Perspective on Risk - Dec. 1, 2022 (Grab-bag)

Supply Shocks; Housing; What Happens in China ; Pyramid of Ponzi; Celsius Bankruptcy; Burning Crypto To Its Roots; Nepotism & Risk Mgt.; Ethics & FOMC; Models & Algos; Unintended Consequences; More

This post is a grab-bag of updates. I’m also going to be sending a self-scouting report on topics I’ve covered over the last year: that one will be useful for newer subscribers as it summarizes some of the working hypothesis.

How to Handle Supply Shocks

In the past, associated with discussions of Zoltan Poszar’s work as well as inflation and slowing global growth, we discussed that ‘economic risk’ was shifting from a world dominated by demand shocks to a world more affected by supply shocks. Traditionally, the Fed has been in the position to address decreases to aggregate demand through monetary policy; it seems to have less tools available to address supply shocks.

With that in mind, I want to call attention to a recent Fed speech by Gov. Lael Brainard What Can We Learn from the Pandemic and the War about Supply Shocks, Inflation, and Monetary Policy? The essential question being asked is “When can you look through supply shocks?” The answer is when they are transient and unlinked. But in serial sequence, idiosyncratic supply shocks cumulate to become a more persistent effect.

After several decades in which supply was highly elastic and inflation was low and relatively stable, a series of supply shocks associated with the pandemic and Russia's war against Ukraine … highlights the challenges for monetary policy in responding to a protracted series of adverse supply shocks. In addition, to the extent that the lower elasticity of supply we have seen recently could become more common due to challenges such as demographics, deglobalization, and climate change, it could herald a shift to an environment characterized by more volatile inflation compared with the preceding few decades.

The standard monetary policy prescription is to "look through" supply shocks … that are not assessed to leave a lasting imprint on potential output. In contrast, if supply shocks durably lower potential output such that the economy is operating above potential, monetary policy tightening is necessary to bring demand into alignment with the economy's reduced productive capacity.

[T]he drawn-out sequence of shocks … blurred the lines about what constitutes a temporary shock as opposed to a persistent shock to potential output. Even when each individual supply shock fades over time and behaves like a temporary shock on its own, a drawn-out sequence of adverse supply shocks … is likely to call for monetary policy tightening to restore balance between demand and supply.

The supply disruptions in key goods and commodities sectors associated with the pandemic and Russia's war against Ukraine have highlighted the fragility of global supply chains and the risks of inelastic supply at moments of stress. … [O]ngoing discussions about moving from "just in time" to "just in case" inventory management and from offshoring to "nearshoring" are raising important questions about the extent to which businesses are likely to reconfigure global supply chains...

To conclude, … [a] protracted series of adverse supply shocks could persistently weigh on potential output or could risk pushing inflation expectations above target in ways that call for monetary policy to tighten for risk-management reasons. More speculatively, it is possible that longer-term changes—such as those associated with labor supply, deglobalization, and climate change—could reduce the elasticity of supply and increase inflation volatility into the future.

More on Housing

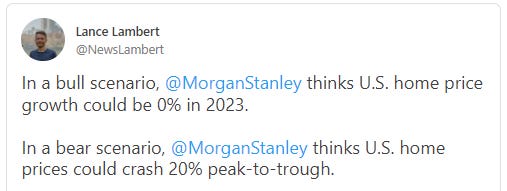

I came across @NewsLambert (covers housing for Fortune) who wrote up the U.S. Housing market forecasts from Morgan Stanley.

Based upon this graph that he shares, the ‘market’ remains 9% over trend value at the end of 2023 after an apx. 5% decrease in the 2nd half of 2022 (based on Case-Shiller metric).

@mikesimonsen of Altos provides useful information on the housing market. He notes that inventory for sale has slowed (while still at a low level historically).

Properties with price reduction has plateaued.

And the median price of new listings is still elevated and showing somewhat normal cyclical patters,

One last note: as much as anything, we have a supply issue. Low supply increases affordability, increases median rents, and drives the increase in homelessness. We need supply side policies to mitigate this issue.

Update:

Fed Chair Powell just dropped this informative graph

What Happens in China Does Not Stay in China

I found this paper by four Fed economists, What Happens in China Does Not Stay in China (Board of Governors of Federal Reserve System), interesting. The paper quantifies the extent of the growth of China’s growing source of final demand on global finance.

In this paper, however, we provide evidence that China constitutes an important driver of the global financial cycle. We argue that because of China's importance for global consumption, stronger Chinese growth raises global growth prospects, inducing an increase in global risk sentiment and an expansion in global asset prices and global credit.

