Perspective on Risk - (Fraud)

Perspective on Risk - (Fraud)

Allianz Global Investors; Archegos; Other

Rainy day. No golf. So you get another spew.

Allianz Global Investors

Allianz is paying $2.3bn in fines, $3.2bn in restitution and $463m in forfeiture over a set of funds that managed about $12bn at peak.

Those of us involved in the Bankers Trust leveraged derivatives examinations will have a sense of deja-vue. Has all the classics:

Providing inaccurate marks to clients and control functions.

Manipulating spreadsheets to get the desired results

Lying about the leverage levels

SEC Press Release

As a consequence of the guilty plea, AGI US is automatically and immediately disqualified from providing advisory services to US registered investment funds for the next ten years, and will exit the business of conducting these fund services.

The SEC Complaint does a really nice job laying out what happened. I highly recommend reading (or at least skimming) the entire thing.

Here are some excerpts that get to the core:

Defendants fraud involved numerous material misrepresentations and other deceptive conduct related to AGI’s US Structured Alpha Funds which were private funds sold to investors.

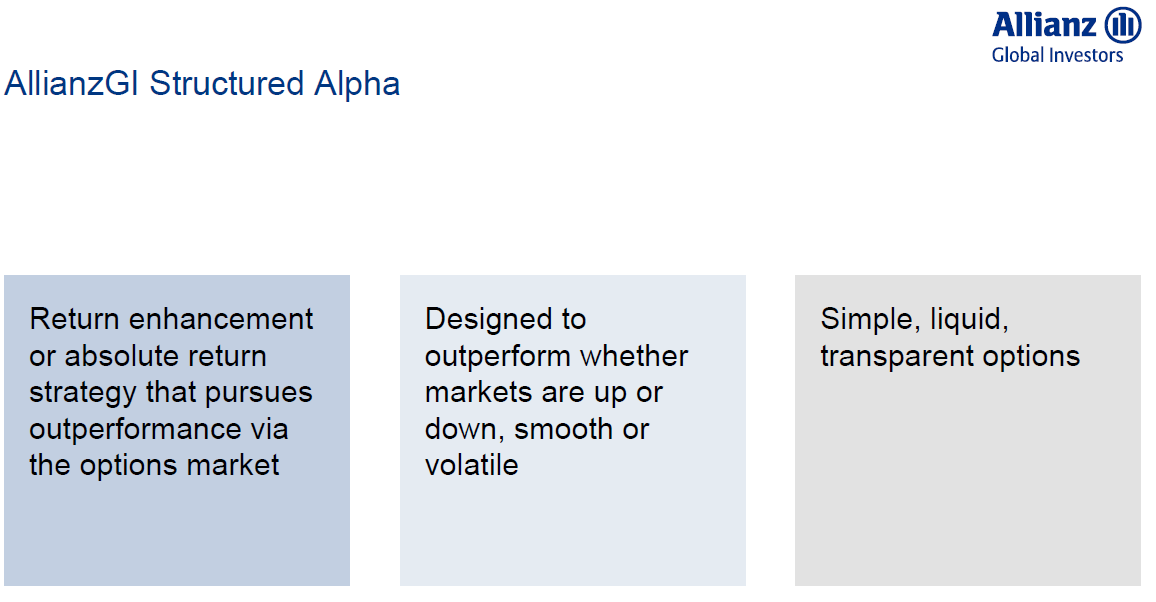

Structured Alpha was a complex trading strategy designed to generate profits by using a portfolio of debt or equity securities as collateral to purchase and sell options, principally on the S&P500 index.

