Perspective on Risk - Dec 13, 2023

Is This Time Unique? US Regulators Clamp Down; Model Validation; Barr on Liquidity Management; NY Fed's Cultural Reform Podcast; More Stuff ...

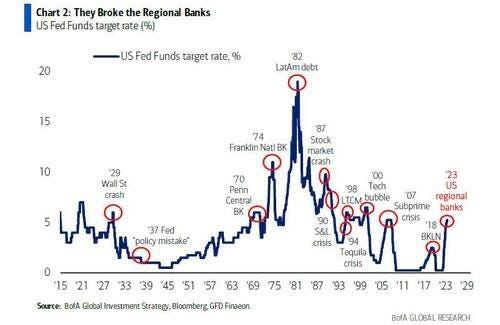

Is This Time Unique?

Every Fed rate hiking cycle continues until something significant breaks.

If the only thing that breaks this time is SVB, Signature and First Republic, we should consider ourselves lucky.

US Regulators Clamp Down

US regulators clamp down in bid to prevent more bank failures (Reuters)

Actually, nothing should be surprising here.

Interviews with a dozen industry executives, lawyers and regulatory officials show examiners are executing surprise reviews of a key confidential supervisory bank health rating and in some cases have issued downgrades. They are increasingly warning big banks they will be placed under an order restricting a range of activities if they don't fix lapses; and are pressing top executives to take personal accountability for addressing the banks' problems.

The FDIC and other regulators wrote in recent months to regional and community banks in a number of states notifying them they had launched surprise reviews of their "CAMELS" rating, five of the people said.

Reasons regulators cited for downgrades included insufficient capital, management issues, and in many cases, exposure to commercial real estate, a sector struggling amid high rates and lingering office vacancies, the people said.

One of the problems highlighted by the SVB, Signature, First Republic failures was the disconnect between the off-site monitoring functions at the regulatory agencies and the onsite teams evaluation and transmission of changes to the financial risk components of the various ratings.

I’ll go one step further and argue that there is no advantage, and perhaps even a disadvantage, of having the dispersed onsite teams rating the financial strength of the organizations. Dispassionate peer-based analysis can do a much better job. So can models and algorithms.

Supervisors are also pressing big bank bosses to take more personal accountability for problems, in some cases seeking briefings with C-suite executives or board members to secure assurances that they are personally on top of the problems, two of the people said.

This they should have been doing all along - I know we did.

Model Validation

…is hard, but needs to be done rigorously by qualified staff. Here is another paper in the ongoing factor replication crisis that is underway.

A Grad-School Number-Cruncher Shakes Up the World of Bond Quants (Bloomberg)

While working on his degree at Warwick Business School in England in 2021, he tried to understand established thinking about bonds by replicating the field’s seminal research. But he found he couldn’t do that with an influential paper by three Georgetown University professors.

The paper in question was from the Journal of Financial Economics: RETRACTED: Common risk factors in the cross-section of corporate bond returns

This paper:

got the calendar wrong. In the case of two factors, there was a lead error, meaning the authors gave the returns of, say, February as the returns of January. For the third factor, there was the opposite problem of a lag error.

removed the most extreme losses for some bonds, making the factors look less volatile than they were.

Here is the rebuttal paper in full: Priced risk in corporate bonds. Such polite economist language for such a smack-down.

Recent studies document strong empirical support for multifactor models that aim to explain the cross-sectional variation in corporate bond expected excess returns. We revisit these findings and provide evidence that common factor pricing in corporate bonds is exceedingly difficult to establish. Based on portfolio- and bond-level analyses, we demonstrate that previously proposed bond risk factors, with traded liquidity as the only marginal exception, do not have any incremental explanatory power over the corporate bond market factor. Consequently, this implies that the bond CAPM is not dominated by either traded- or nontraded-factor models in pairwise and multiple model comparison tests.

Barr Speech on Liquidity Management

Again, for the most part, I’m trying not to rehash every Fed Gov speech. But The Importance of Effective Liquidity Risk Management is worth touching on briefly if only to give you topics to talk over with your Treasury department. Send it to them and ask them for a self-assessment.

