund industry is divided into two pieces; Government, which per the title are backed by sovereign obligations, and Prime, which can be backed by a broader set of assets - typically including commercial paper.

There have been subsequent reference to this paper including “Are Banks Still Special” (Olson, 2006) and “Are Banks Special? A Re-Revisitation“ (H. Rodgin Cohen, 2017)