We construct a measure of China's credit impulse to identify Chinese policy-induced demand shocks. … Then [w]e estimate an alternative measure of Chinese GDP growth that captures its business cycle given data concerns about the smoothness of official GDP data.

Their goal is …

To the best of our knowledge, this is the first paper that formally shows that China’s credit policies are an important driver of the global financial cycle.

We argue that its influence reverberates through the global financial system through its impact on global growth given China’s importance in global consumption.

We estimate that a policy-induced increase in China’s credit impulse of 1% of GDP boosts its own economy by 1.2%. After one to two years, the credit shock is estimated to induce a 0.3% increase in global GDP outside of China and raise commodity prices and global trade excluding China by 2.2% and 1%, respectively, boosted by stronger Chinese demand. … [T]he effects of a policy-induced Chinese credit expansion of 1% of GDP on

global credit are about half the size of a 25 basis points reduction in the federal funds rate

[W]e find that China’s economy has significant spillovers to global GDP and not just EMEs, boosted by stronger Chinese demand.

A ‘Pyramid of Ponzi’

The above has been my go-to phrase when describing the implosion of the crypto *industry*. Sometimes I add ‘with a side of pump-n-dump fraud.’ As such, I loved to see this tweet (recommended reading) from @Frances_Coppola:

Celsius Bankruptcy Report

Really, if you want to follow the implosion, just follow Matt Levine. He’s doing a great job. Or if you like podcasts, here he is on Oddlots (Spotify link) explaining FTX and Alemeda. Anyway:

On Saturday, Celsius’ bankruptcy examiner filed a report about what it did with customer money.

As he puts it,

The report is fascinating in its boring details.

One thing that I say a lot around here is that crypto is engaged in re-learning the lessons of traditional finance. … But I want to say here that one lesson crypto is relearning is about the value of having a good accounting system for keeping track of where the money is.

Folks interested in Op Risk will find lots of examples for future instruction.

Regulation sort of did its job.

Intense regulatory pressure forced Celsius to change its business model. … On September 17, 2021, the New Jersey Bureau of Securities ordered Celsius to cease and desist from offering the Earn product to unaccredited investors and from accepting any additional assets into an existing Earn account.

In response, Celsius developed a “Custody” program for its unaccredited U.S. customers, which it launched on April 15, 2022, to meet New Jersey’s deadline for compliance. The Custody program allowed existing customers to continue to receive rewards for their existing Earn accounts but required them to make all future deposits into a Custody account. Crypto assets in a Custody account were not eligible for rewards, and under a new Terms of Use, title remained with the customer; Celsius stated that it would “not transfer, sell, loan or otherwise rehypothecate” those Custody assets.

Unfortunately,

Due to time pressure and lack of engineering resources, Celsius chose to rely on manual reconciliations and transfers of crypto assets without robust controls for the Custody program, with aspirations of developing a more effective process later. This same time pressure left Celsius without a viable solution for unaccredited investor customers residing in nine states in which Celsius did not have the proper licenses to offer a Custody program.

To fund Custody accounts, Celsius moved crypto assets out of its commingled Main wallets into separate wallets designated for the Custody accounts. Because the crypto assets in the Custody wallets all arrived in aggregate transfers from Celsius’s commingled Main wallets, Celsius did not treat any particular asset in the Custody wallets as belonging to any particular customer. And due to the decision not to develop a separate Custody infrastructure, when customers transferred new crypto assets into a Custody account, the crypto assets were deposited in the same manner as they had been under the Earn program.

The examiner concludes:

This investigation revealed that Celsius reacted to the regulatory scrutiny by launching its Custody program without sufficient accounting and operational controls or technical infrastructure. The Custody accounts did not regularly reconcile with assets held in the Custody wallets; shortfalls in the Custody wallets were funded by the Main wallets, where Earn deposits and other crypto assets were held; and no effort was made to segregate or separately identify any assets associated with the Withhold accounts, which were commingled in the Main wallets.

Burning Crypto To Its Roots

Here are some of the real-world linkages of the crypto implosion.

Crypto Lenders’ Woes Worsen as Bitcoin Miners Struggle to Repay Debt (Bloomberg)

Miners, who raised as much as $4 billion from mining-equipment financing when profit margins were as high as 90%, are defaulting on loans and sending hundreds of thousands of machines that served as collateral back to lenders. New York Digital Investment Group, Celsius Network, BlockFi Inc., Galaxy Digital, and the Foundry unit of Digital Currency Group were among the biggest providers of funding to finance computer equipment and build data centers.

Lenders are already looking at a glut of machines after liquidating rig-backed loans from miners.

