Perspective on Risk - Oct. 28, 2023

From Tropical Storm to CAT-5 in 12 Hours; Credit; Markets; Money Market Funds; Euroclear Makes Bank; Main Street Lending Facility Performance; Prayer-GPT; Asymmetries

From Tropical Storm to CAT-5 in 12 Hours

Scared yet? Still denying climate change?

Otis strengthened from a tropical storm into a major hurricane within only about 12 hours before it made landfall at 1:25 a.m. CDT, according to the hurricane center. The storm slammed into Mexico's coast with maximum sustained winds of 165 mph and hurricane-force winds extending up to 30 miles from its center.

"Otis has explosively intensified 95 kt [about 110 mph] during the past 24 hours, a mark only exceeded in modern times by Patricia in 2015," the hurricane center said in an advisory released late Tuesday night, as Otis grew quickly into a Category 5 storm. At the time, forecasters added, "There are no hurricanes on record even close to this intensity for this part of Mexico."

How Hurricane Otis defied forecasts and exploded into a massive storm (Vox)

For Otis, the “key ingredient” for intensification was warm water, with temperatures topping 86 degrees Fahrenheit, said Brian McNoldy, a hurricane researcher at the University of Miami

Hurricane Otis likely to trigger Mexico catastrophe bond payout (Artemis)

The tail risk of natural disasters is typically covered through reinsurance. But a small but growing fraction has been transferred to the capital markets through “CAT bonds.” Investors like these because they are uncorrelated to their equity and fixed income portfolios.

The Government of Mexico’s catastrophe bond is facing its most severe threat of the current Pacific tropical cyclone season, as hurricane Otis has rapidly intensified to a category 5 storm and its central pressure has deepened sufficiently to trigger the $125 million IBRD / FONDEN 2020 tranche of notes that are exposed.

CAT bonds come in three flavors: indemnity, industry loss, and parametric. The Chicago Fed has a primer Catastrophe Bonds: A Primer and Retrospective. This one is a parametric bond

The parametric trigger for the cat bond’s Pacific hurricane coverage is based on landfall location and minimum central pressure of any storm that approaches the Mexican coast. In order for the $125 million Class D Fonden 2020 cat bond notes to face any loss of principal at all, the minimum central pressure of hurricane Otis would need to fall to 935 mb or below. Hurricane Otis is reported to have had a minimum central pressure of 923 mb at landfall

At 923 mb, hurricane Otis is likely to trigger Mexico’s catastrophe bond and cause a 25% or even a 50% loss of the $125 million of exposed principal, it now appears.

Related Research

Will Global Warming Make Hurricane Forecasting More Difficult? (American Meteorological Assn.2017)

Hurricane track forecasts have improved steadily over the past few decades, yet forecasting hurricane intensity remains challenging. Of special concern are the rare instances of tropical cyclones that intensify rapidly just before landfall, catching forecasters and populations off guard, thereby risking large casualties. Here, we review two historical examples of such events and use scaling arguments and models to show that rapid intensification just before landfall is likely to become increasingly frequent and severe as the globe warms.

Credit

SLOOS is showing tightening conditions beginning to rival GFC. Marginal credits are having tougher time finding liquidity. Folks are playing tricks to refi deals, and smart money is raising for distressed debt.

Firms Beginning To Tap Credit Lines

Debt Collector Intrum Taps Banks After Funding Markets Sour

Swedish debt collector Intrum AB is tapping bank credit lines for funding as selling commercial paper becomes more challenging.

The company drew down on its revolving credit facility to cover funding gaps, according to a statement on Wednesday. It reported an 8.7% drop in its outstanding commercial paper, which currently stands at 760 million kronor ($68 million), citing poor sentiment in the credit market.

Distressed Firms Have a New Controversial Way to Get Rescue Cash

The move, known as a “double-dip,” helps struggling firms raise cash by issuing debt out of an empty subsidiary, having the parent company guarantee that debt, and sending the proceeds from the debt deal back to the parent company via an inter-company loan, which then becomes another form of collateral for the obligation.

Double-dips can improve creditors’ prospects for recovery in a default by giving them more or different claims on a company’s assets, the strategists wrote. The maneuver differs from transactions like priming — which pushes existing creditors back in line for repayment — by allowing the existing creditors to participate in the deal. And unlike drop-down financings, where a company moves assets out of reach of some creditors, no assets are transferred.

Private Credit

Matt Levine highlighted an article Private Credit Lenders Giving Up Protections to Win Bigger Deals.

