Perspective on Risk - June 19, 2023 (Decoupling Update)

The Non-de-dollarization; Restrict Capital Flows; Expropriate Russian Assets; De-dollarization is Popular; Russian Perspective; BRIC Bank Needs Dollars; Toose on Invoicing; Chips

Folks, there are some enormously important articles referenced in this Substack; the first three in particular:

Newman & Chapman argue the dollar will grow, rather than shrink, in influence.

Pettis thinks it would be in US interests to restrict capital inflows (and the $ be damned) - this is a must-read article.

Summers, et. al. want to expropriate Russian financial assets

Setzer points out that dedollarization is popular … in countries that don’t have any dollars left in their reserves

A Russian professor admits Russia’s actions will not be able to make its currency a global means of payment; nor will it be able to undermine the dollar hegemony by its actions

A bank set up to finance BRIC projects outside the dollar system … is finding itself short of dollars.

Toose shows why shifting away from dollars is so difficult

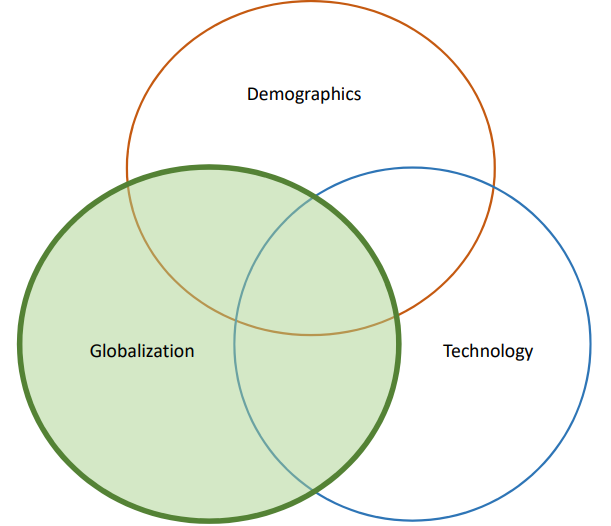

For those new to the substack, you may want to peruse some of the earlier posts on decoupling. The essence of my view is that there are powerful long-term factors that affect capital flows and returns on labor and capital. The big three are demographics, technological change, and trends in globalization. Climate change now gets an honorable mention. The decoupling discussion was sparked about 18 months ago by Zoltan Pozar of (the late) Credit Suisse.

Perspective on Risk - April 18, 2023 (Decoupling Update)

The Non-de-dollarization

You don’t find many individuals with the perspective of Jay Newman and Meyrick Chapman. So what they say matters.

In defense of the dollar (JAY NEWMAN AND MEYRICK CHAPMAN)

There is a credible threat to dollar supremacy, but that threat comes more from fragmentation than the emergence of a true competitor. For America’s rivals, though, fragmentation is good enough, as it damages the dollar system — but less obvious is that it will also be very costly, reduce information and flexibility, encourage fragility and abet repression.

Examined closely, however, the origin story — that the dollar is dominant because trade is denominated in dollars and that the role of the dollar in trade is eroding — is fatally flawed. And it’s not just wrong on the volume of trade, it has things backward in terms of why the dollar is so useful.

International trade isn’t the right measure of the dollar’s significance — the gold standard here is its role in financial transactions.

That fact is that trade and financial transactions are denominated in dollars because the dollar is trusted. And that trust has been earned because contracts governed by U.S. (and U.K.) law — i.e. common law systems — embody legal and social norms that have been developed and tested over centuries. Rivals can offer nothing even remotely comparable.

In fact, there’s reason to argue that common law — enforceable in U.S. and U.K. courts — not only underpins the value of the dollar but is, in and of itself, the equivalent of a reserve currency. Rather than failing and fading as geopolitics becomes more fraught and contentious, both the dollar and the legal system that defines it will grow in influence and utility.

Pettis Believes It Would Be In The US Interest To Restrict Capital Inflows (and dollar dominance be damned)

America Cannot Continue to Absorb Global Imbalances

It is important to understand the U.S. trade deficit within the context of global trade. In spite of the World Trade Organization (WTO) and other global entities designed to enforce free trade, the world is experiencing one of the most mercantilist periods in history.

The fact that we live in a world with the largest, most persistent trade imbalances in history is more than sufficient proof that mercantilist policies in individual economies are preventing the necessary adjustments that make free trade beneficial for the world.

