Perspective on Risk - July 29, 2024

Supervision; Mortgage Servicers; CRE; Private Credit; Liquidity in Privates; Llama's are a systemic risk.

Supervision Stuff

Petrou at Peterson Institute for International Economics

Interesting perspective from Ms. Petrou. I’ve highlighted some of her stuff before, sometimes agreeing and sometimes not. I’ll highlight some points from her remarks and give my reaction at the end.

U.S. Bank Supervision: How to Make It Both Good and Just

What I find most discouraging about the United States’ supervisory situation is how much remains unchanged in terms of structure, results, and supervisory accountability not just since March of last year, but also since the 2008 Great Financial Crisis (GFC)

She cites four areas: Speed & Certainty, Effectiveness, Accountability, and Just Supervision.

… many confidential reports showing that bank examiners often quickly spotted looming problems … [issued] meaningful enforcement actions only when it was far too late.

Large examination bureaucracies are at grave risk not just of lethargy, but also of being encumbered by so many internal reporting requirements and conflicting incentives that they lack the ability to distinguish material weaknesses from minor failings and then to rapidly resolve or punish persistent material weaknesses and violations. With so many examiners who, like all employees, are worried at least as much about themselves as about bank safety and soundness, there is no way to ensure that supervision does not spend so much time examining superficial scratches that mortal danger is missed.

In the U.S., the public is only given the information needed to hold supervisors accountable after a bank fails. That is, of course, far too late. … CAMELS ratings assigned insured depositories and the like-kind ratings assigned their parent holding companies [should be publicly released]. … Knowing that a CAMELS rating will be public and depositors will soon learn of it is a tough-minded, but effective way to ensure that supervisors know their reputations are at risk if they focus on internal incentives instead of rapid remediation and that bank management cleans up its act before market discipline demands that it does so in no uncertain terms likely past the point of recovery.

Supervision that is not only good, but also just must balance effective response and mandatory injunctions with the need always to ensure that the rights of supervised banks to a hearing if supervision goes too far must be respected.

First, much of this is spot on. We’ve discussed this before when discussing SVB.

An examination team has a wide variety of skill sets and experience, but one aspect she highlights, spending much time examining superficial scratches, is a good place to start. Until they get considerable experience, every examiner believes that their “findings” are the most important thing; it doesn’t matter whether it is credit, BSA, interest rate risk, or whatever. Examiners generally do not let things slide because they sense the risk is immaterial, and in some cases like BSA/AML they can’t.

It is then the job of the more senior examiners and their supervisors to prioritize the findings, determine and justify a rating, and write up a report. This leads to the need for another of her criticisms: the need for examination bureaucracies. The first level of “vetting” is by the examiner team and the EIC themselves. Sometimes, this vetting is helpful in identifying cross-cutting issues and root-causes of problems. I have generally found that bank management appreciates this perspective. A second level of vetting occurs at the managerial, or portfolio level. For a while, when I was at the Fed, as a manager, we tried to focus the examination reports much more directly on the most germane findings. But I imagine as we have moved back into a world of more aggressive supervision, it has become more important to document and put management on record for everything that has been found.

The “examination bureaucracy” is also an important way to control for her last point, that the supervisory response is “just.” In fact, I would argue, that during my time at the Fed this was of upmost importance. Findings, ratings and report language were consistently “vetted” to insure that we were treating similar banks equally. This was in fact one of the reasons for the creation of “horizontal reviews.”

All of this vetting takes time, and results in a de-prioritization of some issues. And it is possible that this results in something important getting deprioritized. The conduct of a horizontal review also can add time. If a team is evaluating six banks, and wants to provide the firm with perspective on how they compare to peers, the first firm reviewed will certainly be waiting for a bit.

Changing this process results in additional variation at some level. Eliminate the managerial review and you may have more “injustice” due to discriminant treatment of firms.

That leaves us with her third point: should we disclose supervisory ratings? As with our discussion of the stigma of borrowing from the Discount Window, disclosing ratings puts an additional piece of information into the market, in theory, at least, aiding “market discipline.” Petrou feels that disclosing the ratings lets “supervisors know their reputations are at risk.” I support her proposal in theory, but worry that it would provide the opposite incentive when dealing with the largest banks. She writes:

U.S. practice has been to cloud CAMELS ratings because regulators fear the consequences of objective, cold-hearted market discipline.