Barr expounds on some of the lessons they’ve uncovered, likely through their horizontal review. He highlights signaling, operational and

It may be difficult for a firm to conduct significant asset sales in a short time frame without becoming the subject of adverse attention

We also saw during this period that firms were not as well positioned to monetize (that is, to borrow against or be ready to sell) their assets as they should have been. … The March stress episode, however, highlighted the fact that, in practice, there can be operational impediments to a bank's ability to monetize its liquidity buffers in large volumes and in a rapid time frame in acute stress.

The March stress underlined the possibility that private repo markets may not be a viable financing channel for banks that need to rapidly ramp up access, especially for banks that may not regularly transact in these markets, even if such repo markets can be a viable source of liquidity for banks that regularly tap such markets and have more gradual funding stresses. Sharp shifts in calls on private repo market capacity, particularly by firms experiencing stress, may not be easily met.

[Banks] faced internal operational challenges in quickly identifying and moving collateral that would have provided them additional borrowing capacity at the discount window. … There are two key aspects of discount window readiness: preparedness to access the discount window and prepositioning adequate amounts of collateral. … many of these banks had not recently tested their discount window access prior to the stress event … In the case of some banks, the amount of collateral prepositioned was also a tiny fraction of potentially flight-prone liabilities going into the stress event. This lack of pre-pledging is a concern for several reasons, including that certain collateral types can require more time to pledge. Less liquid collateral can take longer to be assessed and valued at the discount window, meaning that banks should not expect they can gain immediate liquidity against these assets.

He also continues the never-ending effort to destigmatize borrowing from the Discount Window. Not sure this will happen.

Cultural Reform Podcast

Must have missed this one. Toni Dechario of the NY Fed has five interesting podcast interviews of culture at Podcast: Bank Notes. Here is the Spotify link if you’d prefer to access this way. There are also transcripts for each interview if you click on the little blue circles below each podcast.

These are excellent training tools for your staff. I particularly liked:

Success Through Failure: The PreMortem Method

[Gary Klein] is well-known for creating the PreMortem Method of Risk Assessment, a risk management exercise that helps project team members imagine potential problems upfront, rather than examining shortfalls in hindsight. This episode digs into the how and why of Klein’s premortem practice, what differentiates it from other strategic tools, and the challenges of integrating a culture of curiosity into established ways of working.

How to Fix What’s Not (Yet) Broken

Michael Hallsworth and Scott Young of the Behavioural Insights Team discuss why it is important for organizations to examine their operational frameworks and systems, in order to better assess how established processes and environments may be impacting the work of their employees. They also share recommendations for reducing the overconfidence bias, overcoming entrenched ways of thinking, and fostering a culture of transparency.

Please check out the rest as well.

More On …

More links to stuff discussed in the past.

Argentina

The OddLots folks interview Brad Setser (Spotify, no transcript currently available)

Regulator Oversight of Compensation

Top ECB official wants to give risk managers more power on bank bonuses (FT)

Official is former NYDFS Sup. McCaul

Crowded Trades (Watched Pot Never Boils Alert)

Citadel and Its Peers Are Piling Into the Same Trades.

The Bank of England is still v v worried about Treasury basis trades (FT)

Nickle Fraud

Trafigura Staff Tried to Hide Nickel ‘Red Flags,’ Gupta Says

Staff at Trafigura Group worked with alleged fraudster Prateek Gupta to ensure that their dealings would not raise the suspicion of key lender Citigroup Inc., according to messages made public in the court battle between the two sides.

Passive Investing

Passive Investing and Market Quality

BPI Recommendations To Enhance Fed’s Sup & Reg Report

The information on supervisory ratings in these reports should be standardized and expanded to facilitate better understanding of trends and drivers.

The report should include a breakdown of supervisory priorities on a supervisory program level – e.g., breaking out (large and foreign banking organizations) LFBO as compared to (Large Institution Supervision Coordinating Committee) LISCC priorities.

The detailed breakdown of supervisory findings that this report provided for CBOs and RBOs should also be provided for the larger bank categories

… the report … does not specify the report’s “as of” date as a general matter.

… the report should include greater disclosure on where and how the examiner workforce is being assigned.

The report … should include more detailed supervisory observations and findings (“lessons learned”) gleaned from the most recent standing and ad hoc horizontal examinations.