The role that the United States plays in the global economy … is the absorber of last resort for excess foreign savings, it must also be the consumer of last resort for excess production, which means foreign manufactures have privileged access to American consumers relative to American manufacturers. It is not in the best interest of the American economy that it continues to play this role.

If the United States wants to eliminate its trade deficits, it must change tactics. Rather than restrict trade, the policymakers must restrict the ability of countries that run persistent trade surpluses to dump their excess savings into U.S. financial markets. They should unilaterally restrict harmful capital inflows in ways that leave productive, long-term investment in the American economy unaffected.

Of course, restricting inflows will partially undermine the global dominance of the U.S. dollar, so the necessary policies will almost certainly be opposed by Wall Street, by billionaire owners of highly mobile capital, and by the foreign policy establishment. They will however benefit American manufacturers, workers, small businesses, and middle-class savers, and ultimately will result in a healthier, stronger American economy and industrial base with a larger share of global manufacturing.

Expropriating Russian Assets

In Foreign Affairs, Summers, Zelikow and Zoellick write The Other Counteroffensive to Save Ukraine.

As Ukrainians risk their lives battling for national survival, the United States, European countries, and their allies should prepare a counteroffensive of their own against Russian aggression: a massive new European recovery program to begin operation by next year.

To give this plan credibility, Western countries should prepare to use frozen Russian assets to help fund Ukraine’s reconstruction.

Here’s the interesting point:

Russia should bear the bulk of these costs. ….Those now frozen Russian state financial assets probably total about $300 billion. Most of the funds are held in euros, with the bulk of these EU holdings concentrated in Belgium’s Euroclear clearing house. But significant Russian financial assets are also frozen in the United States, the United Kingdom (including the Cayman Islands), Switzerland, and several other countries.

They discount the downside

Some worry that transferring Russian assets would be so pathbreaking that it could scare countries away from holding large foreign exchange reserves from countries that implement countermeasures.

Some analysts worry that transferring them could threaten the status of the dollar in international finance.

Some long-term concerns about the dollar’s role in the world economy are valid, but a transfer of Russia’s already frozen reserves would not add much to those concerns. To begin with, the United States would be acting in concert with issuers of other major reserve currencies, such as the euro, yen, and sterling.

Concluding:

Far from a dangerous precedent, a transfer of Russian assets would be a powerful warning to other countries that may be considering wars of aggression. It would be a reminder of how costly it can be to assault global norms in a world that is still so deeply interconnected.

De-dollarization is Popular

(in Countries That Don’t Have Any Dollars)

Exclusive: Pakistan paid in Chinese currency for discounted Russian oil

Pakistan paid for its first government-to-government import of discounted Russian crude oil in Chinese currency, the South Asian country's petroleum minister said on Monday, a significant shift in its U.S. dollar-dominated export payments policy.

Discounted crude offers a respite as Pakistan faces an economic crisis with an acute balance of payments problem, risking a default on its external debt. The foreign exchange reserves held by the central bank are scarcely enough to cover a month of controlled imports.

A Russian Perspective

A professor and the chair at the Department of World Economy at Moscow State Lomonosov University writes in Russia’s Dedollarization Delusion

Moving beyond payment settlements in dollars has long been on the Kremlin wish list — an objective clearly fueled more by geopolitical aversions to the United States than economic considerations. Russian leaders have sought this over the past twenty years with a wide range of methods, and with mixed and often unforeseen results.

In the first half of the 2000s the main declared task declared was the convertibility of the ruble; the idea was to turn it into a currency that could be taken seriously on global currency markets.

These days it is difficult to say how realistic such a goal seemed then. It is only obvious now that nothing was done to achieve it: clearly, no international lending market for the ruble was built.

With the outbreak of the war … It was then decided to collect new reserves (if they manage to accumulate them at all) exclusively in Chinese currency. … Russia is gradually shifting its focus from the currencies of «unfriendly» countries to other instruments, but the ruble is used only in cases where other options are not fundamentally considered.

An instance of how an arbitrary decision to switch to settlements in national currencies does not work is Moscow’s attempt to trade in rubles or rupees with India, for which Russia

A more credible alternative payment alternative could be the Yian.

China is Moscow’s most important trading partner, from which Russia buys goods and services worth almost $ 80 billion a year. Therefore, the accumulation of reserves in yuan now looks relatively reliable — as far as anything can be reliable in today’s Russia and around it. The Chinese currency is also used in international settlements, although its share in global trade in goods does not exceed 4.5%, and in international currency exchange transactions — 7%. But these indicators are quite sufficient for Russia to rely on it, with its 2.6% share in world trade. China has recently been actively and successfully establishing a regime of bilateral settlements with countries across Africa, the Middle East and Latin America — so the yuan, unlike the rupee, looks attractive.