This exact fear will lead to pressure to not downgrade a bank. I have seen it in action already, as there are signals that the market can read, such as a prohibition on mergers, that can signal when a bank is in the penalty box. One must also ask how we would feel if a foreign regulator publicly downgraded a significant US bank leading to a run.

However, and I am probably an outlier in the supervisory community, but I think the benefits of disclosure (perhaps with a short six month delay) outweigh the risks. And more so for the GSIBs than the smaller banks; market discipline will be more effective there. Perhaps we need to overcome our fears.

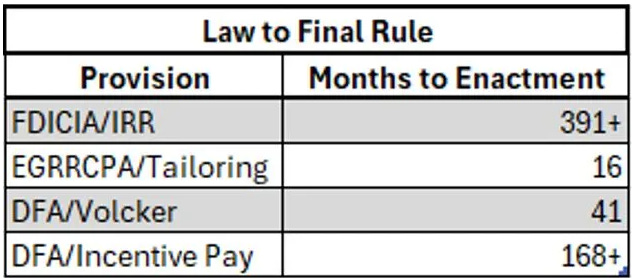

Always Take The Over

The UponFurtherAnalysis blog, which appears to be written by an OCC supervisor, authored Regulatory Limbo that discusses timeliness in both supervision and regulation.

Bank supervision for SVB and other failed banks lacked a sense of urgency. But at least the bank supervision process follows some specific timelines. For example, at OCC, we needed to send a Supervisory Letter out within 45 days of completion of field work. Paradoxically, the higher the stakes, the slower the process. One reason corrective actions for SVB took so long was that the vetting process was so extensive. Similarly, an exam team can issue an MRA in several weeks (or shorter if it’s urgent) while formal enforcement actions take months, even years.

We don’t see the same hard deadlines with regulations. That not only means that regulations take longer but there is more variability around the timelines.

There can be good and bad reasons for this.

Some regulations are much more complex than others.

Some meet stiffer resistance, but the resistance can just as easily reflect lobbying efforts as democracy in action.

Regulators usually prefer to enact big rules on an interagency basis. Getting each of the agencies to agree takes time. That’s not necessarily a good reason but it’s an understandable one.

Speedy or slow enactment may also reflect a regulator’s preferences and priorities rather than practical impediments.

Chevron will make things even worse.

Recent court decisions invite legal challenges and are likely to make the rulemaking process even slower. Fear of litigation will probably also make regulatory timelines even more one-sided. Litigants need both standing and deep pockets, so banker-friendly initiatives will likely remain on the fast track. Regulations opposed by the banking industry or by other powerful interests will likely remain in limbo.

Operational Risk

Secret Bank Ratings Show US Regulator’s Concern on Handling Risk (Bloomberg)

In the confidential assessments, the Office of the Comptroller of the Currency said 11 of the 22 large banks it supervises have “insufficient” or “weak” management of so-called operational risk …

That contributed to about one-third of the banks rating three or worse on a five-point scale for their overall management …

Deposit Insurance & Market Discipline

A level playing field for deposit insurance (Logan)

In discussing Karen Petrou’s remarks above, we touched on the role of market discipline. Certainly during the Greenspan era, and into the Bernanke era, market discipline was a much ballyhooed tool for controlling a banking system. And since I came up in that system, I guess you can say I drank the cool-aid.

Pres. Logan raises the possibility of raising the level of deposit insurance.

Federal insurance coverage is limited to $250,000 per depositor. That limit is supposed to give small depositors confidence while creating incentives for larger depositors to investigate their banks’ condition. While large depositors could theoretically provide helpful market discipline, they also often perceive—rightly or wrongly—that some banks are too big to fail and that the government will bail out those banks or their depositors in a crisis. Such perceptions undermine market discipline and tilt the playing field toward big banks.

The perception that certain banks are too big to fail tilts the playing field. Some people argue that stringent regulations on big banks counterbalance any too-big-to-fail benefits. But even if the costs and benefits of size are equal most of the time, the equation breaks when stresses emerge and the value of a perceived guarantee is suddenly much larger.

Conceptually, there are a couple of possibilities for restoring balance. Regulators could adopt even tougher regulations on the largest banks. But such regulations could put a drag on the economy by raising big banks’ costs for some of the unique and critical intermediation services they provide.