“Private credit is dropping maintenance covenants in larger deals,” analysts including Derek Gluckman wrote in a Thursday report, referring to a type of investor protection that requires companies to periodically meet certain tests of financial health. Leveraged loans discarded the safeguards years ago and most are now considered ‘covenant-lite.’ Direct lenders are following suit, Moody’s says, noting that only 7% of private credit loans larger than $500 million in its analysis had maintenance covenants, compared to 67% of loans smaller than $250 million. …

The global $1.5 trillion private credit market has been known for more conservative deal terms … “Private credit loans are strikingly more protective than broadly-syndicated loans, but differences will narrow,” Moody’s wrote. “The ramparts between public and private lenders will come down as competitive pressures mount, just as the same protections eroded in the broadly-syndicated loan market over time.”

Levine concludes:

Right now, private credit lenders are much more likely than bond or bank loan investors to be relationship lenders, to get to know the company well, lend it money and hold the loan to maturity. But give that some time and it will change.

Chinese Real Estate & CDS

Country Garden’s Missed Bond Payment Triggers CDS Payout

The Credit Derivatives Determinations Committees, which oversee the credit default swaps market, ruled a failure-to-pay credit event occurred on Oct. 18, according to a notice posted Thursday. A meeting was held on Wednesday to deliberate on whether Country Garden missing a $15.4 million coupon payment triggered CDS payouts.

The bond’s trustee has deemed China’s former largest developer to be in default on a dollar note for the first time after Country Garden didn’t pay interest by the end of a grace period, Bloomberg News reported on Wednesday. The trustee told the bond’s holders that the delinquency “constitutes an event of default.”

Country Garden’s dollar notes are indicated at just 4 cents, according to prices compiled by Bloomberg

Markets

Emerging Markets

Lazard Is Taking an ‘Unusually Low’ Level of Risk in EM Bonds (Bloomberg)

The money manager, which oversaw more than $203 billion in assets as of mid-year, is turning away from high-yield bonds from developing markets in favor of investment-grade credits, according to a note. Debt from Argentina — where a presidential runoff is now in focus — is of particular concern

High-yielding bonds from Egypt, Kenya and Nigeria also stand out in terms of risk. By Lazard’s count, 33 of the 76 countries tracked by the firm have bonds trading at yields at or above 9.5% — high enough to effectively lock the nations out of bond markets.

Distressed Debt

Fortress Targets $8 Billion Fundraise for Credit Opportunities

Fortress Investment Group is targeting as much as $8 billion for its latest credit opportunities fund, which will invest in areas ranging from distressed debt to structured credit

Treasury Basis Trade

Not going to repeat everything I’ve written about here. Just noting:

Griffin Says Scrutiny of SEC Basis Trade ‘Utterly Beyond Me’ (Bloomberg)

“This [strategy that provides liquidity and improves Treasury market efficiently] is totally lost on Gary Gensler and totally lost on the Fed,” Griffin said during a conversation with fellow billionaire Paul Tudor Jones.

Gary Gensler said last week that

The funding that prime brokerages provide to some hedge funds on a “very generous basis” is the biggest source of risk in the financial system …

Interesting tidbit here; certainly hope this wasn’t the Fed’s motivation:

Jones, who runs hedge fund Tudor Investment Corp., said his firm’s basis trade portfolio “was in extreme duress” in March 2020 and that “the Fed’s entrance in the market bailed that particular book out.” While it didn’t affect the firm’s overall profit and loss, it “was a huge stress,” he said.

Asset-backed

Used-Car Dealer Halts Plans for Subprime Auto Loan Offering

Private equity-backed used-car dealer Byrider chose not to proceed with its latest subprime auto asset-backed security deal, a sign that investors may be growing reluctant to buy some lower-rated securitizations.

Texas-based lender Tricolor Holdings LLC postponed a $259 million offering earlier this month and Bridgecrest last week sold subordinate tranches of its notes outside of guided price talk, meaning the issuer had to pay up by offering a higher spread to get the deal done.

Money Market Funds

The issue around MMMFs (particularly institutional funds) is that investors have a first-mover advantage when the assets fall below par. Huge issue for financial stability.

Pandemic Revealed Unresolved Vulnerabilities (GAO)

In 2010 and 2014, the Securities and Exchange Commission (SEC) revised its money market mutual fund (MMF) rules after some MMFs experienced runs (heavy redemptions) during the 2007–2009 financial crisis.

