Perspective on Risk - April 3, 2025 (Something Other Than Tariffs)

Demographics; Globalization/Geopolitics; Global Warming

Demographics

I haven’t really focused on demographics in a while, and there are several new pieces out.

Aging Will Hit China’s Economy Far Harder Than Is Recognized (CFR)

Ageing cost projections – new evidence from the 2024 Ageing Report (ECB)

Decomposing Effects of Population Aging on Economic Growth in OECD Countries (Lee and Shin; MIT)

Global Demographic Shifts: Population Aging and Decline (Policy Horizons Canada)

Dependency and depopulation? (McKinsey Global)

Rather than review each separately, I will attempt to synthesize their conclusions.

Demographics Shifting From Tailwind To Headwind

For decades, demographic trends have been a positive force for economic growth in developed economies. But this tailwind is rapidly becoming a headwind. This shift is fundamentally altering economic growth prospects, consumption patterns, labor markets.

According to the McKinsey Global Institute (MGI), two-thirds of humanity now lives in countries with fertility below the replacement rate of 2.1 children per woman—the level needed to maintain population stability.

Falling fertility rates explain about 80 percent of the changes in today's total population resulting from the demographic shift sweeping the world.

The fertility collapse has been most dramatic in emerging economies: Brazil's fertility rate plummeted from 6.1 babies per woman in 1960 to just 1.6 today. India's fertility rate dropped below replacement level in 2019. China's fertility rate is now among the world's lowest at 1.1 children per woman. The UN projects that total global population will peak at just above 10 billion around 2084 before beginning to decline.

The first wave regions (advanced economies and China) have already reached peak working-age population. China's share of global population, currently the second largest at 18%, is projected to shrink to just 6% by 2100—making China's population only 170 million larger than North America's (compared to a difference of roughly one billion people today).

Emerging Asia, India, Latin America, Middle East/North Africa will begin to peak in the 2030s, earlier than I had guessed. Sub-Saharan Africa will not peak until later in the century.

Deteriorating Support Ratios

Perhaps the most important demographic metric for economic outcomes is the support ratio—the number of working-age people (15-64 years) relative to each person 65 and older. This ratio indicates how many potential workers are available to support each elderly person through direct care, tax payments, or economic production.

Globally, the support ratio was 9.4 in 1997... By 2050, the support ratio is expected to fall to 3.9—that is, fewer than four people will need to support each senior.

The first wave regions have already reached peak working-age population in percentage terms. Their working-age population share has dropped from a peak of 70% in 2010 to 67% today and is projected to fall to just 59% by 2050. Greater China, and Western Europe will face the lowest support ratios by 2050, with Greater China experiencing the fastest decline.

Even fast growing India, currently the world's largest population, will see its support ratio fall from 9.8 today to roughly half that by 2050, eventually dropping to 1.9—about the same as Japan today—by 2100.

… Leads To Slower Growth

GDP per capita growth depends on two key factors: productivity growth (output per hour worked) and the total hours worked per capita. Demographics primarily affects the latter through changing the share of the population that is working-age (the age mix) and their labor intensity (how much each person works).

Demographic headwinds will be a drag on hours per capita... equivalent to a cumulative reduction in hours per capita per week of 2.2 hours across first wave economies from 2023 to 2050

According to the CFR:

Aging reduces the labor force participation rate, which in turn dampens GDP growth. But aging also drags down growth further through a second channel—one which is not widely recognized: that is, it pulls down labor force productivity. …

Whereas aging will result in per capita U.S. GDP growth 6 percent lower than it would be without aging, it will knock a much larger 10 percent off China’s per capita growth. The gap owes mainly to China’s much lower birth rate and immigration flows.

Research cited in Lee & Shin's paper) confirms these findings, showing that "the impact of aging directly on economic growth, the labor force and productivity" reduces growth by approximately 0.4% annually in the United States.

The demographic drag extends beyond just hours worked—it also appears to negatively impact productivity growth, particularly total factor productivity (TFP). Lee & Shin's analysis of OECD countries finds that:

Lowered TFP growth associated with aging explains more than fully the lowered growth rate of GDP per capita.