I really dislike this last sentence. It implies that we are comfortable subsidizing the cost of capital of the largest banks because of the “unique and critical intermediation services they provide.” Perhaps if we weren’t distorting the market cost of capital, their services would not be unique!

Or, authorities could increase the deposit insurance limit so that deposits would be more equally protected at all banks. The FDIC proposed some interesting options along those lines in a report last year. Of course, the benefits of a higher limit have to be weighed against potential costs, such as whether deposit insurance premiums would need to rise or whether a higher limit could increase moral hazard and encourage banks to take excessive risks.

An interesting study would be to see if the size of the TBTF deposit subsidy has shrunk relative to the regional banks now that the systemic risk exemption was used in the SVB case. In the immediate aftermath of SVB, the subsidy clearly increased as depositors flocked to the TBTF banks and the regulators stated that this was a one-off and not a policy change.

In SVB’s case, I’m not sure that deposit guarantee size was the determining factor in the run; it was more the nature of the funds: payroll, etc.

Preventing Regional Bank Mergers Entrenches The TBTF Premium

The Bank Policy Institute, a lobbying group for large banks, published Regional Bank Mergers Would Increase Competition without Increasing Systemic Risk. In it, they are pushing back against regulatory restrictions on regional bank mergers. They argue that these mergers would be safe and increase competition for the GSIBs.

And while this is true, I believe that the rules only serve to entrench the GSIBs by increasing the barriers-to-entry in their businesses. There is an alternative to creating more GSIBs, and that is reducing the systemic risk of the existing GSIBs by breaking them up.

But back to the BPI paper:

… the OCC’s recently proposed merger policy framework would effectively hobble the ability of large regional banks to compete by stating that approved mergers generally should result in institutions under $50 billion in total assets—a feature “consistent with approval” that could easily be misconstrued as prohibition against combinations that would exceed this arbitrary threshold. Similarly, the FDIC proposes “heightened scrutiny” for mergers that result in a combined entity of over $100 billion in assets. There is no statutory nor analytical basis for these thresholds, and they contravene the policy objectives of Congress in enacting statutory size limits on bank acquisitions including a prohibition on transactions where the combined entity exceeds 10 percent of insured deposits or financial system liabilities by imposing far more severe size limits.

… to replicate the nationwide dominance of the largest U.S. banks in both scale and funding stability, multiple banks in Category III and IV[9] would need to combine.

Indeed, using any measure of systemic risk, any resulting institution from these hypothetical combinations of large—but noncomplex—regional banks would inherently present far less systemic risk than that presented by the existing U.S. GSIBs, as demonstrated in Figure 4 below. And of course, more realistic combinations involving any two regional banks would present even less systemic risk than these hypothetical multi-bank mergers.

Graham Steele, who I’ve quoted before, had this reaction via his Twitter/X account.

A few responses to this piece on one of the hottest topics of the moment: bank consolidation. It's important not to be fooled by some pretty clever arguments. They'd result in less regulation, less competition, and more risks to financial stability. 1/

On financial stability, it says measures of systemic importance support more regional bank mergers. These metrics under-count the risks of domestically focused banks. SVB had a very low score but its failure required a systemic risk determination. These banks are much larger. 2/

On competition, again, the piece observes that regional banks have much less market share than their globally systemic counterparts. But more deregulation and more consolidation will only make the concentration of credit worse, not better. 3/

The piece says a proposed $100 bn threshold for merger review is contrary to law. But the law says banks of that size need enhanced regulations. And when Congress pass the 10% deposit limit, it was clear that mergers below that threshold should still be denied. 4/

Contagion Between Banks And Insurers

Measuring capital at risk with financial contagion: two-sector model with banks and insurers (Bank of England)

The Bank is focused on the right things, The US regulators are hamstrung by the fragmented nature of regulation of both banking and insurance.

In this paper, the Bank tries to answer the following question:

How do interdependent economic shocks impact the [UK] financial system and reverberate within it?

So what do they conclude?

Overall, we find that, since the Covid pandemic (2020–21), the UK financial system has experienced an improvement in both profit expectations and tail losses. Comparing sectoral losses in an extreme stress scenario, we find that insurers are more affected than banks by economic credit and traded risk losses, while fire sale losses affect banks more than insurers.

