Perspective on Risk - June 1, 2022

Perspective on Risk - June 1, 2022

It's Too Damn Hot

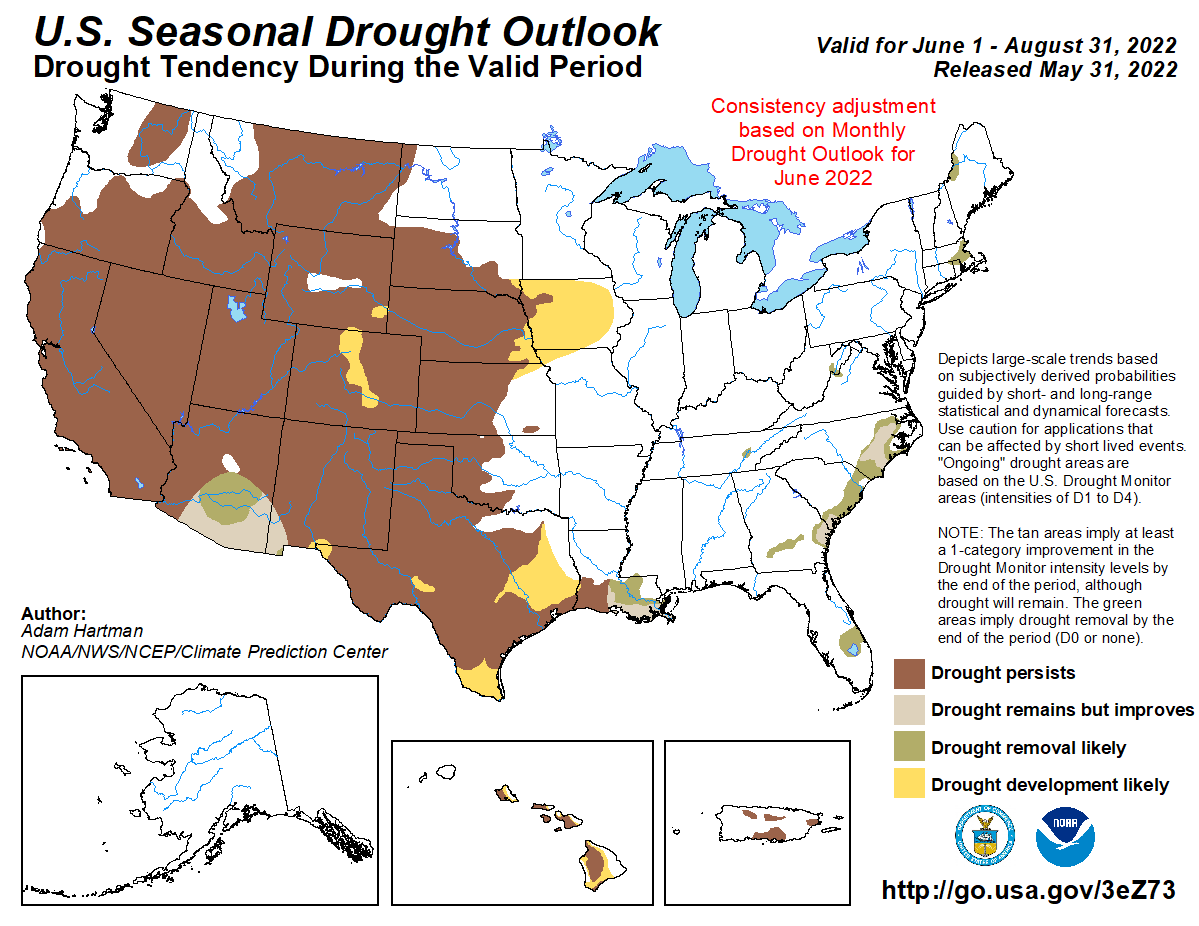

Areas of the US Under Drought is Increasing

From the National Weather Service’s Climate Prediction Center

Ironically, N. Dakota has been too wet this year, which is hurting their grain planting.

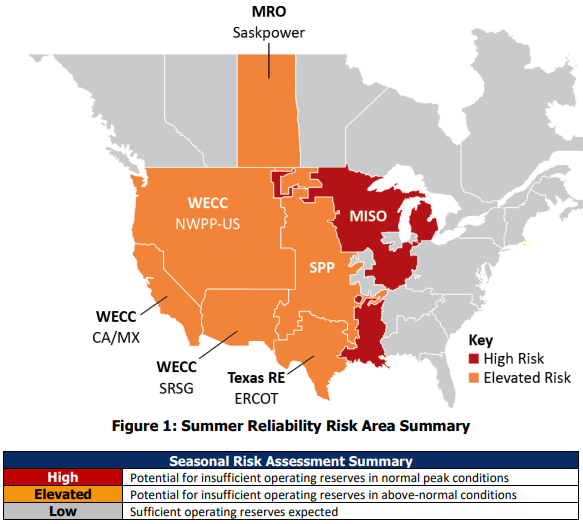

Regulator Cites Near-term Concerns About NA Grid Capacity

2022 Summer Reliability Assessment (from the North American Electric Reliability Corporation). Interesting report for operational risk management nerds.

Midcontinent ISO (MISO) faces a capacity shortfall in its North and Central areas, resulting in high risk of energy emergencies during peak summer conditions.

At the start of the summer, a key transmission line connecting MISO’s northern and southern areas will be out of service.

Anticipated resource capacity in Saskatchewan will be strained to meet peak demand projections, which have risen by over 7.5% since 2021.

Drought conditions create heightened reliability risk for the summer. Drought exists or threatens wide areas of North America, resulting in unique challenges to area electricity supplies and potential impacts on demand:

Grain Producing Areas In Drought

(disclosure: I’m still long $WEAT)

The Definition of Insanity

A Third Worthwhile Paper on the Economics of Climate Change

Previously, I highlighted these three papers that I thought were worthwhile reading on the economics of climate change.

Rapid intensification of the emerging southwestern North American megadrought in 2020–2021

Banks and Climate Change Risk (Oliver Wyman)

I would now commend to you a fourth paper:

Here is the abstract:

The distribution of ownership of transition risk associated with stranded fossil-fuel assets remains poorly understood. We calculate that global stranded assets as present value of future lost profits in the upstream oil and gas sector exceed US$1 trillion under plausible changes in expectations about the effects of climate policy. We trace the equity risk ownership from 43,439 oil and gas production assets through a global equity network of 1.8 million companies to their ultimate owners. Most of the market risk falls on private investors, overwhelmingly in OECD countries, including substantial exposure through pension funds and financial markets. The ownership distribution reveals an international net transfer of more than 15% of global stranded asset risk to OECD-based investors. Rich country stakeholders therefore have a major stake in how the transition in oil and gas production is managed, as ongoing supporters of the fossil-fuel economy and potentially exposed owners of stranded assets.