McKinsey calculates that most first wave countries would need to increase productivity growth by two to four times their historical rates to maintain past GDP per capita growth in the face of demographic headwinds.

China faces a particularly acute demographic challenge. The country is aging at an unprecedented pace, with the share of its population aged 60 and older projected to rise from about 20% today to over 40% by 2050—higher than the United States and comparable to Japan's aging trajectory. To achieve its 4.9% growth target (already reduced from historical rates), McKinsey calculates that China would need to grow productivity by 5.5% annually through 2050

McKinsey notes that the demographic dividend that fueled East Asian economic miracles is disappearing:

In India... the dividend added 0.7 percentage point each year on average to the country's GDP per capita growth, but as the age mix skews older, it will contribute only 0.2 percent annually on average to Indian incomes to 2050.

… Challenges Government Finances

The most immediate impact of demographic aging is on government finances, particularly in countries with generous welfare states and pay-as-you-go pension systems. The fiscal math becomes increasingly difficult as support ratios decline.

Time spent in retirement has increased substantially—from 11 to 18 years on average since 1970 according to the OECD. In the United States, the Social Security trust fund could be depleted by 2034, potentially leading to a 25% reduction in benefits without structural reforms.

These fiscal pressures come at a time when many advanced economies already face high debt levels. France, Italy, Japan, Spain, the United Kingdom, and the United States, already have public debts exceeding 100% of annual GDP.

… Changes Consumption Patterns

I was surprised to learn that seniors already consume more per capita than younger cohorts in most advanced countries. In 2023, those 65 and older consumed 16% more per capita in direct consumption than average in both Western Europe and Japan. If you include “in-kind consumption,” such as government-funded healthcare, seniors consumed 22-24% more per capita.

If 2023 spending patterns are maintained, the share of consumption by those 65 years and older in first wave regions will rise from 21 to 31 percent [by 2050]

Healthcare will increase the most, rising between 5% and 29% due to age mix changes alone across China, Germany, Japan, and the United States. Education spending could fall by 4% to 33% per capita due to fewer young people.

… Has Profound Implications For Savings & Investment

As Policy Horizons Canada notes:

Older populations tend to have more savers and fewer borrowers, which can translate into lower interest rates and higher asset prices.

This dynamic has already played out in many advanced economies, where asset appreciation—particularly in housing—has helped current retirees fund their consumption. Home equity has been a crucial source of retirement security, as housing costs (including imputed rent) represent about 40% of total consumption among seniors.

If populations shrink significantly, housing demand may eventually fall, potentially undermining a key source of retirement security. Japan offers a cautionary tale, with stagnant or falling real estate prices in many areas as its population has declined.

The demographic shift toward older populations has several implications for financial markets.

Higher saving rates among aging populations, combined with reduced investment demand due to slower economic growth, have put downward pressure on real interest rates. This pattern has been evident across advanced economies over the past two decades. The ECB's 2024 Ageing Report notes that:

“demographics, leading to a greater proportion of elderly citizens and increased demand for pensions, health care, and long-term care services, will strain public finances," potentially keeping rates lower due to higher savings rates.

Evidence suggests aging populations may demand a higher risk premium for equities, potentially leading to lower price-to-earnings ratios as risk aversion increases. This could partially counteract the effect of lower interest rates on equity valuations.

… Shifts Global Capital Flows

Demographics will fundamentally reshape global capital flows in coming decades. As first wave regions age rapidly, capital will increasingly seek higher returns in younger economies with more favorable demographic profiles.

Policy Horizons Canada explicitly identifies this shift:

"Capital flows: Slowing growth in some aging Asian countries could see global capital flows redirected to emerging economies with higher growth rates. This may be likely in Southeast or South Asia in the short to medium term, and Africa in the longer term. In time, such changes could help revise global patterns of trade and power."