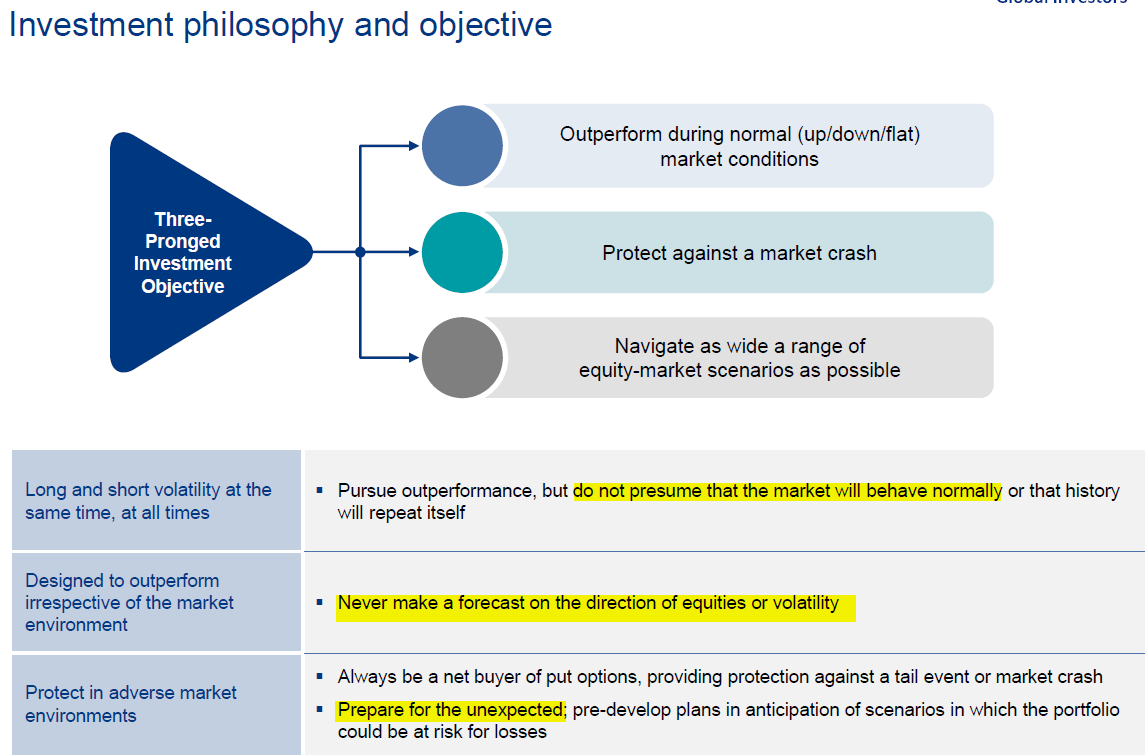

Tourant caused the portfolio management team not to implement a risk management program agreed to with Structured Alpha’s largest investor (Client A), and then to hide that failure and increase his own compensation, Tourant manipulated certain reports provided to AGI US and Client A regarding the risk management program.

One key aspect of how the funds would be managed involved hedging positions consisting of put options, which were sometimes referred to by AGI US personnel as “tail risk hedges” or “TRHs.” … Instead … the portfolio management team, at Tourant’s direction, generally purchased cheaper put options with significantly lower strike prices.

But contrary to the representations in the marketing slide … strike prices for TRHs often were not laddered within the range of -10% to -25% during the relevant period.

Defendants manipulated numerous reports and other information provided to investors. As described below, the reports and information … included (1) risk reports prepared by an AGI US affiliate, IDS GmbH (“IDS Risk Reports”), (2) daily performance data, (3) so-called “Greeks,” which are measures of risk, (4) attribution spreadsheets, (5) expected value (“EV”) sheets, and (6) open position data.

MarketBricoleur has a nice compellation of slides from the marketing deck

I do want to highlight one if-its-too-good-to-be-true element here. Just quickly skimming the pitch deck, early on you get this slide. Wouldn’t we all love outperformance regardless of the markets!

Depends on the sophistication of the client: Gibson Greetings anyone?

And then, who needs forecasts, we’ll just buy protection for every eventuality.

No red flags here! You get what you pay for.

Everything’s OK as long as you don’t have to mark-to-market.

Did you catch the comment in the dark blue above? And don’t worry, ERM is on top of things.

And additional Twitter thread worth quickly taking a look at: cephalopod_v7_final_2.xlsx (it’s ok to click; it links to a single-page Threadreader app summary)

JohannesBorgen also has a thread which is quite good.

Archegos

Back in April, the “SEC Charged Archegos and its Founder with Massive Market Manipulation Scheme.” Here is a link to the complaint filing. This one is just a step of pretty basic failues by the brokers, plus lying by Hwang and crew.

Some excerpts:

Generally, over time, Archegos pursued a long/short equity strategy, generally taking long exposures in single name issuers, and hedging those long exposures largely through short exposures to exchange-traded funds and custom baskets, with some limited short exposures to single name issuers, as well.

The vast majority of Archegos’s long exposure was synthetic, a deliberate strategy Hwang implemented to limit the visibility of market participants and Counterparties into the extent of Archegos’s aggregate holdings.

To avoid reporting thresholds under Section 13(d) of the Exchange Act, when Archegos approached stock holdings representing 5% of the shares outstanding of any particular issuer, it would generally shift from purchasing cash equity positions in that issuer to purchasing synthetic exposure to the issuer through SBSs (BP: security-based swap).

Although each Counterparty could see what positions Archegos held with it, each had limited, and in some cases no, visibility into Archegos’s holdings elsewhere, relying upon Archegos to be truthful and accurate in whatever information it was willing to provide as to its aggregate holdings.

As discussed further below, Archegos was not truthful and accurate in providing such information.

During the Relevant Period, and particularly from January through March 2021, Archegos’s trading of the equities of and SBSs referencing its Top 10 Holdings frequently exceeded 20%, often reached 30%, and even surpassed 40% of certain issuers’ daily trading volume.

During the Relevant Period, and particularly from January to March 2021, Archegos employed numerous tactics intended to artificially impact the share prices of the Top 10 Holdings. None of this trading was based on a principled view of the true value of a particular issuer and instead was intended to artificially inflate share prices.

Archegos, as directed by Hwang, timed some of its trading to maximize market impact, engaging in both pre-open trading, as well as trading during the last 30 minutes of the trading day …

Archegos’s growing position sizes began to bump up against the Counterparties’ trading capacity limits – limits on the amount of SBSs that Counterparties would allow Archegos to hold in particular companies.

Counterparties frequently asked questions about Archegos’s concentration levels and portfolio makeup in order for the Counterparties to evaluate whether and how much to increase capacity limits, or to change margin levels.

Becker and Tomita, who typically led these discussions; Halligan, who at times directed these discussions; and Hwang, who set the tone for these discussions, understood that if Archegos provided truthful information to questions about concentration or portfolio construction, or refused to provide such information, then Counterparties would not, or likely would not, authorize an increase in capacity or provide more favorable margin rates.

But Hwang mandated that Archegos personnel not provide such information, which Counterparties would need to extend risk limits.

As a result of the intense pressure to add capacity that came from Hwang and Hwang’s directive not to provide full information to Counterparties, Archegos, through Halligan, Tomita, and Becker, intentionally and recklessly gave materially false information to Counterparties, or omitted material information, regarding the concentration and liquidity of its portfolio.

Rest is just details. Pretty garden variety.

JohannesBorgen has a thread that explains the likely weaknesses in CS’s counterparty risk management.

Other

Deutsche Bank Gets WhatsApp Information Request From Regulator (Bloomberg)

Probably should look at Telegram too.