Perspective on Risk - June 16, 2022 (Move fast; break things)

Perspective on Risk - June 16, 2022 (Move fast; break things)

Don’t Fight The Market; Inflation; A Hairy Eyeball Story; When VaR Spikes; Counterparty Default - Followup; Celsius = Crypto MF Global; Elliott Sues LME; Climate Change; Compliance Matters

Update on a few things before I head to Seattle to see my son for a few days.

I seriously started this only expecting to post every two weeks or so.

Don’t Fight The Market

The saying used to be “Don’t Fight The Fed” but in reality the Fed capitulated to the market. The market is in command at the moment, not the Fed.

As you will see below, housing has contributed only about 0.6% of the observed yoy change in inflation, but housing and autos are the two principle industries where demand is quickly affected by rate hikes.

Since (to quote Friedman):

Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.

People usually just quote the first half of the saying without noting the relationship to output. It probably would have been better to increase the number of houses and vehicles, but those things take time, so the Fed had to kill demand.

A faster rise in rates will increase volatility in other areas: watch JPY as one of the first places to observe stress. It’s already being seen in their corporate issuance.

Watch our MBS markets, and in particular the mortgage warehouses. I don’t have first-hand observability anymore, but here is one anecdote I observed:

In bond jargon, MBS went “no-bid.” No buyers for MBS. Then a few posted prices beyond borrower demand, not wanting to buy except at penalty prices. Overnight the retail consequence has been a leap from roughly 5.50% to 6.00% for low-fee 30-fixed loans.1

Chris Whalen raises liquidity issues in a piece2 he wrote today for National Mortgage News:

Whereas the sounds of fear and panic heard among IMBs in May 2020 turned out to be false alarms, the liquidity stress facing the mortgage industry today is real. The true scope of the threat will soon be manifest in falling bids for legacy loans and MSRs. This time around is not just different from 2020, but it could be the worst year the industry has seen in a decade.

At a minimum, the FHFA needs to raise with the Financial Stability Oversight Counsel the need for a liquidity backstop for government lenders. Moreover, the FHFA ought to explore immediately reopening Federal Home Loan Bank membership to IMBs with a regulated insurance or broker/dealer affiliate. The issue here is not capital, but access to liquidity in a time of disappearing loan collateral.

The Biden administration needs to merely raise awareness of the liquidity issue and indicate that a response is in process to growing pressures on IMBs. The FSOC must state that they are aware of the pressures caused by a change in Fed interest rate policy and are prepared to act to address liquidity needs in the government loan market.

Just a reminder that mortgage warehouse problems preceded the problems with Bear Sterns High Grade fund by 4-6 months.

Spreads on Italian 10 year bonds have also already widened out vs their Bund equivalents.

ps: Just before I send this out I noticed this Odd Lots interview of Eric Lonergan:

Why M&G's Eric Lonergan Believes We’re at the Start of Euro Crisis Part II

The other reality is the underlying problem is more severe than in 2010. Italy’s debt to GDP ratio has risen from 120% of GDP to 150%. Its sensitivity to spreads and yields is chronic. Also, political risk is high. There is an election in Italy next year. Possibly the departure of Mario Draghi. This raises the spectre of fiscal non-compliance.

Although Terry Checki used to always remind me that the Italians are richer than God (along with Exxon I guess)

Remember folks, this is just the start of the actual Fed tightening. Everything so far is market foreshadowing. Truly restrictive conditions are still ahead of us.

Inflation

Our earlier discussion suggested three part parts:

Stimulus-induced goods demand interacting with covid-related production and supply chain delays

Russia/Ukraine-related commodity price inflation (energy, fertilizer, foodstuffs)

Tight US labor market conditions and supply/demand imbalance

Mark Zandi recently tweeted this useful breakdown of observed inflation changes.

By Zandi’s count, Stimulus-related inflation increases looks to be about 2.0%, Russia/Ukraine about 3.5%, and Labor only 0.1%. He rightfully adds in housing, which we have discussed before. The Labor share looks low to me.

How To Survive A Liquidity Panic (A Hairy Eyeball Story)

John Macfarlane was Salomon Brothers’ treasurer when his firm became embroiled in scandal. Salomon’s traders had submitted unauthorized bids in the name of customers in US Treasury security auctions. The use of customer names allowed the traders to purchase more securities than Treasury Department rules allowed. Senior management learned about these violations, but failed to take timely action. John and his team were responsible for financing Salomon during the crisis to prevent it from defaulting on its debt.