McKinsey's analysis quantifies the magnitude of this opportunity. By 2050, later wave regions would account for over two-thirds of all hours worked globally, with Sub-Saharan Africa alone accounting for 18% of global work hours—double its current share. Meanwhile, China's contribution could fall from 26% today to 18% by 2050.

This creates profound investment implications. As MGI notes:

"Consumption pools are shifting from North America and Western Europe to Emerging Asia and India... For example, World Data Lab projects that India and Emerging Asia will account for 30 percent of global consumption at purchasing-power parity (PPP), up from 12 percent in 1997."

For investors, this geographic reallocation represents both challenge and opportunity. The evidence from Lee and Shin suggests that:

"If productivity levels remained constant, forecast shifts in hours toward lower productivity regions could reduce global productivity growth by 0.5% per year."

However, this productivity gap creates substantial opportunity for capital to flow toward regions with:

Growing labor forces (increasing the marginal product of capital)

Young populations with high consumption growth

Potentially higher returns due to economic catch-up

McKinsey suggests these flows could accelerate "catch-up growth" in these regions, potentially aiding their transition to higher income levels before their own demographic transitions intensify. However, it also cautions that "navigating as a business may become more complex, as many later wave countries have more challenging legal and governance environments."

The demographic transition in advanced economies has been linked to the "global savings glut" and "secular stagnation" thesis articulated by Ben Bernanke and Larry Summers. The CFR's Ageing Report provides evidence of this connection:

Population aging is also projected to have a detrimental impact on public finances in the period to 2070 by lowering potential output growth. The 2024 Ageing Report projects euro area potential output growth to decrease from the average level of 1.4% estimated for this year and the last two years, to stand at 0.8% in the early 2030s, as labour input growth turns negative."

As populations age in advanced economies, savings rates tend to remain elevated while investment demand weakens due to slower labor force growth. This excess saving seeks returns globally, potentially flowing to regions with more favorable demographics and higher returns.

China's demographic transition will have particularly significant implications for global capital flows. As China's exceptional economic growth moderates due in part to demographic headwinds, its role as both a destination for and source of global capital will evolve. As its population ages and growth slows, Chinese savings could increasingly flow outward in search of higher returns in younger economies, particularly across Asia and Africa. Concurrently, China's attractiveness as a destination for foreign investment may diminish relative to younger emerging markets.

Lee and Shin notes that

if productivity levels remained constant, forecast shifts in hours toward lower productivity regions could reduce global productivity growth by 0.5% per year.

This creates opportunities for capital to flow toward these regions to help close the productivity gap.

An intriguing dimension mentioned by Policy Horizons Canada is the potential for "out-migration from industrialized countries":

High costs of living and growing stress on healthcare systems may lead more older people from developed countries to migrate to countries where they have greater buying power. This would help mitigate the stress on systems in the developed world, while increasing demand for services in the destination countries.

Portugal, Costa Rica and Morocco are looking more appealing by the day.

… And Labor Markets

By 2050, older workers will contribute a higher proportion than today. When looking at workers 50 and older:

Their share will climb to 37 percent on average by 2050, up from 32 percent today and 17 percent in 1997.

In China, workers aged 50 and older will account for 39 of every 100 hours worked by 2050, up from 31 in 2023. In Germany, they could account for 42% rather than 35% of hours worked by 2050.

Japan offers a preview of these adaptations, with substantially higher labor force participation among older adults than other developed economies. The labor force participation rate among Japanese aged 50-65 years is 84%, up from 73% in 1997, and among those 65 and older, it's 26%—compared to 19% in the United States and just 4% in France.

Labor markets are also seeing increased competition for migrant workers globally as populations age. Policy Horizons Canada observes:

Countries accustomed to picking and choosing among many would-be immigrants may have to compete more vigorously to attract a shrinking pool of highly valued immigrant workers.

Conclussion

… the current calculus of economies cannot support existing income and retirement norms—something must give - McKinsey Global Institute

Globalization/Geopolitics

Three Views

Here are three interesting articles that examine the changing dynamics of the global economic order, particularly the shift away from the post-Cold War paradigm of liberal globalization, but they approach this transformation from different angles and with different conclusions.

