Perspective on Risk - Nov. 11, 2022

A Conversation; Risk Adjusted Returns; Fed’s Financial Stability Report; CISA; Credit Suisse (or First Boston); Inflation and Valuation; Research Proves the Obvious; LDI; Regulation; Covid; More

A Conversation with Former Colleagues

I was having dinner with two esteemed former coworkers and PoR subscribers, and one of them said:

Brian, great newsletter. Lot’s of information, but it’s not prioritized. If you were still a risk manager, what’s the biggest thing you’d be worried about?

Great question; sort of knew it was coming.

Most of the information I share is boundary-spanning; from a Bayesian perspective, looking for information to adjust my priors and either refute or fit it to my larger long-term drivers/framework (demographics, technology, globalization).

After thinking for a bit, I answered thusly:

My biggest concern right now is that I’m pretty sure the recent past won’t be prologue. We seem to be at a number of potential real inflection points: the end of years of declining interest rates and disinflation; the possible end of Western hegemony; technology that is either at the last stage of improving productivity (chips/internet view) or the beginning of a wildly new world (artificial intelligence revolution).

I tend to be an empiricist. I prefer to look at data; I like formal models rather than relying on judgement (mental models in someone’s head). But in light of the inflection points, I am very cautious on whether past data and relationships will continue to hold. Empirical models may not hold; mental models may not work either.

We already know that correlations tend to be different when rates rise or fall, but even this observation is based on rate increases during a secular decline; we don’t have much information on rate declines during an environment of secularly rising rates and inflation. Writ large, it may mean we are undercapitalizing risk positions.

I also worry that too many decisionmakers have not lived through a real, long-term grinding recession like we had in the late 1980s. I have found that people rarely learn lessons from the past, and only learn from their own mistakes. This means mistakes will be made again.

Anyway, thought you might appreciate the discussion. Feel free to add your thoughts here

Risk Adjusted Returns

For those who say I only know how to talk about risk, but not the associated upside, eat this:

Fed’s Financial Stability Report

The Fed published their November 2022 Financial Stability Report. One of two Financial Stability Reports published in the US (the other is from the FSOC). Generally, not as insightful as the BIS or BoE reports. Joseph Wang has a tweet stream of his observations.

I didn’t find much surprising herein; the risks they cite are the ones that are popularly articulated. In general, it is a balanced view of the risks outstanding. It does have a useful discussion of Treasury market liquidity. Here’s my 2 cents:

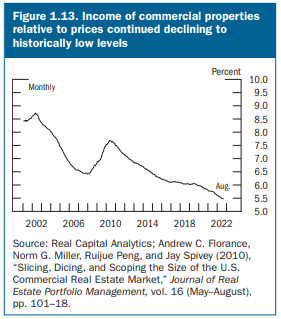

While equity and bond markets have adjusted down, the commercial real estate sector, at least according to their published metrics, remains overheated/hot. Cap rates are low and continue to fall. I think we should prepare for a late 1980s style CRE downturns (especially as virtually no risk managers around these days experienced the downturn). In general, land prices across RRE, farm and CRE all look inflated.

The share of leveraged loans being underwritten with >5x leverage remains surprisingly high.

Surprisingly little mention of emerging market economy risks; it is generically limped into “international risks.”

No discussion of stuck loan syndications using up balance sheet and liquidity, and possibly subjecting firms to future write-downs.

CISA

CISA stands for the Cybersecurity & Information Security Agency. Among their responsibilities is to act as the “National Coordinator for Critical Infrastructure Security and Resilience.” To that end:

In July 2021, President Biden signed a National Security Memorandum on Improving Cybersecurity for Critical Infrastructure Control Systems. This memorandum required CISA, in coordination with the National Institute of Standards and Technology (NIST) and the interagency community, to develop baseline cybersecurity performance goals that are consistent across all critical infrastructure sectors. These voluntary cross-sector Cybersecurity Performance Goals (CPGs) are intended to help establish a common set of fundamental cybersecurity practices for critical infrastructure, and especially help small- and medium-sized organizations kickstart their cybersecurity efforts.

To accomplish this, CISA has published CROSS-SECTOR CYBERSECURITY PERFORMANCE GOALS. Think of this as a basic checklist - a quick-start guide if you will - to implementing a secure environment. They provide a set of what I imagine are useful baseline tools:

A distinct subset of my audience will find this valuable.

More Credit Suisse (or First Boston)

Last month, for a few weeks, the Swiss National Bank utilized their dollar swap line with the Federal Reserve. The SNB drew $6.27 billion during the week of Oct 13, and more than $11 billion the following week. At the time, it was rumored that CS was facing a run.