Here is their story: The Salomon Brothers Treasury Auction Scandal

We reduced the balance sheet. The fairest, easiest, and most effective tool was to increase the internal rate the Finance Department charged each trader for the unsecured capital required to fund his positions.

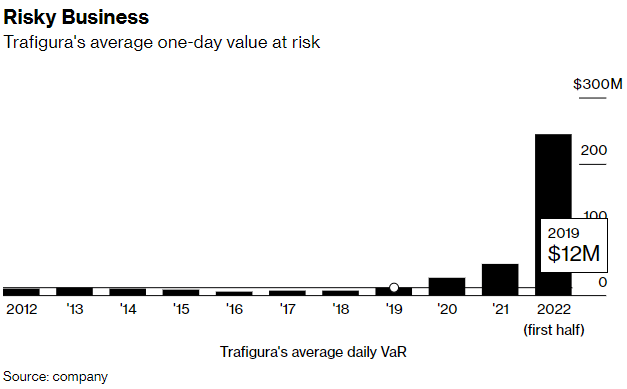

When VaR Spikes

Trafigura Profit Surges Despite War Raising Trading Risks

As commodity prices soared in late February, Trafigura’s value at risk -- a measure of how much the company could lose on a normal trading day -- also shot higher. Over the six-month period, the VaR averaged $244 million, more than five times the previous year’s average.

Counterparty Default - Followup

Remember in the last PoR?

Turns out the FT thinks it was Citi.

Citigroup suffered a technology glitch at the height of the market panic over coronavirus that left it relying on the grace of an exchange clearing house to prevent the bank from defaulting on margin payments for derivatives contracts.

Celsius = Crypto MF Global

If you remember MF Global, when they failed they were shown to have been using client collateral to meet margin calls. Looks like Celsius did the same thing in crypto space. Nothing new under the sun.

Elliott Sues LME

I’ve got to admit, this is going to be fun to watch.

Climate Change

Former colleague and Tobias Adrian and others affiliated with the IMF have written a paper that seeks to complement the existing literature that quantifies the social cost of carbon by focusing “on quantifying the gains from phasing out coal.”

We estimate that the net gain to the world of phasing out coal is very large indeed. By comparing the present value of benefits of avoided carbon emissions from phasing out coal, starting in 2024 on a phase-out schedule in line with the Net Zero 2050 scenario of the Network for Greening the Financial System (NGFS), to the present value of costs of ending coal plus costs of replacing it with renewable energy, our baseline estimate is that the world could realize a net total gain of 77.89 trillion US dollars. This represents an increase of around 1.2% of current world GDP every year until 2100. Per tonne of coal, this represents a net gain of around $125, and per tonne of avoided coal emissions, this represents a net gain of $55.

They’ve also summarized the paper in a blog post, How Replacing Coal With Renewable Energy Could Pay For Itself, for those who prefer consuming information in this fashion.

Also, the BIS issued Principles for the effective management and supervision of climate-related financial risks Standard stuff, fitting climate risk into the core principles framework: governance (accountability; policies & procedures)), internal controls, risk identification and monitoring, risk assessment and insuring sufficient capital & liquidity, reporting, scenario analysis.

Perhaps the more interesting (although really not that interesting) part is:

Principle 13: : Supervisors should determine that banks’ incorporation of material climate-related financial risks into their business strategies, corporate governance and internal control frameworks is sound and comprehensive.

Principle 16: In conducting supervisory assessments of banks’ management of climate-related financial risks, supervisors should utilise an appropriate range of techniques and tools and adopt adequate follow-up measures in case of material misalignment with supervisory expectations.

Principle 18: Supervisors should consider using climate-related risk scenario analysis to identify relevant risk factors, size portfolio exposures, identify data gaps and inform the adequacy of risk management approaches. Supervisors may also consider the use of climate-related stress testing to evaluate a firm’s financial position under severe but plausible scenarios. Where appropriate, supervisors should consider disclosing the findings of these exercises.

Welcome to the world of climate stress tests (and who knows, maybe Written Agreements).

Finally, looks like the SEC is stepping up their review of ESG disclosures: The SEC War on Greenwashing Has Begun

Compliance Matters

SEC Probes Small Bond Trades That Lead to Big Returns

Chinese Traders Find Aluminum Stocks They Financed May Not Exist

Cherry Creek Mortgage, Mortgage Credit News by Louis S Barnes

Whalen, National Mortgage News, Opinion Mortgage industry liquidity risk returns