Evidence indicates that SEC’s reforms did not prevent runs during the COVID-19 pandemic. For example, prime MMFs—which can invest in all types of short-term debt instruments—held by institutional investors experienced net redemptions of about 30 percent of their total assets in a 2-week period in March 2020 (see figure). Some evidence also indicates SEC’s reforms may have contributed to the runs. Some investors may have preemptively redeemed MMF shares to avoid incurring a liquidity fee or losing access to their funds under a redemption gate.

This is now showing up in revised prospectus.

The SEC revised their rules so that:

under certain circumstances … asset managers [are obliged] to charge a 200 basis point withdrawal fee.

The fund's board would have the sole power to make the call, if it determines the fee is in the fund's “best interest.” Yet should a fund's daily net redemptions top 5%, asset managers are obliged to levy the fee.

The new rule also increases the minimum liquid assets a non-government MMMF must hold:

The new SEC ruling increases the mandatory minimum of liquid assets a money market fund must hold free on any given day to 25%, up from 10%, and to 50% weekly, up from 30%.

I’m still not sure that this changes the incentives sufficiently. As I wrote back in May, Bagehot is out of date - the structure of the financial markets have changed. Central banks need to provide priced, ex-ante liquidity insurance. See Perspective on Risk - May, 19, 2023

Euroclear Makes Bank

Matt Levine crushed it with his Oct. 26 Money Stuff. So much good stuff in there. He taught me something new today:

Consider a Russian oligarch who invested some money in the bonds of a German company a few years ago, … [subsequently] was subjected to comprehensive sanctions by the European Union... His bonds are trapped at an EU brokerage and he can’t sell them. But then the bonds mature and the German company has to pay them back. … What happens? Who gets the money?

… the delightful actual answer is that Euroclear gets the money.

Here is Euroclear’s announcement of its financial results, which explains how this works. It’s not really that Euroclear gets to keep the money; it’s just that (1) Euroclear gets to hold the money until someone figures out what to do with it and (2) meanwhile, it gets to invest the money and keep any interest it earns.

A big topic when I was at the Fed was fiduciary reviews of escheatment at transfer agents. Practices there were quite sloppy. Hope Euroclear keeps better records.

Main Street Lending Facility Performance

…is not very good.

Tip of the hat to George Selgin for pointing us to Interim Report: Audit of the Effects the Main Street Lending Program’s Loan Losses Have on Treasury’s Investment in the Program from the Office of the Special Inspector General for Pandemic Recovery.

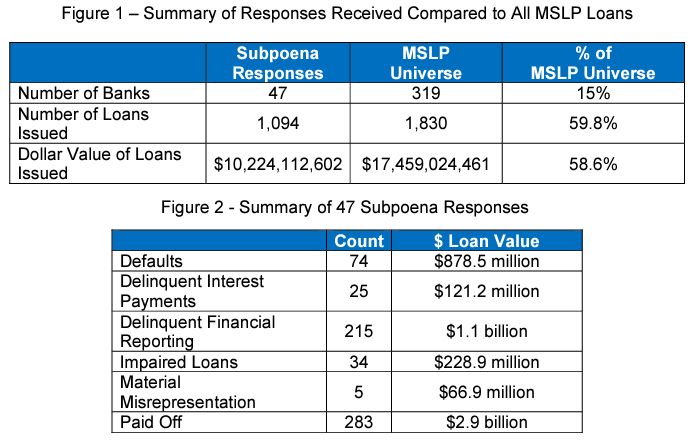

As of August 4, 2023, all 47 banks responded to our subpoenas for MSLP loan information. Those 47 banks issued 1,094 MSLP loans, at a value of over $10.2 billion. That represents approximately 60 percent of the total number of MSLP loans issued, and 59 percent of the total dollar value.

… Bank responses to our subpoenas show that of the 1,094 loans issued by the 47 responding banks, $878.5 million in loans are or were in default; $121.2 million in loans have or had delinquent interest payments; 215 borrowers are at least 90 days delinquent in providing required quarterly or annual financial reports; $228.9 million in loans are or were deemed impaired by the bank or by outside auditors or examiners; and 5 loans had borrowers where the bank determined that the borrower made material misrepresentations during the loan process.

Prayer-GPT

South Korean Christians turn to AI for prayer (FT)

About 20 per cent of 650 Protestant ministers in Korea recently surveyed by the Ministry Data Institute said they have used ChatGPT to create sermons and about 60 per cent of them found ChatGPT useful in coming up with ideas for sermons.

We faced strong resistance from churches initially with their suspicion that we are trying to replace God and pastors,” said Kim Min-joon, Awake’s chief executive. “But pastors began to appreciate our service as it helps them save time in preparing for sermons, and find more time to take care of lonely, troubled followers.

Asymmetries