Perspective on Risk - July 10, 2023 (Capital)

Framing; Barr Speech; How Much Would Have Been Saved If TLAC Was In Place For Failed Regionals

Disclosure

For the record, I was part of the Federal Reserve team that implemented the market risk amendment to the original Basel Capital Accords, and I was part of the BIS’s Models Working Group that developed the Basel II approach to capital. I also contributed to the Fed’s initial treatment of credit derivatives under the original Accord.

This affects how I think about capital

Framing

Basel II is dead; long live Basel III.

Basel I with its standardized risk weights was broken, led to banks lending to the riskiest (and highest returning) borrowers for a given capital change.

The genesis of the Basel II approach was simple.

Incent banks to capture their own history of credit default and migration

Require the sophisticated banks to calculate their own risk based upon their own risk profile. This would build upon their internal economic capital models, and encourage the development of more rigorous and well-constructed models.

But that vision didn’t even completely make it out of the Basel II starting gates before regulators sought to constrain and standardize the approach. This forced the banks modelling towards a regulatory-approved approach, not an internal-approach.

Basel II is yet another nail in that coffin.

This Is About Capital Requirements, Not Capital

Requirements is a key concept here: the Fed does not determine what is capital, they determine what qualifies as capital for the purpose of meeting a regulatory determined minimum threshold.

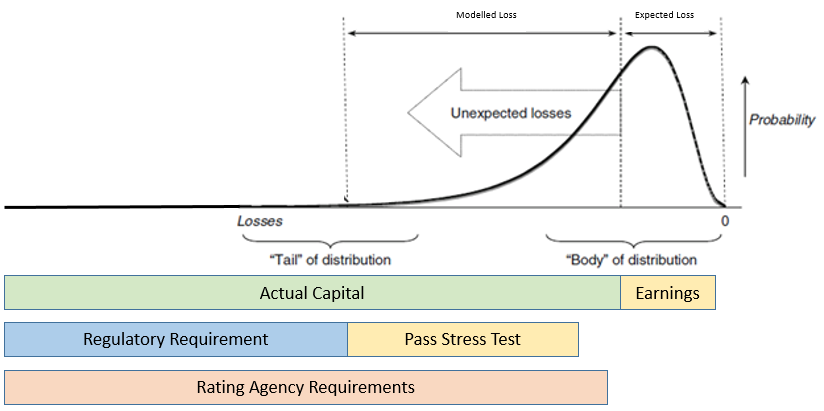

Higher Capital Requirements Lessen Losses to The Deposit Insurance Fund;

Higher Capital Buffers Reduce the Probability of Failure

Rating Agencies Essentially Dictate Minimum Requirements

For all leveraged financial systems, there is some degree of stress that will cause failures.

Regulatory minimum capital insures there is some value to the estate following failure that can offset the need for the sovereign to inject public capital.

Minimum regulatory standards set a threshold for regulatory intervention. Capital is held above the regulatory minimums to lower the probability of crossing the regulatory threshold.

Market requirements for capital can and usually are set differently from the regulatory measures. They can be lower or higher than the regulatory expectations.

The credit rating agencies will set their expectations for the size of the buffer required. This may or may not align with the ‘stress test buffer’ set by regulators.

Firms will try and operate as close to their view of the economic capital requirements as possible in order to earn the expected market return. This will lead to both proper business decisions and regulatory capital arbitrage.

Regulators design the speedometer; rating agencies set the speed limit.

Barr Speech

Barr has begun to release the details of proposed changes to regulatory capital requirements in his speech Holistic Capital Review.

As Barr states, these requirements are already quite complex:

The existing approach includes the risk-based requirements, stress testing, the risk-based capital buffers, and the leverage requirements and buffers.

Proposed Changes

Reduced Use of Own Estimates

First, for a firm's lending activities, the proposed rules would end the practice of relying on banks' own individual estimates of their own risk and instead use a more transparent and consistent approach.

The proposal would continue to permit firms to use internal models to capture the complex dynamics of most market risks but would not rely on banks modeling certain market risks that are too hard to model.

Firms would also be required to model risk at the level of individual trading desks for particular asset classes, instead of at the firm level. The proposal would also introduce a standardized approach that is well-aligned with the modeled approach, for use where the modeled approach is not feasible.