Good paper for us contagion nerds.

Don’t Backstop The Mortgage Servicers

Opinion | Why Is the Government Encouraging a Taxpayer Bailout? (Politico)

Mortgage origination and servicing are now increasingly dominated by nonbanks such as Lakeview, PennyMac, Rocket, United Wholesale and Mr. Cooper.

Massive growth in nonbank mortgage companies is one of the major structural changes that’s occurred in the mortgage market since it played a star role in the global financial crisis of 2008. Back then nonbank companies owned servicing rights for 4 percent of mortgages; today it is 54 percent.

… the Financial Stability Oversight Council (FSOC) recently released a report focusing on the risks arising from the current regulatory structure for mortgage servicing … [that] included a suggestion that Congress create a permanent bailout fund to underwrite these risks.

… this is a terrible idea.

Congress … tasked FSOC with the responsibility “to promote market discipline, by eliminating expectations … that the Government will shield … losses in the event of a failure.” By suggesting Congress create a backstop for mortgage servicers, FSOC undermined market discipline.

FSOC should also direct its member agencies to set standards for mortgage servicer companies

Instead of accepting that bailouts are inevitable — or actively promoting them — FSOC needs to use its power and authority to improve the oversight of our mortgage markets, and make clear that if a mortgage servicer or any other financial institution fails, it will be private investors and creditors who lose money, not taxpayers. That is the way to ensure market discipline and end the bailout cycle.

Commercial Real Estate

Single Asset Deals Imploding

The financial models behind the ratings never forecast property prices falling below the value of the debt.

Real-Estate Meltdown Strains Even the Safest Office Bonds (WSJ)

The commercial real-estate meltdown is spilling over into the bond market.

Defaults are mounting in a favorite Wall Street mortgage-bond investment …

There are about $260 billion of the deals, known as single-asset, single-borrower bonds, held by investors such as banks, insurers, pensions and mutual funds. …

These so-called SASB bonds were meant to be ultrasafe, but the rate of loans at or near default has nearly tripled over two years, hitting 8.7% in 2024, according to data from the CRE Finance Council.

The losses are particularly jarring for investors because credit-rating firms initially gave many of the bonds triple-A ratings—higher than even U.S. Treasury bonds. The financial models behind the ratings never forecast property prices falling below the value of the debt. …

Bonds are getting hit now because debt is coming due on properties that were able to limp along for years. …

S&P Global Ratings and Morningstar DBRS rated about half the [1740 Broadway] bonds triple-A. They cited … their faith that Blackstone, one of the top private-equity firms in the country, would protect the investment if L Brands ever moved out.

Aaa defaults are highly destabilizing if they broaden.

Banks & CRE Losses

My working hypothesis, after looking at the data, is that the CRE downturn we are having may result in significant losses, and perhaps failures, at small and medium sized banks, but will not threaten the large banks or the health of the financial system more Broadly. Now, the OFR has published Bank Health and Future Commercial Real Estate Losses. I’ll summarize their conclusions, but it is worth a read.

The analysis shows that if CRE loan losses approached levels experienced in prior CRE downturns, hundreds of banks could have CRE loan losses and unrealized securities losses that exceed their shareholders’ equity.

The OFR uses historical loss rates to estimate potential losses. Using a CRE loan loss rate of 7.3% that represents the peak observed in the 2007-2009 financial crisis, they estimate 278 vulnerable banks are generally smaller, with $1 billion or less of assets, and primarily operate in suburban and rural locations in the Midwest and South.

FRED doesn’t have good time series data going back through the late 1970s and early 1980s. I have said that I thought that this CRE downturn would approximate the downturn from the late 1980s/early 1990s. I remember that downturn as being more material than the 2007 downturn, but it appears I may be wrong. I do know that it was significant for many large banks.

Private Credit

The FT has a nice info-graphic primer on the whole private credit trend, How private equity tangled banks in a web of debt. If you need to understand the basics, I highly recommend it. (hat-tip to David Kogan)

Matt Levine took notice in Private Equity Puts Debt Everywhere and got to the nub of the matter:

… could the private equity industry pose a risk to the wider financial system?