The first two, by Froman and Toose, assert that the old economic paradigm - characterized by free trade, market liberalization, and global integration - is breaking down. Both highlight the return of state-directed economic strategies. And both express doubt about the effectiveness of limited industrial policies.

Where they differ is that Froman's thesis is that China has "won" by establishing its economic model as the de facto standard, with the US imitating Chinese policies, whereas Tooze emphasizes that no coherent new paradigm has replaced the old one, leading to "pervasive cognitive dissonance."

Froman concentrates on trade and investment policies (tariffs, investment restrictions), while Tooze emphasizes the disconnect between these and fundamental macroeconomic realities (fiscal policy, monetary policy, exchange rates).

The third is a paper by Brad Setser. The Setser paper provides an important counterpoint to the narratives presented in the Froman and Tooze articles. Setser directly contradicts Froman's framing that China has “won.”

Where Froman sees Chinese economic practices as having conquered the global system, Setser portrays China's export surge as stemming from unhealthy internal imbalances.

Where Tooze describes a situation where "the old is dying and the new cannot be born," while Setser suggests the old system of global trade integration remains surprisingly robust.

Setser introduces the concept that some forms of globalization are unhealthy (like tax-avoidance-driven investment flows) while others are beneficial, adding nuance that neither Froman nor Tooze fully explore.

China Has Already Remade The International System (Froman - Foreign Policy)

Whether or not the United States can compete with China on China’s playing field …the United States is now operating largely in accordance with Beijing’s standards

An interesting article by the current president of the Council on Foreign Relations and Obama’s U.S. Trade Representative.

… the U.S. strategy of engagement with China was based on the premise that, if the United States incorporated China into the global rules-based system, China would become more like the United States. … the expectation was that integration would facilitate convergence.

Instead of China coming to resemble the United States, the United States is behaving more like China. Washington may have forged the open, liberal rules-based order, but China has defined its next phase: protectionism, subsidization, restrictions on foreign investment, and industrial policy.

Washington, having failed to convince Beijing to change its predatory economic policies or to move forward with an alternative trading bloc to counterbalance China, was left with one option: the United States had to become more like China.

President Joe Biden maintained … and added tariffs on other Chinese products … and …Trump has imposed an additional 20 percent tari on all U.S. imports from China …

Whether or not the United States can compete with China on China’s playing field, it is important to recognize a fundamental truth: the United States is now operating largely in accordance with Beijing’s standards, with a new economic model characterized by protectionism, constraints on foreign investment, subsidies, and industrial policy—essentially nationalist state capitalism. In the war over who gets to define the rules of the road, the battle is over, at least for now. And China won.

The old US economic policy is dying and the new cannot be born (Toose - FT)

The coherence of economic policy in the heyday of globalisation can be overstated. But today’s dissonance between industrial and macroeconomic policy is new and intense. It forms an anti-paradigm that adds materially to the uncertainty haunting the world economy.

It is a commonplace that in recent years the paradigm of globalisation has come apart. There is no longer a presumption of ever closer global integration. The politics of trade are superheated. National industrial policy is all the rage. But the evidence for major changes in the flow of trade is scant. What has replaced the old paradigm is less a coherent new agenda than pervasive cognitive dissonance.

The pressure of global competition falls heavily on America’s traded goods sectors, notably manufacturing. That isn’t a bug. It’s a feature of what was once an elite consensus favouring market access and trade liberalisation underpinned by the widely felt benefits of cheap imports. That consensus broke down in 2016 when Donald Trump won the rustbelt states. Since then populist protectionism, promises of re-industrialisation and finger-pointing at China have framed US policy.

If your aim is restoring the competitive position of US industry, a large dollar devaluation would do more than a sprinkling of industrial subsidies. But how to engineer one in the face of global demand for US financial assets is anyone’s guess. There is discussion of a tariff on foreign capital inflows, in effect a tax on the dollar as a reserve currency. But for such a radical policy to see the light of day would require producer interests to dethrone Wall Street — nothing short of a revolution. Meanwhile, fiscal consolidation, the solution to the “twin deficit” problem adopted by the Clinton administration in the 1990s, is ruled out by deadlock in Congress.