Russia — and this can be said quite definitely — will not be able to make its currency a global means of payment; nor will it be able to undermine the dollar hegemony by its actions, but it is possibly capable of finding options for ensuring safe and relatively efficient settlements with the replacement of the dollar or the euro with the yuan or dirham.

BRIC Bank Needs Dollars

A Bank China Built to Challenge the Dollar Now Needs the Dollar (WSJ)

Eight years after Chinese leader Xi Jinping and his counterparts from Brazil, Russia, India and South Africa established the New Development Bank, with headquarters in a swanky Shanghai skyscraper, it has all but stopped making new loans and is having trouble raising dollar funds to repay its debts, according to an examination of its finances and interviews with bankers and others familiar with the matter.

the Brics’s development bank is fighting for its very survival, threatened by its own reliance on the U.S. currency.

After setting up shop in Shanghai in 2015 with $10 billion in committed capital from the five founders, the members found it would be difficult to rely only on China’s banks and capital markets. The development bank began to borrow billions of dollars from institutional investors on Wall Street as well as China’s state-owned banks. Some of what it borrowed was denominated in China’s yuan, but around two-thirds of the bank’s borrowings are dollar-denominated—hardly in line with the bank’s stated aim to break their members’ reliance on the dollar.

Invoicing

If we go back to the Chin framework, there are four mutually reinforcing roles that make the USD the global reserve currency:

Invoicing transactions

Trade Financing

Investing and borrowing

Currency hedging

We discussed in the last decoupling update how many of the headlines about countries transacting in the Ruble or Yuan were less than meets the eye. But it has been hard to get firm figures to understand how trends in invoicing and trade financing are evolving.

Adam Tooze has a useful Chartbook #211 Bucking the buck? Debating the global dollar ... again!

As far as trade is concerned there has been an increase in the share of China’s trade invoiced in yuan. But as Gerard DiPippo and Andrea Leonard Palazzi point out in a very useful CSIS post, this not a secular trend. Rather it is a partial return to levels of yuan-invoicing, which before 2015 were much higher.

The deals done since 2022 have been motivated not by commercial but by explicitly political motives, largely centered on Russia’s ostracized position. They have been in large part bilateral agreements. They do not, therefore, suggest the emergence of an alternative yuan-based network of international finance and trade.

But he then calls attention to Pakistan Keen to Pay for Russian Oil Imports With Chinese Yuan stating:

The Russo-Bangladeshi agreement to transact in yuan is significant….

Shifting the trade in oil from dollars to yuan would be a more substantial shift. But it echoes half a century of similar suggestions none of which have so far produced a significant shift. And if the Chinese and Saudis actually followed through it would expose what is the underlying question which is, where the Gulf states would invest their petroyuan. Will the Saudis be willing to invest petroyuan in Chinese government debt in the face of capital account controls?

Chips Replacing Oil

Chile plans to nationalize its vast lithium industry

Chile's President Gabriel Boric said on Thursday he would nationalize the country's lithium industry

Future lithium contracts would only be issued as public-private partnerships with state control, he said.

Codelco and state miner Enami will be given exploration and extraction contracts in areas where there are now private projects before the national lithium company is formed.

Global chipmakers to expand in Japan as tech decoupling accelerates (FT)

Seven of the world’s largest semiconductor makers have set out plans to increase manufacturing and deepen tech partnerships in Japan as western allies step up efforts to reshape the global chip supply chain amid rising tensions with China.

At an unprecedented meeting in Tokyo with Japanese prime minister Fumio Kishida, the heads of chipmakers including Taiwan Semiconductor Manufacturing, South Korea’s Samsung Electronics and Intel and Micron of the US described plans that could transform Japan’s prospects of re-emerging as a semiconductor powerhouse.

The risk to seizing Russian reserves and other assets for the purposes of rebuilding Ukraine is that it expands the conflict from supporting an ally against an unjust invasion, i.e., an indirect participation in the conflict, to a direct attack on one of the belligerents in the manner of asset confiscations. That is exactly contrary to the US government's position of limiting the conflict. It increases the likelihood of a wider war and Russian retaliation in any of several forms, e.g., terminating the grain export deal, seizing NATO country vessels, etc. The idea sounds justified but it is fraught with risk.