The Stress Tests Are Not Going Away

I believe that the stress test should continue to evolve to better capture risk. The exploratory analysis conducted this year demonstrates the capacity of supervisory stress testing to test for a wider range of risks and the value of doing so.

As I have stated previously, in current form these stress tests have lost their value and are a regulatory burden. On an existing cost-benefit analysis, they need to be dropped or substantially changed.

Stress tests can provide useful information for macro-prudential regulation, as we are witnessing in the UK where the stress tests extend beyond the perimeter of regulated banking.

For micro-prudential purposes, the rating agency requirements more than suffice.

Operational Risk Modeling is Dead (good)

For operational losses—such as trading losses or litigation expenses—the proposed rules would replace an internal modeled operational risk requirement with a standardized measure. The proposal would approximate a firm's operational risk charge based on the firm's activities, and adjust the charge upward based on a firm's historical operational losses to add risk sensitivity and provide firms with an incentive to mitigate their operational risk.

Operational risk was a mess. While models were prevalent for credit and market risk, the modeling requirement for operational risk was made out of whole cloth. Hopefully the standardized rule will be fairly simple.

The Enhanced Capital Standards Will Apply To Regional Banks

The enhanced capital rules apply to banks and bank holding companies with $100 billion or more in assets.

Unrealized Losses Now Included in Definition of Regulatory Capital

The proposed adjustments would require banks with assets of $100 billion or more to account for unrealized losses and gains in their available-for-sale (AFS) securities when calculating their regulatory capital. This change would improve the transparency of regulatory capital ratios, since it would better reflect banking organizations' actual loss-absorbing capacity.

Inevitable following SVB, but we should understand that this in no panacea.

There are significant asymmetries in the definition of regulatory capital, mostly driven by accounting. For regulatory capital, regulators are now essentially accounting for assets on a mark-to-market basis and the liabilities on an accrual basis.

As interest rates increase, the value of assets will decline, but you will not be able to realize the increase in value of your term liabilities. The regulatory capital measure will now have higher volatility.

Minimum Capital Requirements Will Rise

The proposal's more accurate risk measures as equivalent to requiring the largest banks hold an additional 2 percentage points of capital…

Again, this is the requirement, not the amount of capital.

Wise Technical Changes To G-SIB Surcharge

The proposal would measure on an average basis over the full year the indicators that are currently measured only as of year-end.

The proposal would reduce "cliff effects" in the G-SIB surcharge by measuring G-SIB surcharges in 10-basis point increments instead of the current 50-basis point increments.

The proposal would make improvements to the measurement of some systemic indicators to better align them with risk. These changes would ensure that the G-SIB surcharge better reflects the systemic risk of each G-SIB.

These are all wise and food negate the degree of window dressing that now occurs.

No Changes To Unused Countercyclical Capital Buffer or Supplementary Leverage Ratio

I think the SLR is a good complement to a risk-based capital regime; it controls for when the risk weights are inappropriately low (say as on Aaa CLO tranches in 2007). I doubt the Fed will use the CCB; they certainly could have used it several times already but chose not to.

Long-Term Debt Requirement

A related proposal will be to introduce a long-term debt requirement for all large banks. Long-term debt improves the ability of a bank to be resolved upon failure because the long-term debt can be converted to equity and used to absorb losses. Such a measure would reduce losses borne by the Federal Deposit Insurance Corporation's (FDIC) Deposit Insurance Fund, and provide the FDIC with additional options for restructuring, selling, or winding down a failed bank.

As I stated earlier in framing, this is about reducing the losses to the sovereign, not about reducing the probability of failure.

The banks should be allowed to include unrealized gains from the MTM of their long-term debt in their capital calculations. This would improve the proposal, but I don’t see it mentioned.

But I think the Fed needs to think this through more. As a CFO, with this added requirement, do you increase the size of your balance sheet, and if so with what? Or do you shrink your equity capital, replacing it with LTD and keep the same underlying footings?

That’s A Joke, Son

The international agreement to implement these reforms was finalized more than five years ago, in 2017. Implementing these reforms in a timely way is important, and I am pleased we are beginning that process.

I'd like to emphasize that any changes would not be fully effective for some years because of the notice and comment rulemaking process and any final rule would provide for an appropriate transition.