Subsequently, on the week of Oct 27th, CS disclosed that it had experienced significantly higher withdrawals of deposits in the first two weeks of October "following negative press and social media coverage based on incorrect rumors".

On the Oct 27th earnings call, CS was asked about the LCR breach by Kian Abouhossein of JPMC and Piers Brown of HSBC. From the answers we can deduce that there were two factors at play.

First:

We had self-selected to be out of the capital markets during the month of October, given the strategic announcements that were coming today.

Then there appeared to be a run in the US:

You know, it's not lost on us that, look, you did see in the U.S., as a result of really liquidity in the system contracting, especially from central banks, that you did see large reductions in deposits in the United States as well.

Details are available from this Risk article Credit Suisse’s LCR down 20% in October as depositors flee (I can only access the first paragraphs; I don’t subscribe)

Credit Suisse’s average liquidity coverage ratio (LCR) dropped by a fifth in October, after a run on deposits during the first two weeks of the month.

Fuelled by what the bank called “negative press and social media coverage based on incorrect rumours”, the daily LCR averaged 154% between October 1 and October 25, compared with 192% through the three months to September 30. The bank said this was the result of a significant withdrawal of cash deposits and the non-renewal of maturing time

So what appears to have happened is that:

CS was out of the market pending the announcements

US customers, probably HF and large uninsured depositors ran the US institutions

The Swiss National Bank borrowed dollars from the Fed through the swap line to fund CS

This would be entirely consistent with the US regulators wanting to have their credit risk be to another central bank and not to the institution or its subsidiaries, and would be consistent with the SNB wanting to have control over the process.

Here is a nice fixed income investor presentation by CS that describes their plans. Marc Rubinstein’s Net Interest substack has a nice post on the changes Back to the Future - The Revival of Credit Suisse First Boston.

Welcome back First Boston.

Inflation and Valuation

Over on Linked-In, Doug Daschille points us all to the 1979 paper by Franco Modigliani and Richard Cohn, Inflation, Rational Valuation and the Market that calls out two errors investors make during times of inflation:

First, investors fail to adjust accounting profits for the gain enjoyed by stockholders which results from the real depreciation of nominal corporate liabilities. Unadjusted accounting profits will be adversely affected by rising nominal interest rates, whereas correctly measured profits should keep up with inflation.

Second, investors have a tendency to capitalize equity earnings using a nominal rate instead of the theoretically sound use of the real rate.

The paper requires a paid download. We’ve focused a lot on real rates, but not on the first error. Good reminder.

In the comments, Jim Conklin reminds us that:

[T]he industry's penchant for inverting earnings yields as P/Es [has caused some investors to forget that dividends (or earnings... whatever you believe to be the relevant thing to discount for a stock) grow in line with nominal GDP, not real GDP. That is, there is an inflation term in the discount numerator that cancels the inflation term inherent in the denominator. So while nominal rates rise with inflation, liabilities shrink relative to earnings.

The Best Research Proves the Obvious

Catering and Return Manipulation in Private Equity

We provide evidence that private equity (PE) fund managers manipulate returns to cater to their investors. Using a large dataset of PE real estate funds, we show that PE fund managers overstate returns if they oversee a larger share of their investors' assets, and doing so has a more significant impact on investors' reported returns. Additional cross-sectional results are inconsistent with models in which investors punish or are deceived by manipulations. In contrast, our results highlight an underlying tension in PE performance: the "phony happiness” that some PE investors receive from overstated and smoothed interim returns due to agency frictions within their organizations.

Or as Cliff Askness calls it, volatility laundering.

More on the UK LDI Problems

It appears that Apollo was a major buyer in UK pension fund fire sale (FT)

Apollo Global snapped up $1.1bn of assets from UK pension funds [through] its Athene unit [which] has lower return targets than traditional private debt funds, making the unit a good home for such distressed sales. Kleinman said Apollo’s purchases were made at an effective 8 per cent yield, a relatively high figure for the safest class of corporate loans.

“There was nothing inherently wrong with the CLO tranches we were buying,” said Kleinman. “[They] happened to be the most liquid asset that those entities had to liquidate in order to cover their leverage and margin issues.”

Probably a very good trade, and one I suspect we would have tried to be a part of in my old AIG days.

The Bank of England has written a nice letter explaining their actions around the LDI crisis.

Taken at face value, this market intelligence would have implied additional long-term gilt sales of at least £50 billion in a short space of time, as compared to recent average market trading volumes of just £12 billion per day in these maturity sectors.

The Bank was informed by a number of LDI fund managers that, at the prevailing yields, multiple LDI funds were likely to fall into negative net asset value. As a result, it was likely that these funds would have to begin the process of winding up the following morning. In that eventuality, a large quantity of gilts, held as collateral by banks that had lent to these LDI funds, was likely to be sold on the market, driving a potentially self-reinforcing spiral and threatening severe disruption of core funding markets and consequent widespread financial instability.