Sure? I guess? I am not particularly worried — the banks’ claims on all of this stuff seem pretty senior, and the substrate at the bottom of all of this leverage (cash flows from lots of businesses) seems reasonably robust and diversified. But a (the?) main risk to the financial system is when people put money into assets that they think are safe, and those safe assets turn out to be correlated and risky. The more sorts of safe tranches you manufacture out of the basic raw materials of business cash flows, the more ways some of them could go wrong.

I think that’s what I’ve been saying. Especially when they begin to be used as cash-equivalents.

Liquidity In Privates

Private Equity

A Private Equity Liquidity Squeeze By Any Other Name

… in April, Princeton’s Andrew “Sparky” Golden, the legendary outgoing CIO at PRINCO, told Financial Times this has been the “‘worst ever environment’ for liquidity” in private equity.

The breathtaking pace of the Fed’s rate rise cycle to combat the worst inflation since the 1980s impaired the deal climate for financing rounds, M&A and IPOs. Transactions stalled with GPs, portfolio companies and founders wary of undercutting heady valuations from frothier times.

Cash distributions to LPs fell to 11.2% of funds’ NAVs in 2023, the lowest level since the GFC and far south of the 25% median of the past 25-year period, according to Raymond James, while Cambridge Associates estimated distribution yields from US PE firms at 9%. Based on a survey of five of the largest private equity managers, Bloomberg pinned the drop in distributions at -49% in 2023 from 2021’s levels.

Continuation funds, which allow GPs to sidestep deeper losses while returning capital to investors who seek distributions, have become increasingly popular. Further telling of pressure to return capital to LPs, the secondary market for VC has also “exploded”

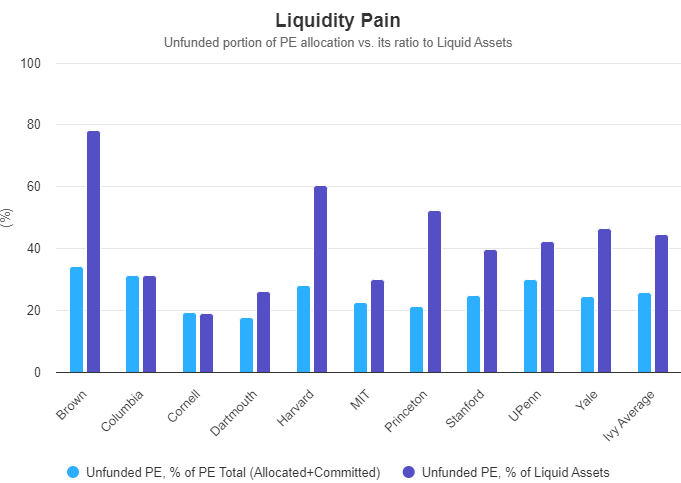

It is amidst this environment that Ivies, fortunate to have pristine Aaa credit ratings, have tapped the bond market for financing needs

Here … we show the portion of endowments’ PE allocations that are unfunded and then measure that $ figure’s ratio to liquid assets in each endowment.

The Ivy average unfunded PE allocation as a percentage of liquid assets is 44% … Brown’s liquidity pain potential is significant. In addition to leading the group of elite endowments in unfunded portion of PE allocation, their unfunded PE as a percentage of liquid assets – at over 78% – is significantly higher than peers.

University budgets have become increasingly reliant on endowments. Per NACUBO (H/t Financial Times Alphaville), the average university budget that was derived from endowments in the 70’s was 4%. Today, over 17% of “larger, better-endowed” schools’ budgets are funded from their endowments.

There’s a lot more good stuff in this piece, if you’re into this kind of stuff.

Hedge Fund Liquidity

Hudson Bay Joins Hedge Funds Locking Up Investor Cash for Longer (Bloomberg)

Sander Gerber’s firm in April transitioned clients in its flagship fund to a 12.5% quarterly investor gate level, down from 25% — meaning it will now take two years to fully exit the fund instead of one.

Hudson Bay joins other multibillion-dollar firms that have prolonged their lockup periods, though its two-year lockup is shorter than many of its competitors.

Llama Is A Systemic Risk

No, not Frank-the-Wonder-Llama (my college roommate), but Meta’s new open source AI model. Meta’s Llama 3.1 breaches the computational limit for posing a systemic risk in the EU.