The Surprising Resilience of Globalization: An Examination of Claims of Economic Fragmentation (Setzer for Economic Strategy Group)

The immediate risk facing the global economy is perhaps better described as unhealthy integration than fragmentation.

The now-standard tale of deglobalization certainly contains a kernel of truth. Policies meant to accelerate economic integration across borders no longer command a clear political majority, certainly not in the United States.

Global trade continues to rise alongside global economic growth. If anything, trade has picked up since the pandemic. Widespread expectations that the global economy would fragment into rival blocks have not yet come to pass.

We should make no across-the-board assumption that higher levels of globalization necessarily reflect more perfect markets and/or the elimination of arbitrary restrictions on cross-border flows. Rather, certain forms of integration stem from distorted incentives, and thus a fall in measured integration can be a sign of a healthier and more balanced global economy.

China's own domestic downturn … is pushing China's economy to rely more on exports, even as its trading partners express growing concerns about dependence on Chinese supply. Unbalanced integration is still a form of integration.

A China that needs to export to make up for internal demand shortfalls will intrinsically create sectoral-supply dependencies even in the absence of sector-specific government intervention at a time when concerns about over-reliance on Chinese supply are real.

The myth of deglobalisation hides the real shifts

The myth of deglobalisation hides the real shifts (FT)

The trade war of former US president Donald Trump and the supply chain snarl-ups caused by Covid turned deglobalisation into a mainstream topic. And two developments in the past two years suggest that the process might indeed have begun.

The first of these is the fact that global trade in goods in 2023 declined by a little over 1 per cent even though global GDP expanded by a trend-consistent 3.2 per cent, according to the IMF. This is unusual. …

The second indication can be found in the ratio of global trade (in goods) to global industrial production, as based on data provided by the authoritative Dutch central planning bureau. This ratio has been in decline since around mid-2022, suggestive of a deglobalisation trend.

China’s share in global exports has continued to increase, across practically all the major merchandise goods categories. … Hence, a better way to describe what’s going on than deglobalisation is to say that the rest of the global economy is becoming less important to China, but the country continues to become more important to the rest of the global economy.

Exorbitant Privilege Is No More

Brad Setzer tweets:

Exorbitant privilege is no more --

The US FDI income balance (US firms profits abroad net of foreign firms US profits) goes away once the excess profit US firms earn in low tax jurisdictions is stripped out ...

the US income balance is about to fall into a deficit (likely in 2025) -- which should get a bit of attention. In fact, the investment income balance would be in a sizable deficit already if not for US excess FDI income in tax havens

Hard tho to overstate how much attention the positive US income balance has received over the years in international economics. The swing toward a deficit ought to get a bit of attention!

And yes, the real source of "dark matter" was tax avoidance all along -- the US FDI income surplus is all from a small subset of centers of tax avoidance.

Petrodollar Recycling → Critical Minerals Finance

One thesis is that American power and prosperity came from control of oil and the recycling of petrodollars. Pozsar’s predictions are that we are now entering a world where the critical input is not oil but minerals, and where control is more diffuse and disputed (but with a Chinese advantage). China, with control of minerals, won’t need the Yuan-recycling like we have with the petrodollar.

The attached document from the Center for Strategic and International Studies (CSIS) doesn't directly discuss Zoltan Pozsar's theories about the US dollar and commodity-backed currencies. However, the CSIS document provides substantial evidence supporting his view.

The document extensively details China's strategic control over critical minerals processing and production. Further, it describes how China has already demonstrated its willingness to use mineral export restrictions as economic leverage, such as banning rare earth exports to Japan in 2010 and imposing restrictions on gallium, germanium, and graphite exports to the US.

Critical Minerals and the Future of the U.S. Economy (CSIS)

A very comprehensive summary of the current state-of-play.