This is a classic example of a fire-sale externality, and the Bank did the exact right thing in bridging liquidity to maintain orderly markets.

Regulation

OCC Announces Office of Financial Technology

The Office of the Comptroller of the Currency today announced it will establish an Office of Financial Technology early next year to bolster the agency’s expertise and ability to adapt to a rapidly changing banking landscape. The Office of Financial Technology will build on and incorporate the Office of Innovation, which the OCC established in 2016 to coordinate agency efforts to support responsible financial innovation.

Covid

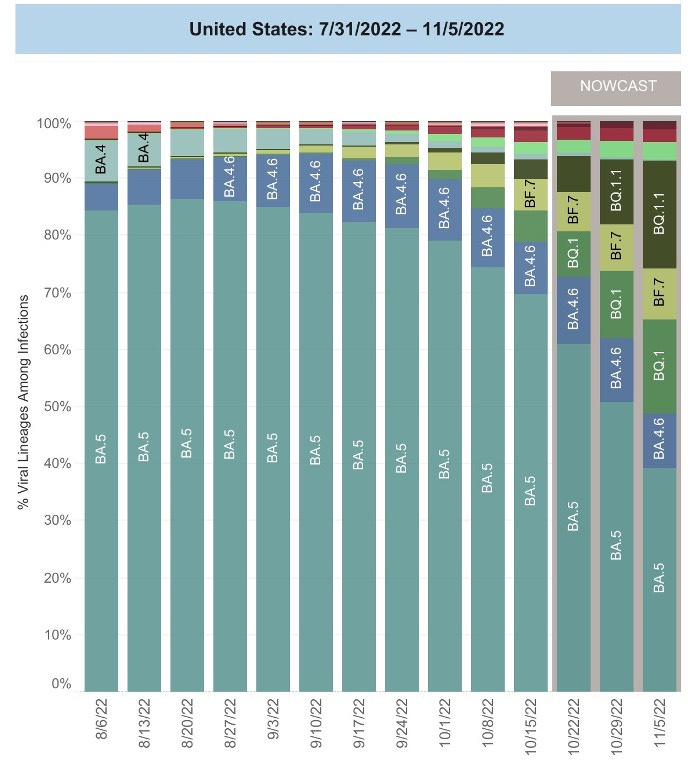

I know we are tired of Covid talk; I certainly am. Fortunately there are folks who are continuing to follow the emerging variants. Eric Topol’s Ground Truth substack recently published Daily pandemic briefing, 4 November 2022 discussing the recent rapid rise of the BQ.1.1 variant.

He provides a reason for optimism:

If we can withstand a significant wave from BQ.1.1 it would suggest that the Omicron variant soup is not nearly as big a threat as was envisioned. Why? Because our immunity wall of vaccinations, boosters, and infections may have cumulatively held up to the further evolution of the Omicron sub-subvaraints. That it would take a whole new “Omicron-like” event, a new family of variants, to wreak havoc again.

But this DOES mean that you should get the recent Omicron booster, particularly if you are in a vulnerable group.

More

NatWest Markets Pleads Guilty to Fraud in U.S. Treasury Markets

Back in the period form 2008-18, several Natwest traders spoofed the UST market:

By placing Spoof Orders, the Subject NatWest Traders intended to inject materially false and misleading information about the genuine supply and demand for U.S. Treasuries into the markets, and to deceive other participants in those markets into believing something untrue, namely that the visible order book accurately reflected market-based forces of supply and demand.

A decade later:

NatWest pleaded guilty to one count of wire fraud and one count of securities fraud

NatWest also will serve three years of probation and will agree to the imposition of an independent compliance monitor.

Rare for a firm to be found guilty (as opposed to the individuals). But Natwest was a repeat offender:

The 2018 securities fraud scheme constituted a material breach of the Oct. 25, 2017 Non-Prosecution Agreement between the U.S. Attorney’s Office for the District of Connecticut and NatWest’s U.S. broker-dealer subsidiary, NatWest Markets Securities Inc. (formerly RBS Securities Inc.), and occurred while NatWest (formerly The Royal Bank of Scotland Plc) was on probation following its May 20, 2015 guilty plea and Jan. 5, 2017 sentencing for conspiring to manipulate the foreign currency exchange market.

The Illuminati Has Officially Chosen to End Our Partnership with Kanye West (The New Yorker)

In light of his recent inflammatory, hateful comments, the Illuminati has made the decision to end our relationship with Ye, formerly known as Kanye West. West’s abhorrent, anti-Semitic remarks are unacceptable, and starkly go against the values of our global shadow regime.