Chip Maker Nvidia Issues Tepid Earnings Forecast as Videogaming Business Slows (WSJ)

Graphics chip maker Nvidia Corp. … reported a sharp decline in quarterly sales, driven by waning consumer demand for its videogaming chips … and the onset of the cryptowinter.

From the 8-K:

Volatility in the cryptocurrency market – such as the recent declines in cryptocurrency prices or changes in method of verifying transactions, including proof of work or proof of stake – can impact demand for our products and our ability to accurately estimate it.

OEM and Other revenue was down 52% from a year ago and down 18% sequentially. The year-on-year decrease was due to a decline in Cryptocurrency Mining Processor (CMP) revenue, which was nominal in the quarter compared with $155 million from a year ago.

Nepotism Doesn’t Make For Sound Risk Management

Without going into details, Silvergate Bank is tied up in the whole FTX fraud. @ashwinibrila pointed out this little gem from Silvergate:

Ethics & the FOMC

I’ve stated in the past that XXX, XXX and XXX should all step down because of their failures to comply with trading restrictions. It is with humor and chagrin that I read this in the FOMC minutes:

No real consequences for the powerful. Doesn’t set the example of leadership that we should expect.

Models & Algorithms

Neural stonks predictions (FT)

From JPMorgan’s long-term strategy group led by Jan Loeys:

We construct a neural network model based on fundamentals to forecast 10-year out returns on the S&P 500.

The model makes no assumptions about the future and is based solely upon currently observable fundamentals. …

The model forecasts an SPX return of 8.0% pa in the coming 10 years. This forecast comes with a one-sigma risk of ~1.5%, implying a 2/3 probability of a return between 6.5% and 9.5% pa.

As the FT notes, seems a lot of spurious sophistication to arrive at a result pretty close to the long-term returns.

Anyway, if anyone has access to the paper, please shoot me a copy.

Unintended Consequences

Highway signs showing traffic deaths don’t reduce crashes (Science)

In the past decade, at least 28 U.S. states have started to display traffic fatality numbers to scare motorists into safer driving. But a new analysis of Texas car crashes co-authored by Madsen suggests such signs may actually be associated with more crashes, not fewer.

The analysis of 844,939 accidents showed that in the 10 kilometers downroad of the signs, crashes increased by 1.35% when the numbers were displayed, the researchers report today in Science. Madsen and Hall propose that the fatality stats are so in your face that they grab too much of the driver’s attention, causing a crash. The data support this explanation, they say: Crashes increased when the death numbers displayed on the signs were higher.

Podcasts

Eugene Fama: A Life in Finance (Spotify link)

In today’s episode, [Meb Faber talks] to Professor Fama about whether he thinks the Fed can control inflation, where the phrase efficient markets came from, and his take on the global market portfolio. As we wind down, we hear the last time he bought an individual stock.

Stuff To Read

The difference between a snafu, a shitshow, and a clusterfuck (Quartz)

To appreciate what a clusterfuck is—and to understand how to avoid one—it is first helpful to clarify some of the things a clusterfuck is not:

A fuck-up. “A fuck-up is just something all of us do every day,” Sutton says. “I broke the egg I made for breakfast this morning. That was kind of a fuck-up.” Whereas clusterfucks are perfectly preventable, fuck-ups are an unavoidable feature of the human condition.

A SNAFU. While sometimes used as a synonym for minor malfunctions and hiccups, this slang military acronym—“Situation Normal, All Fucked Up”—actually refers to the functionally messy state that describes many otherwise healthy companies (and many of our personal lives). A SNAFU work environment is usually manageable; one that is FUBAR (Fucked Up Beyond All Repair, another military legacy) probably isn’t. “When my students with little experience go to work at a famous company and it isn’t quite as they dreamed, I do ask them if it is FUBAR or SNAFU, and tell them SNAFU will describe most places they work,” Sutton said.

A shitshow. No less an authority than the Oxford English Dictionary describes a shitshow as a “situation or state of affairs characterized by chaos, confusion, or incompetence.” A clusterfuck may come to possess all those characteristics, but is more properly identified by the decisions that produced it than its outcome.

Nobody Planned This, Nobody Expected It (Morgan Housel on CollabFund)

The Battle of Stalingrad was the largest battle in history. With it came equally superlative stories of how people dealt with risk.

The Germans had the most sophisticated equipment in the world. Yet there they were, defeated by mice.

On bullshit in investing (Benn Eifert on the Noahopinion substack)

The investing industry is ridden with bullshit. The most common and insidious form is over-optimism: offers of tantalizing risk/reward that defy any notion of reality, often based on misinformation or deception. Less common but even more dangerous are outright frauds.

Tweets I Liked Purely For The Snark Value