Today, the United States is 100 percent import reliant for 12 of the 50 minerals identified as critical by the U.S. Geological Survey (USGS) and over 50 percent import reliant for another 29. China is the top producer for 29 of these critical minerals.

Safeguarding the supply chains for advanced technologies in strategic industries is an economic and national security imperative. Policymakers now face the immense task of fortifying supplies of everything from lithium and graphite for advanced battery chemistries to tungsten and rare earth elements for the next generation of warfighting technologies.

Global Warming

We’re All Dead, But, Hey, There’s Money To Be Made

Big banks predict catastrophic warming, with profit potential (Politico Climate Wire)

“We now expect a 3°C world,” Morgan Stanley analysts wrote earlier this month, citing “recent setbacks to global decarbonization efforts.”

The recent reports — from Morgan Stanley, JPMorgan Chase and the Institute of International Finance — show that Wall Street has determined the temperature goal is effectively dead and describe how top financial institutions plan to continue operating profitably as temperatures and damages soar.

JPMorgan … vets investments using “baseline” scenarios that assume global warming of 2.7 degrees to more than 3 degrees by the end of this century.

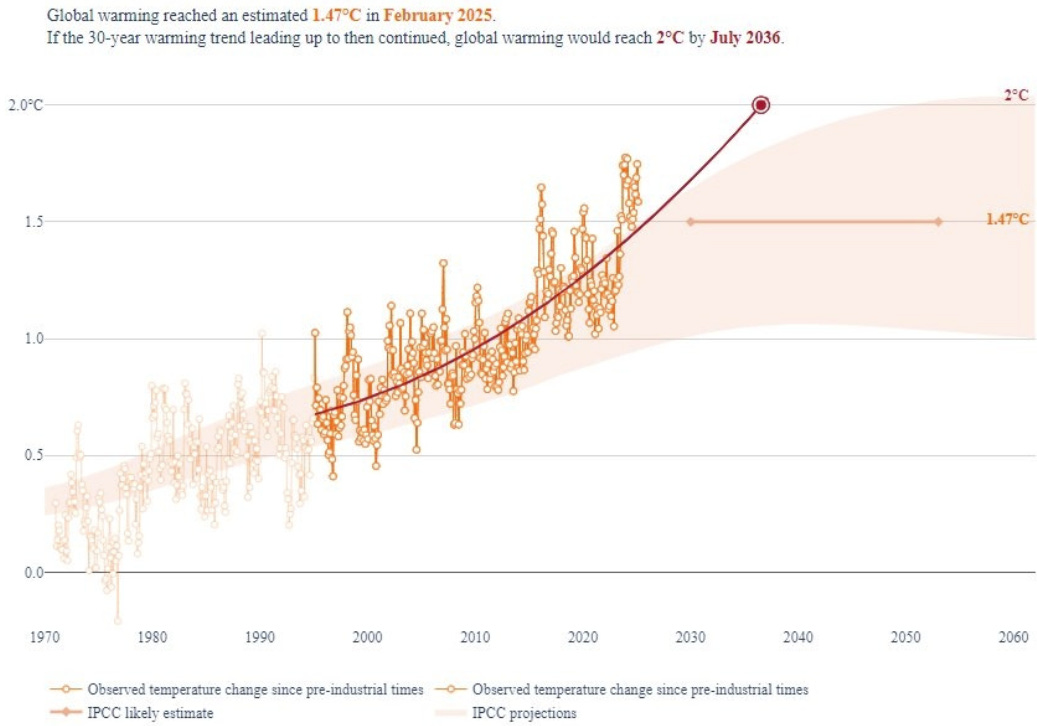

We Are Already At 1.47C

2nd Derivatives

Too Soon?

How we could survive in a post‑collapse world

This paper explores the multifaceted risks of collapse, emphasizing the interconnected environmental, economic, and geopolitical pressures that contribute to vulnerability. By examining historical collapses, such as those of the Roman Empire and the Maya civilization, alongside contemporary examples like Syria, Venezuela, and Yemen, the paper highlights the unique challenges of the current global crisis.