How Much Would Have Been Saved If TLAC Was In Place For Failed Regionals

Greg Feldberg and Carey Mott wrote an interesting piece The 2023 Banking Crisis: Lessons about Bail-in where they estimated that

The FDIC could have saved $13.6 billion in the recent failures of three large banks if regulators had earlier held the banks to the total loss-absorbing capacity (TLAC) standard, based on reasonable assumptions.

They provide some nice statistics on what has happened this year:

In the cases this year, crucially, the FDIC did impose losses on existing shareholders and creditors of the three banks. That meant total losses for the three banks’ shareholders (about $43 billion, based on separate calculations of the book value and market value at year-end), preferred equity holders ($7.3 billion), and other creditors ($4.7 billion). The total bail-in for shareholders and creditors was therefore about $55 billion

The FDIC’s bank-funded DIF was also depleted by an estimated $31.5 billion. Roughly half, or $15.8 billion, resulted from the FDIC’s exceptional coverage of uninsured depositors in SVB and Signature. The FDIC is obliged to recoup the costs of protecting uninsured depositors through special assessments, which it plans to levy on 113 banks. The remaining half, or $15.7 billion, was a loss borne by the DIF due to the discounts offered to the purchasers of the failed banks (not including any loss-sharing agreements with the buyers of the failed banks) and the estimated losses on the assets the FDIC assumed and will eventually liquidate. With a TLAC requirement there would have been more creditors available to absorb losses, providing a first line of defense for the DIF.

Based on our calculations, these three US banks would have had a combined equity and LTD shortfall of $13.6 billion under these assumptions:

Silicon Valley Bank. At year-end 2022, Silicon Valley Bank (SVB)’s liabilities included enough TLAC-eligible equity and debt instruments to exceed the EU’s minimum 13.5% threshold. However, those instruments were mostly CET1 or preferred stock, and long-term debt made up just 3% of RWAs. To meet that part of the US standards, SVB would have had to raise an additional $1.7 billion in LTD or convert some of its excess capital into LTD.

Signature Bank. At the same point in time, Signature’s TLAC ratio was only 7.1%, substantively all of which was in CET1. To comply with a 13.5% TLAC threshold and a 4.5% LTD threshold, Signature would have had to raise another $3.5 billion in LTD. On the capital side, we assume Signature would set aside enough CET1 to continue its capital distributions. Excluding the CET1 that would have met the capital conservation buffer (2.5% of RWA) would have placed Signature in a TLAC-capital deficit of $2.3 billion. The combined shortfall was $5.8 billion.

First Republic. First Republic had only $779 million in long-term senior notes outstanding, and a TLAC ratio of 9.5% at year-end 2022. To meet our hypothetical requirements, First Republic would have had to raise an additional $6.1 billion in LTD.

Hello Brian

I very much enjoyed your thoughts on Barr’s roadmap for reforming capital requirements of US banks in light of recent events.

The statement “Higher Capital Buffers Reduce the Probability of Failure” has general agreement but, there are severe limitations to the effectiveness of this broad brush regulatory constraint. (And full disclosure I speak as a former regulatory lead on developing such rules) For example, the point of non-viability once reached cannot be turned back by any amount of solvency buffer, no matter how large.

Arguably there is a point of diminishing effectiveness for ever larger broadly measured capital buffers given they are not sufficiently targeted to the sources of problems/threats to bank viability (e.g. cumulative effects of bad credit underwriting or reckless maturity transformation). Perhaps this is why in Canada we chose to directly address the risk to the banking system of over leverage in residential mortgage markets by directly addressing minimum standards for the quality of underwriting what is a commoditized product, and lately, returned to specific capital charges on residential mortgages that are negatively amortizing (https://www.osfi-bsif.gc.ca/Eng/fi-if/in-ai/Pages/20230711-let.aspx) rather than relying solely on broad based capital “buffers”.

Finally, while I concur with your assessment of the origins and “calibration” of the operational risk charge, perhaps this too is one risk where applying a capital charge that is essentially a “plug” ought to have a more constrained expert judgement score card instead. Perhaps an examination process that dings those banks who seem to have trouble running with scissors with legally binding orders on remediating the management failures specifically identified as the problem would yield better outcomes?

From one “retired” bank regulator to another, keep up the good work in your sub stack commentary. I look forward to reading them!

Respectfully,

Richard Gresser,

Ottawa Canada